/Hilton%20Worldwide%20Holdings%20Inc%20hoter%20logo%20by-%20tupungato%20via%20iStock.jpg)

Hilton Worldwide Holdings Inc. (HLT), headquartered in McLean, Virginia, is a hospitality company that manages, franchises, owns, and leases hotels and resorts. Valued at $75.4 billion by market cap, the company provides hospitality services through various hotel brands, such as Waldorf Astoria, Hilton Hotels & Resorts, Home2 Suites by Hilton, and more as well as owns over 8,300 properties across 138 countries.

Companies worth $10 billion or more are generally described as “large-cap stocks,” and HLT perfectly fits that description, with its market cap exceeding this mark, underscoring its size, influence, and dominance within the lodging industry. Hilton's diverse brand portfolio, featuring Hampton and Hilton, showcases its robust market presence with a vast room network. The Hilton Honors loyalty program, boasting 195 million members, drives customer retention and attracts new guests, ensuring a steady revenue flow. With a growth in loyalty program membership, Hilton's customer base and market reach continue to expand.

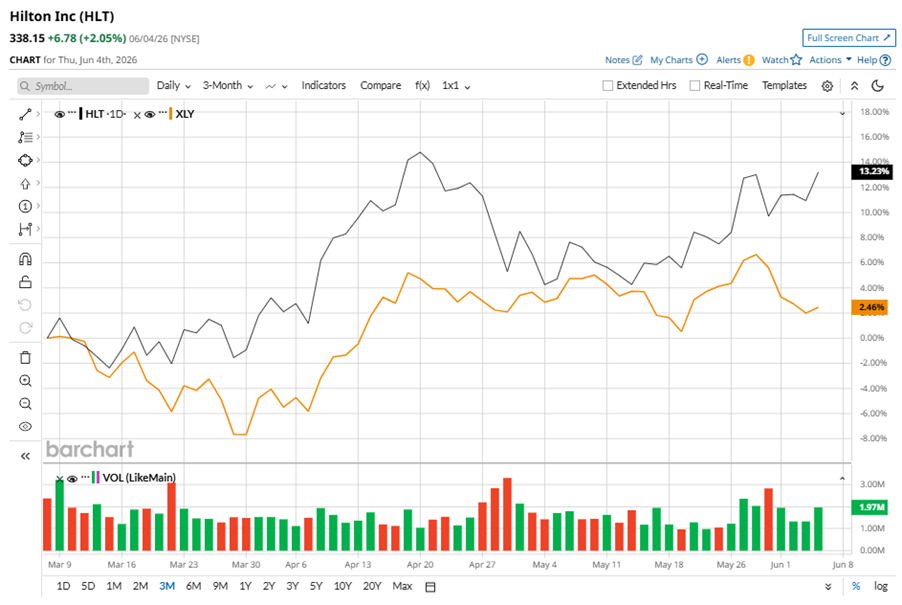

Despite its notable strength, HLT slipped 1.9% from its 52-week high of $344.75, achieved on Apr. 17. Over the past three months, HLT stock has gained 10.9%, outperforming the State Street Consumer Discretionary Select Sector SPDR ETF’s (XLY) marginal gains during the same time frame.

Shares of HLT rose 17.7% on a YTD basis and climbed 35.6% over the past 52 weeks, outperforming XLY’s YTD losses of 1.8% and 9.2% returns over the last year.

To confirm the bullish trend, HLT has been trading above its 50-day moving average since early April, with slight fluctuations. The stock has been trading above its 200-day moving average over the past year.

Hilton’s outperformance was driven by steady U.S. demand and strong net unit growth, with RevPAR up on broad gains across business, leisure, and group segments. The company opened 131 hotels with 16,000+ rooms and reached a record 527,000-room pipeline, led by expansion in APAC, India, and Europe. Looking ahead, Hilton expects demand to broaden into mid- and lower-priced segments, supported by AI investments and new brand launches, while staying cautious on the Middle East conflict and supply chain risks.

On Apr. 28, HLT shares closed down by 2.7% after reporting its Q1 results. Its revenue was $2.9 billion, missing analyst estimates of $3 billion. The company’s adjusted EPS of $2.01 beat analyst estimates by 1.8%.

HLT’s rival, Marriott International, Inc. (MAR) shares have taken the lead over the stock, with a 24.2% uptick on a YTD basis and 47.1% gains over the past 52 weeks.

Wall Street analysts are reasonably bullish on HLT’s prospects. The stock has a consensus “Moderate Buy” rating from the 24 analysts covering it, and the mean price target of $347.33 suggests a potential upside of 2.7% from current price levels.

On the date of publication, Neha Panjwani did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/United%20Parcel%20Service%2C%20Inc_%20logo%20on%20truck-by%20100pk%20via%20iStock.jpg)

/Netflix%20open%20on%20tablet%20by%20rswebsols%20via%20Pixabay.jpg)