/Microsoft%20sign%20at%20the%20headquarters%20by%20VDB%20Photos%20via%20Shutterstock.jpg)

The quantum computing market is growing fast, and the numbers back it up. It is expected to rise from about $3.52 billion in 2025 to roughly $20.20 billion by 2030. That path works out to a sharp 41.8% annual growth rate as real‑world uses in drug discovery, financial modeling, logistics, and cybersecurity move from ideas into live tests.

That helps explain why Microsoft (MSFT) has now rolled out its Majorana 2 chip, a second‑generation topological quantum processor that builds on its earlier Majorana 1 design. Wedbush has described Microsoft’s latest quantum step as “another validation” for the whole industry.

For Microsoft, already a key name thanks to Azure, AI, and Copilot, Majorana 2 is the latest effort to add a third pillar of next‑generation computing on top of cloud and artificial intelligence.

All of these set up a straightforward but important question for shareholders. Is Majorana 2 just another lab‑style headline, or the first clear sign that MSFT’s quantum push could one day change how this stock is valued?

Microsoft’s Fundamentals Still Support the Long‑Term Quantum Bet

Microsoft is a U.S. technology company based in Redmond, Washington, known for its Windows operating system, Office suite, Azure cloud business, and its growing push into AI and quantum computing.

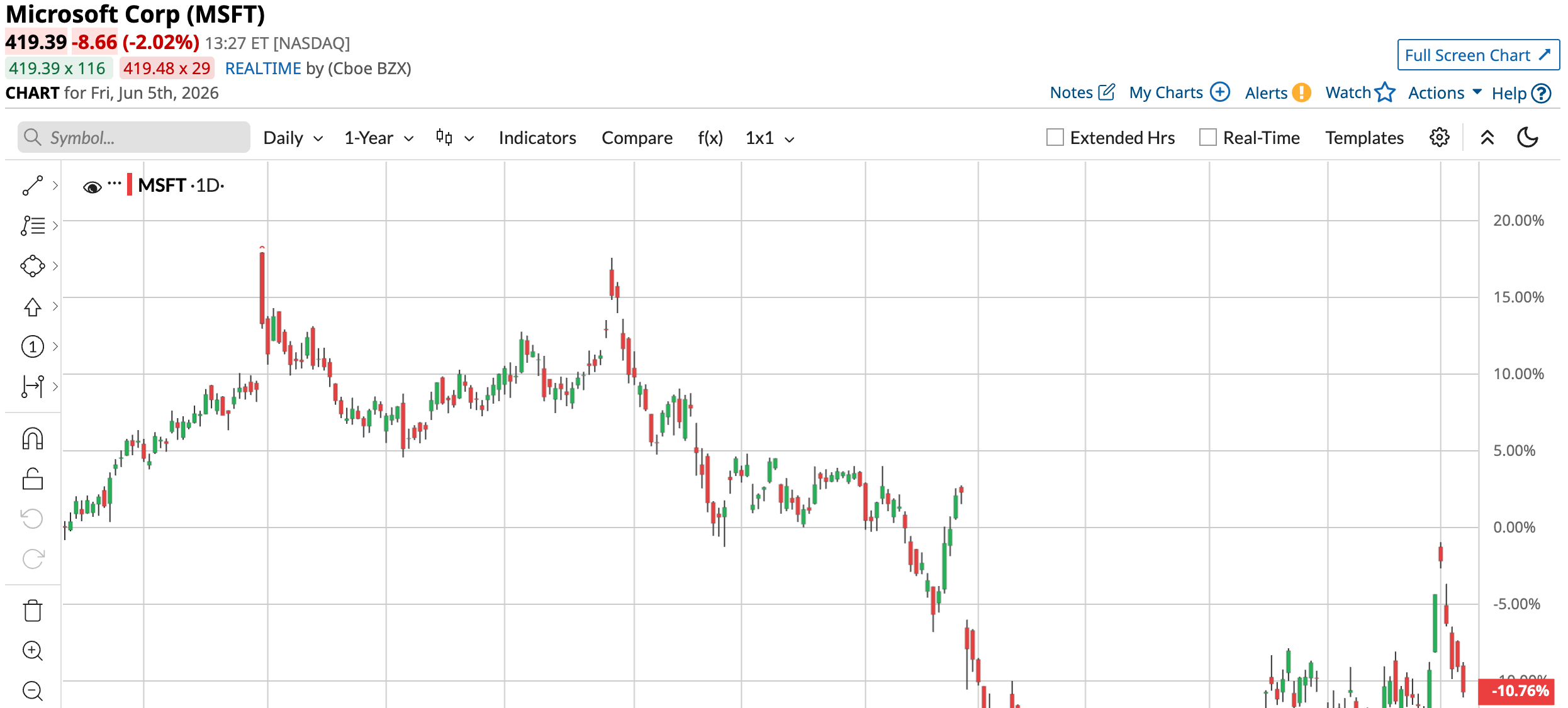

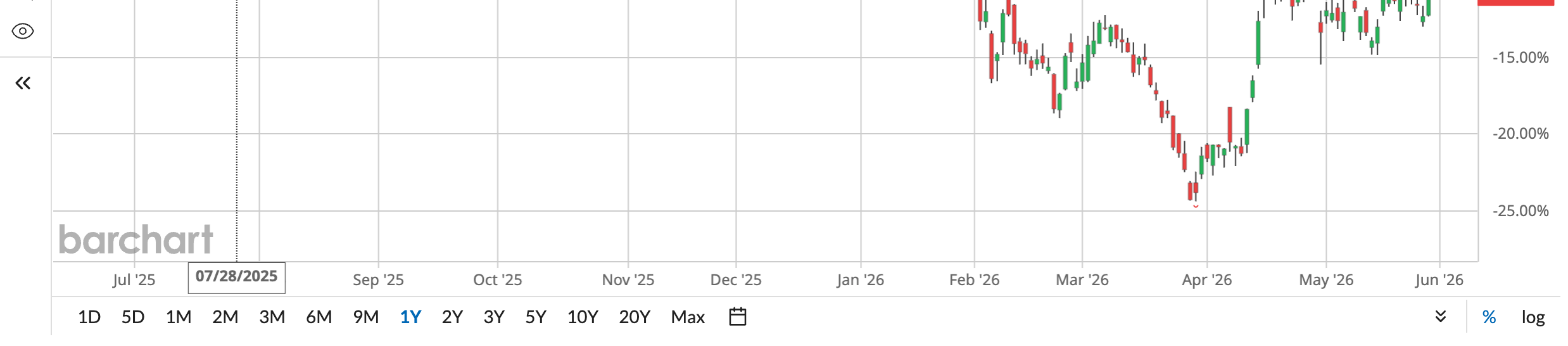

Its is down 13.23% year‑to‑date (YTD) and 10.27% over the past 52 weeks.

The company's equity is valued at roughly $3.18 trillion, and shareholders get a forward annual dividend of $3.64 per share, which works out to a 0.82% yield. This puts Microsoft at 26.44 times trailing earnings and 18.69 times cash flow, slightly above sector medians of 27.05 times and 19.80 times, showing the market is still willing to pay a premium.

MSFT entered the Majorana 2 announcement, coming off a mixed but solid Q1 CY2026 report released in late March. Reported earnings per share were $4.27 versus a consensus estimate of $4.07, a 4.91% upside surprise.

This quarter’s revenue came in at $82.89 billion, up 1.98% year-over-year (YOY), while net income of $31.78 billion fell 17.37%. Notably, gross margin eased from 68.7% to 67.6%, even as the operating margin stayed steady at 46.3%.

This free cash flow margin stood at 19.1% compared with 29% a year earlier. Even so, operating cash flow of $127.49 billion and net cash flow of $1.86 billion, up 57.76% and 131.33% respectively, still give Microsoft plenty of room to fund long‑term projects.

How Microsoft’s Ecosystem Is Lining Up Behind Majorana 2

Microsoft’s Majorana 2 launch sits on top of a setup that is already being built for heavier AI and, over time, quantum‑level workloads. The chip is a second‑generation topological design that aims for a 1,000x boost in qubit reliability over the earlier version, with qubit lifetimes now measured in tens of seconds instead of very short bursts. Microsoft is targeting scalable quantum systems by 2029, several years ahead of its earlier timeline.

Around that core, Microsoft is tightening its AI and data infrastructure in ways that matter for the stock. Pinecone’s Nexus platform now plugs straight into Microsoft OneLake inside Microsoft Fabric, so AI agents can work off structured “artifacts” built on enterprise data instead of trawling raw files each time. That setup has led to more than a 95% drop in frontier large‑language‑model token use, roughly 30x faster task completion, and success rates above 90% in testing.

Healthcare is another area where this build‑out shows up clearly. The Mayo Clinic and Microsoft are co‑developing a high‑end AI model designed specifically for healthcare, using Mayo’s de‑identified health data, clinical know‑how, and long‑term patient records alongside Microsoft’s cloud and AI stack. The model is meant to support deeper clinical reasoning across tasks like earlier diagnosis and more tailored treatment choices.

Taken together, the hardware progress with Majorana 2 and these focused AI and data moves point to Microsoft laying down the rails now.

What the Street Is Pricing In Around Microsoft’s Quantum Push

Microsoft’s near‑term earnings picture gives analysts some comfort. The next earnings release is scheduled for July 29, 26, with the current quarter ending June 26 carrying an average earnings estimate of $4.21 per share. That compares with $3.65 in the same quarter a year ago and points to expected YOY growth of 15.34%.

The buy‑side is leaning in as well. Pershing Square’s (PS) move into Microsoft was made public on May 15, after the fund had been building the position since February, and it was clearly a play on the pullback. Bill Ackman has framed MSFT as mispriced after a period of weaker cloud growth and higher spending, suggesting the market reaction has gone too far.

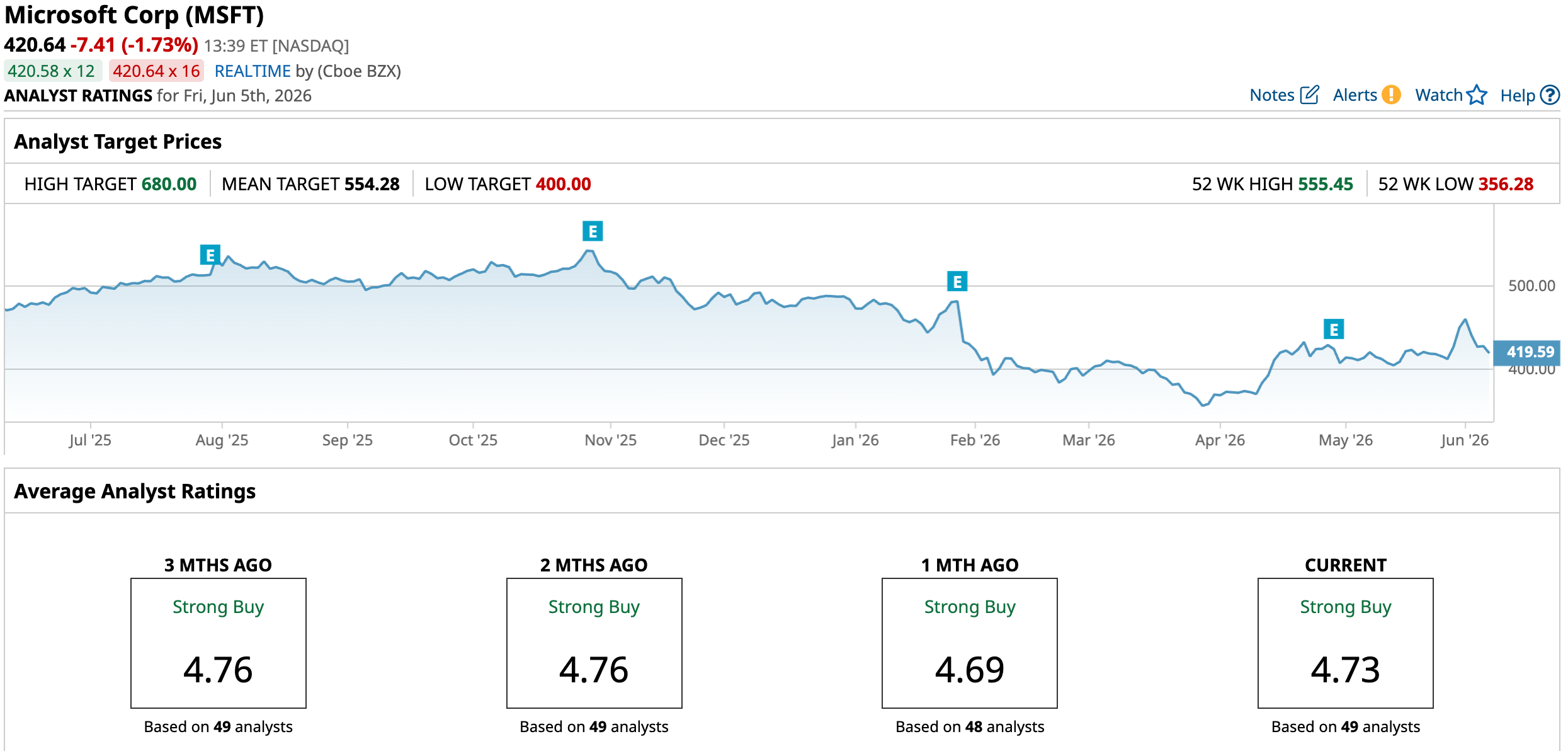

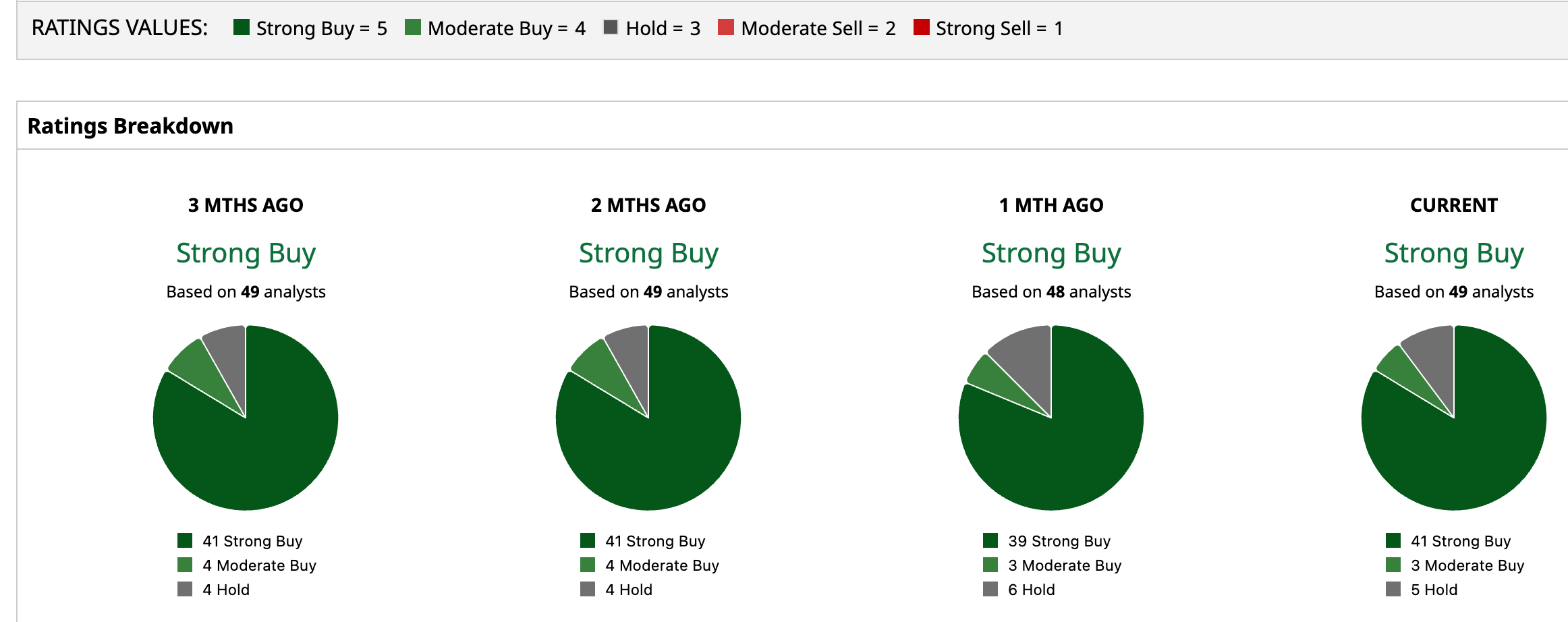

The Street’s view largely supports that stance. Analysts remain upbeat on MSFT, with the consensus still sitting in “Strong Buy” territory rather than drifting toward neutral. The average target price of $554.28 points to 31.77% upside from current levels.

Conclusion

Majorana 2 still sits in the “option value” bucket for Microsoft’s story, but it makes that option feel more tangible for a company already generating strong cash. Given the current growth outlook and upbeat price targets, MSFT looks more likely to drift higher than to see a major reset over the next year. Quantum’s job from here is to move slowly from eye‑catching headlines to something investors begin to factor into the long‑term valuation, one step at a time.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20close-up%20of%20an%20AMD%20office%20by%20gehapromo%20via%20Adobe%20Stock.jpeg)

/ServiceNow%20Inc%20building%20in%20Silicon%20Valley-by%20Sundry%20Photography%20via%20iStock.jpg)

/A%20logo%20for%20Bending%20Spoons%20displayed%20on%20a%20smartphone%20screen%20by%20Timon%20via%20Adobe%20Stock.jpeg)