/Microsoft%20sign%20at%20the%20headquarters%20by%20VDB%20Photos%20via%20Shutterstock.jpg)

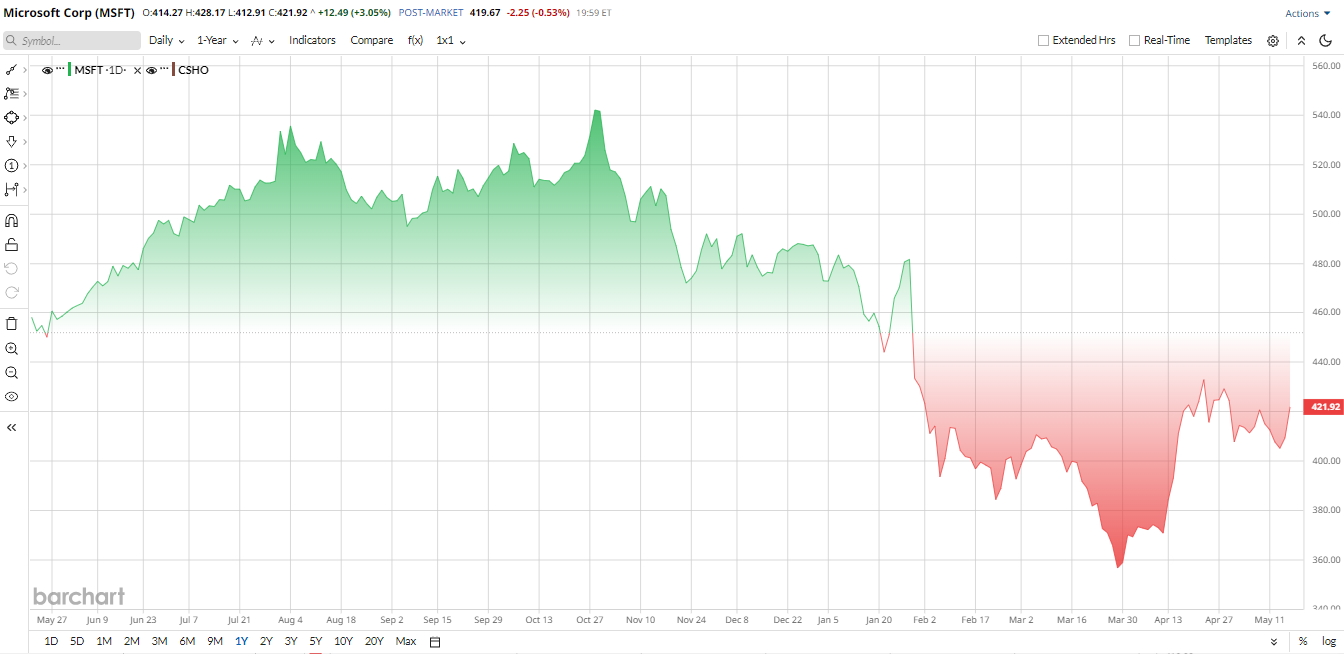

Microsoft (MSFT) has been under pressure this year, and that pullback is exactly what caught the attention of Bill Ackman. On May 15, Pershing Square disclosed a new Microsoft stake after starting to build the position in February. Ackman said the valuation looked compelling after MSFT stock slid on slower cloud growth and a sharp rise in spending.

Shares of Microsoft jumped 3% on the news, serving as a reminder that Wall Street still treats the stock like a market heavyweight.

Why Has Microsoft Stock Been Weak?

Microsoft is down almost 14% year-to-date (YTD), underperforming the broader market. The selloff has not been about a broken business. Instead, it has been about nerves. Investors are worried that the company is spending too much on AI infrastructure, with 2026 capital spending set at about $190 billion. They have also questioned whether Copilot and Azure can keep growing fast enough to justify that outlay. In addition, MSFT stock has been hit by broader Big Tech weakness and the fear that AI competition could chip away at Microsoft's cloud and productivity moat.

That backdrop helps explain why Bill Ackman moved in now. The Pershing Square CEO argues that the Azure cloud division and M365 productivity franchise remain dominant enterprise assets, and he pushed back on the idea that the OpenAI partnership changes are a reason to panic. Microsoft shares had already fallen enough to give long-term investors a better entry point than they had earlier in the year.

Microsoft is still not cheap in the classic bargain sense, but its multiples have come down. MSFT stock trades at about 25.1 times forward earnings, right in line with the sector median and offering a discount from its own five-year average. For a company still growing revenue at a high-teens pace, that is a much friendlier setup than the market provided when shares raced higher.

Bill Ackman Is Betting Big That AI Spending Fears Are Overdone

Bill Ackman’s stake disclosure landed like a thunderclap. Pershing Square first accumulated shares in February after Microsoft’s fiscal second-quarter report sent the stock tumbling.

Ackman directly addressed the two biggest market worries. On M365, he argued that the suite’s deep integration with enterprise security, compliance, and identity systems makes it difficult to replicate. For Azure, he pointed out that about two-thirds of the $190 billion in capex is set toward growth-generating servers and networking gear, not waste. Ackman also highlighted an underappreciated asset in Microsoft’s 27% stake in OpenAI, which could be worth an estimated $200 billion, or about 7% of Microsoft’s entire market capitalization.

The real impact is the signal: one of Wall Street’s most patient, concentrated investors is betting big that the AI fears are overblown.

Microsoft Tops Q3 Earnings Estimates

Microsoft’s fiscal Q3 results, reported on April 29, were solid across the board. Revenue rose 18% to $82.9 billion, operating income climbed 20% to $38.4 billion, and net income increased to $31.8 billion, or $4.27 per diluted share. Microsoft Cloud revenue reached $54.5 billion, while the AI business crossed a $37 billion annual revenue run rate.

The segment detail looked good, too. Productivity and Business Processes revenue rose 17% to $35 billion, Intelligent Cloud revenue increased 30% to $34.7 billion, and Azure and other cloud services grew 40%. More Personal Computing slipped 1% to $13.2 billion, but that is hardly a surprise in a weak PC environment. Microsoft also ended the quarter with $32.1 billion in cash and cash equivalents, which gives it plenty of flexibility even with heavy AI spending.

The spending story is the only part that still makes investors flinch. Capex came in at $31.9 billion for the quarter, and management said it expects about $40 billion in capex for fiscal Q4. Even so, the company guided Q4 revenue between $86.7 billion and $87.8 billion, which suggests growth is still running at a healthy clip.

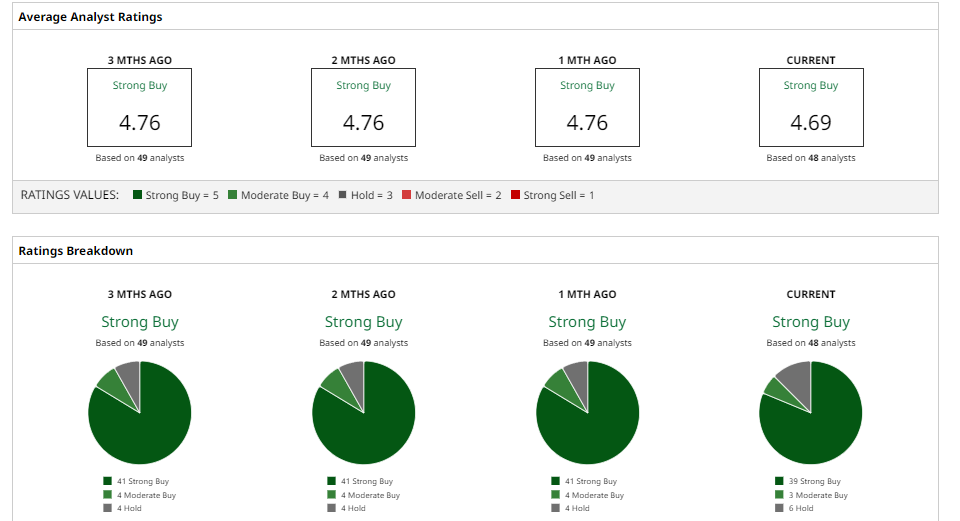

What Do Analysts Say About MSFT Stock?

For the most part, Wall Street remains in Microsoft’s corner. Wedbush has an “Outperform” rating and a $575 price target, TD Cowen has a “Buy” rating and a $540 target, and Goldman Sachs recently lifted its target to $610 while keeping a “Buy” rating. Meanwhile, Deutsche Bank trimmed its target to $550 but left its “Buy” rating intact.

MSFT stock has a consensus "Strong Buy" rating from analysts with an average price target of $554.43. That implies about 33% potential upside from current levels.

Overall, it looks like Ackman is betting that a great business with durable enterprise demand, improving AI monetization, and a more reasonable valuation can keep compounding over time. For long-term investors, that is the real question, and Microsoft still has a strong case.

On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/An%20aerial%20view%20of%20a%20data%20center%20cooling%20system%20by%20Sepia100%20via%20Adobe%20Stock.jpeg)