/A%20corporate%20sign%20for%20AppLovin%20by%20Poetra_RH%20via%20Shutterstock.jpg)

AppLovin (APP) seems to be missing all of the love technology stocks have been receiving from the markets. While the company is not directly related to AI-driven tailwinds, growth and cash flows point to significant value creation potential.

Recently, Edgewater Research raised its rating for the mobile-advertising company to “Outperform.” Edgewater believes that AppLovin has maintained strong performance in terms of user acquisition and monetization. Further, the “the migration of premium In-App Purchase (IAP) holdouts to the ad-supported model” is likely to benefit AppLovin.

Citi also has a similar view and “added a 90-day catalyst watch to the stock.” The key trigger being migration of AppLovin’s eCommerce platform from the referral phase to general availability.

Therefore, it might be a good time to consider APP stock with June being the month when advertisers across the world have access to AXON, the company's proprietary AI-powered advertising engine, to sign-up and run campaigns.

About AppLovin Stock

Headquartered in Palo Alto, AppLovin is a provider of end-to-end artificial intelligence-powered advertising solutions for businesses. The company generates revenue when its clients achieve their return on advertising spend targets using AppLovin’s advertising solutions.

The company’s two segments include Advertising and Apps. Notably, AppLovin exited the mobile gaming business in July 2025, which has enabled laser-sharp focus on the core business.

For FY25, AppLovin reported revenue of $5.5 billion and an adjusted EBITDA of $4.5 billion. This implies an adjusted EBITDA margin of 82.3%. For the same period, the company’s free cash flows were robust at $4 billion.

AppLovin has been on a high-growth trajectory with Q1 FY26 revenue increasing by 59% year-over-year (YOY) to $1.8 billion. However, APP stock has declined by 17.89% in the last six months. For a company with robust growth and swelling cash flows, this correction seems like a good opportunity to accumulate.

Cash Flows Continue to Swell

There are no second thoughts on the point that businesses are valued on their potential to generate cash flows. From that perspective, AppLovin seems attractive with FY25 operating cash flow of $4 billion.

Further, with healthy growth and robust margins, the company has delivered operating cash flow of $1.3 billion for Q1 FY26. This already implies an annualized FCF potential of $5.2 billion. While AppLovin reported long-term debt of $3.5 billion as of Q1, the company’s cash buffer was $2.8 billion.

Further, with healthy free cash flows, credit metrics are strong. Therefore, the company has been pursuing aggressive share repurchase to create shareholder value.

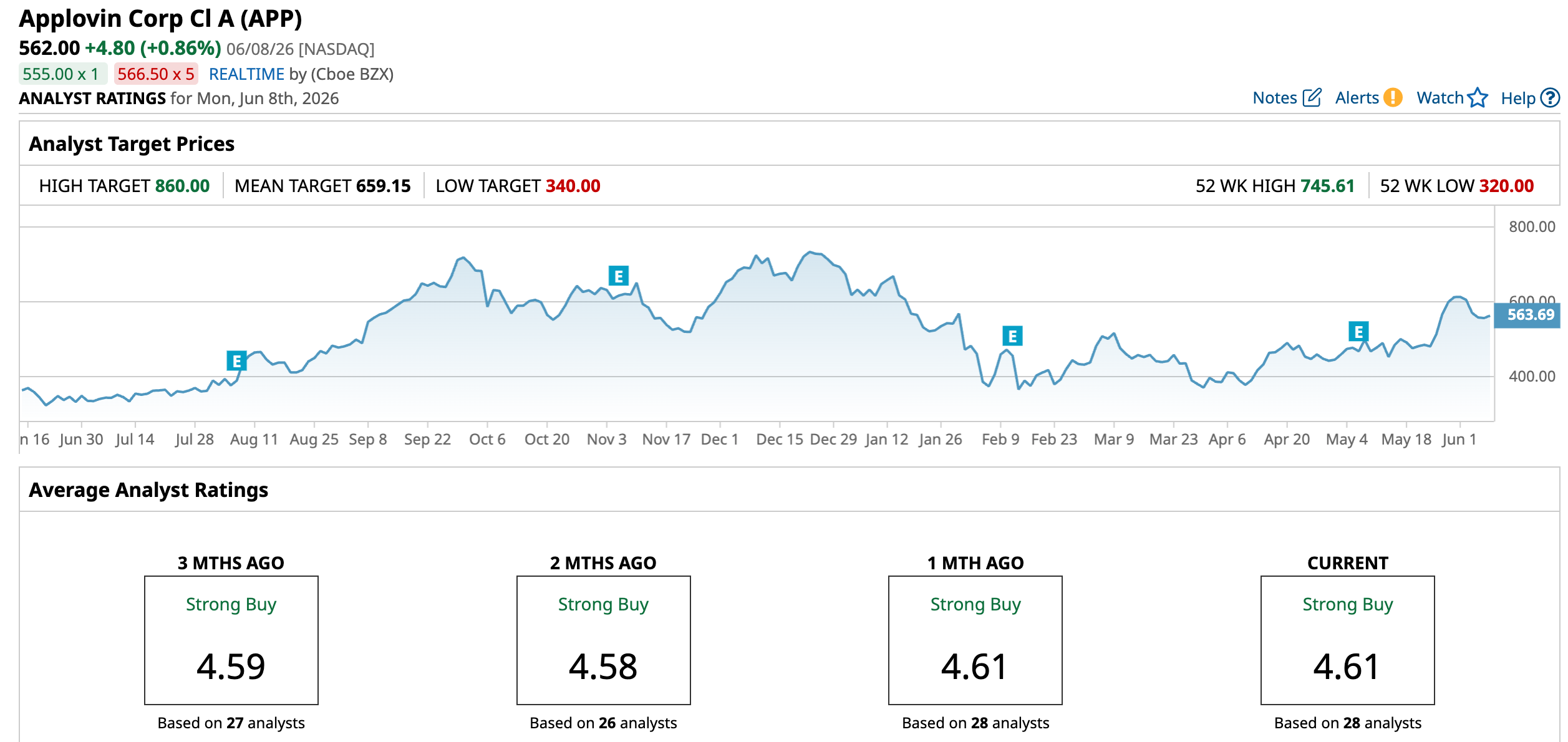

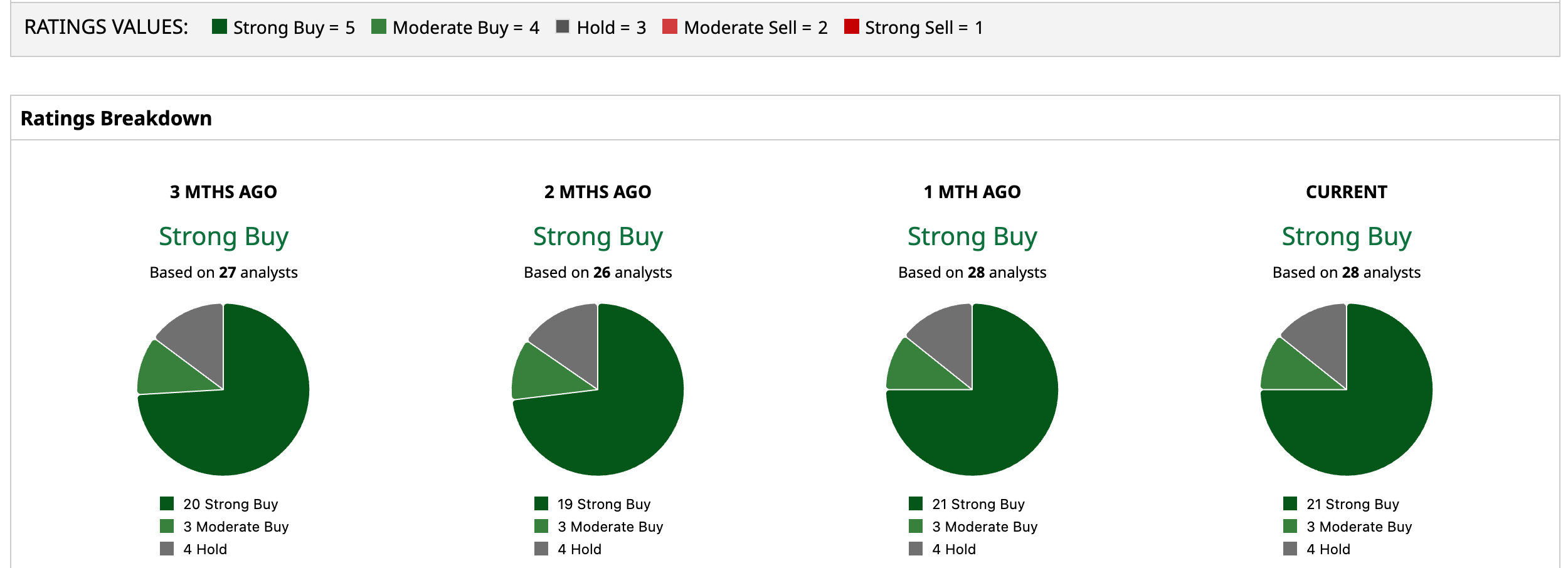

What Do Analysts Say About APP Stock?

Based on 28 analysts with coverage, APP stock has a consensus “Strong Buy” rating. While 21 analysts have a “Strong Buy” rating for APP stock, three have a “Moderate Buy,” and four have a “Hold” rating.

The mean price target of $659.15 represents potential upside of 17.29% from current levels. Further, the most bullish price target of $860 suggests that APP could climb 53% from here.

Concluding Views

From a valuation perspective, AppLovin stock trades at a forward price-to-earnings ratio of 35.25 times. According to analyst estimates, earnings growth for FY26 and FY27 is expected at 57.97% and 32.41%, respectively. Considering the top-line growth and cash flow upside, valuations are attractive and APP stock is likely to trend higher.

For Q2 FY26, the company has guided for revenue between $1.915 billion and $1.945 billion. For the same period, adjusted EBITDA is expected to be between $1.615 billion and $1.645 billion.

With a healthy growth outlook, it’s likely that the stock trend will reverse. Further, as Axon starts running campaigns for advertisers globally, growth acceleration is on the cards. Also, with the prospects of higher conversion rates, stock re-rating is on the cards.

On the date of publication, Faisal Humayun Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.