Not long ago, fears that artificial intelligence (AI) agents could turn the Software-as-a-Service (SaaS) business model on its head sent investors scrambling for the nearest exit. The selloff swept through the sector like a storm and Datadogb (DDOG) got caught in the crossfire despite posting strong results and maintaining a healthy growth outlook.

The irony could not be richer. While many viewed AI as a threat, analysts increasingly saw Datadog as one of the companies best positioned to cash in on the trend. After all, every new AI application, model, and deployment creates another layer of complexity that businesses need to monitor. That reality plays directly into Datadog’s wheelhouse.

The market has started to come around to that view in a big way. A blowout first quarter reignited enthusiasm for the stock and helped turn a former laggard into one of the market’s hottest comeback stories. DDOG stock is now up 73.15% year-to-date (YTD).

Management’s upgraded FY2026 outlook added even more fuel to the rally because it directly linked rising demand for AI observability to stronger revenue expectations. Now investors have another important date staring them in the face.

On June 9, Datadog is scheduled to host its annual Datadog DASH conference, the company’s flagship gathering for builders, engineers, and security teams. The event will focus on observability, security, and AI across modern systems.

Fresh product announcements, customer adoption trends, and management commentary could offer valuable clues about where growth heads next. If the company delivers the goods, shareholders may have even more reasons to smile.

About Datadog Stock

Headquartered in New York, Datadog was founded in 2010 and has grown into one of the leading cloud observability and security platforms in the world. Businesses rely on its software to monitor infrastructure, applications, logs, networks, and security operations across increasingly complex digital environments.

Today, the company commands a market cap of $83.3 billion. Its platform stretches far beyond traditional monitoring tools. Datadog provides AI and Large Language Model (LLM) observability, cost management solutions, incident response capabilities, workflow automation, and real time threat detection services for cloud environments.

Investors have warmed considerably to Datadog’s place in the AI and cloud infrastructure landscape. In the last 52 weeks, DDOG stock is up 92.75%. Moreover, the stock has jumped 87.24% during the last three months.

The rally accelerated further with a 17.64% gain in the past month alone as stronger-than-expected earnings, solid revenue growth, and sharply raised full year guidance turned the tide in the company's favor.

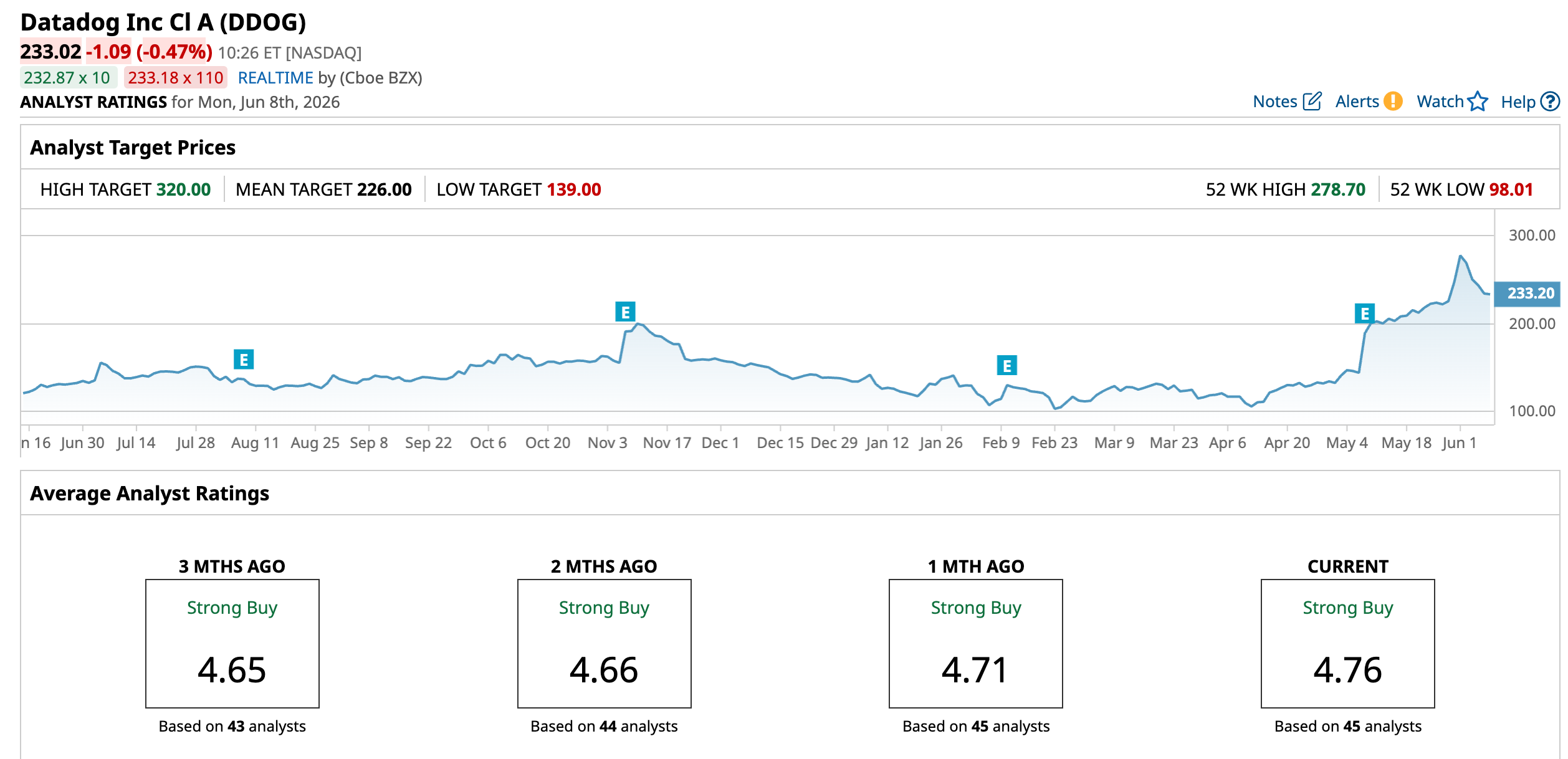

Coming to valuation, DDOG stock is currently trading at 96.70 times forward adjusted earnings and 19.17 times sales. The multiples remain well above industry averages. However, they sit below their own five-year average valuation multiples, which suggests investors may still find a favorable entry point in the stock.

Datadog Surpasses Q1 Earnings

Datadog’s first Q1 FY2026 results, released on May 7, gave investors exactly the kind of quarter they had been hoping for. The market responded with enthusiasm as shares jumped 31.3% on the day of the announcement and tacked on another 6.1% during the following trading session.

Revenue increased 32.2% year-over-year (YOY) to $1 billion. The result landed above the high end of management’s guidance range and comfortably ahead of Wall Street’s expectation of $959.6 million. Non-GAAP EPS grew 30.4% from the year-ago value to $0.60 and cleared analyst estimates of $0.51. Meanwhile, non-GAAP net income rose 29.9% YOY to $218.2 million.

The company also continued attracting larger customers at an impressive pace. Datadog ended the quarter with approximately 4,550 customers generating annual recurring revenue (ARR) of at least $100,000, up from approximately 3,770 a year earlier. Those customers accounted for about 90% of total ARR.

Free cash flow reached $289 million, producing a free cash flow margin of 29%. Meanwhile, the balance sheet remained rock solid, with $4.8 billion in cash, cash equivalents, and marketable securities at quarter end.

Looking ahead, management expects Q2 FY2026 revenue between $1.07 billion and $1.08 billion. The company forecasts non-GAAP EPS between $0.57 and $0.59. Datadog has also raised the bar for the full year. Management now expects fiscal 2026 revenue between $4.30 billion and $4.34 billion, while non-GAAP EPS is projected to land between $2.36 and $2.44.

Wall Street remains optimistic about the earnings trajectory. Analysts expect Q2 FY2026 EPS to grow 100% YOY to $0.12. For full FY2026, analysts project earnings growth of 45.2% YOY to $0.61 per share. Meanwhile, FY2027 forecasts call for another 57.4% increase, bringing the bottom line to $0.96.

What Do Analysts Expect for Datadog Stock?

The strong quarter prompted analysts to sharpen their pencils. Matthew Hedberg of RBC Capital increased his price target on DDOG stock to $250 from $219 while maintaining an “Outperform” rating.

He pointed to Datadog’s ability to benefit from rising observability spending as companies continue migrating workloads to the cloud and expanding their artificial intelligence initiatives. He also highlighted the company’s steady stream of product innovation as another important growth catalyst.

Koji Ikeda of Bank of America also came away impressed. He reiterated his “Buy” rating and lifted his price target to $260 from $225.

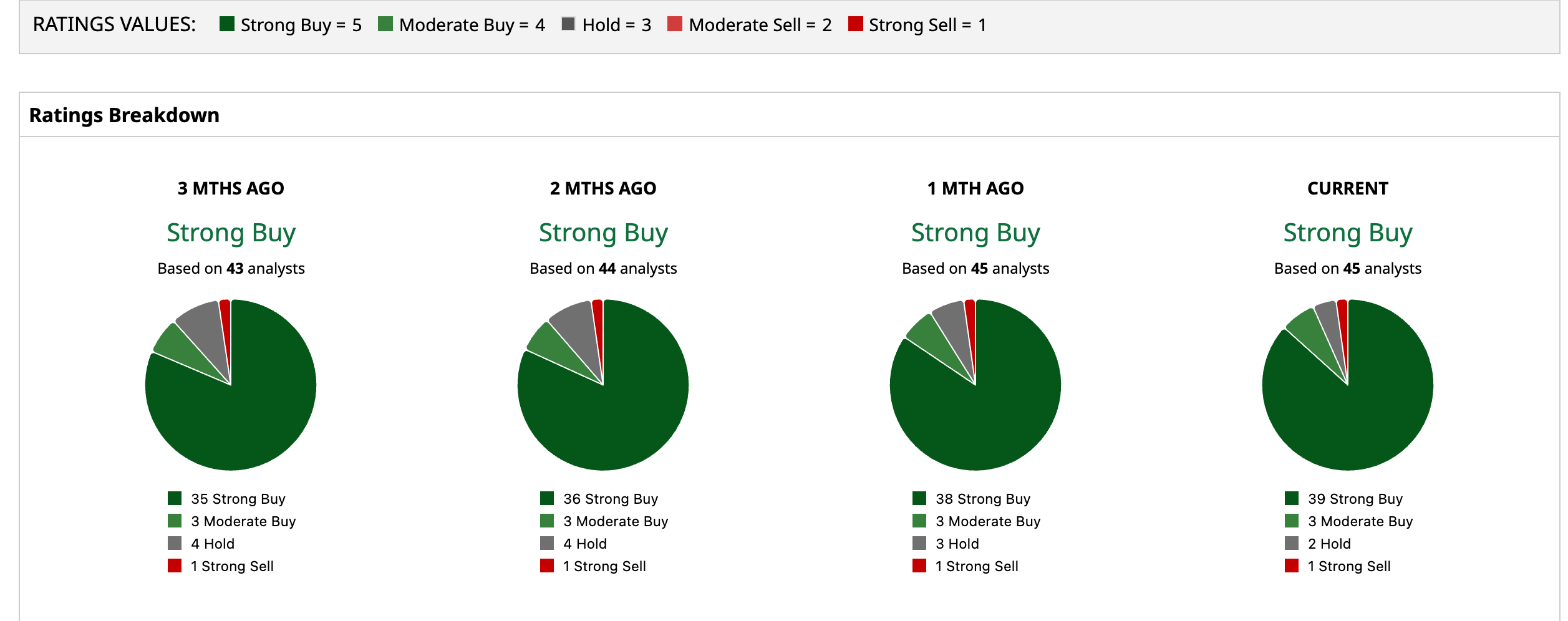

Wall Street continues to wave the bullish flag, assigning the stock an overall "Strong Buy" rating. Among 45 analysts covering the stock, 39 rate it a “Strong Buy,” three recommend “Moderate Buy,” two suggest “Hold,” and one carries a “Strong Sell” rating.

Taken together, those ratings paint a picture of a company that remains firmly in investors’ good graces. The stock is already trading above its average price target of $226. Meanwhile, the Street-High target of $320 suggests a gain of 37.33% from current levels.

On the date of publication, Aanchal Sugandh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Oracle%20Corp_%20office%20logo-by%20Mesut%20Dogan%20via%20iStock.jpg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Boeing%20Co_%20sign%20at%20airport-by%20sanfel%20via%20iStock.jpg)