/NVIDIA%20Corp%20video%20chip-by%20Antonio%20Bordunovi%20via%20iStock.jpg)

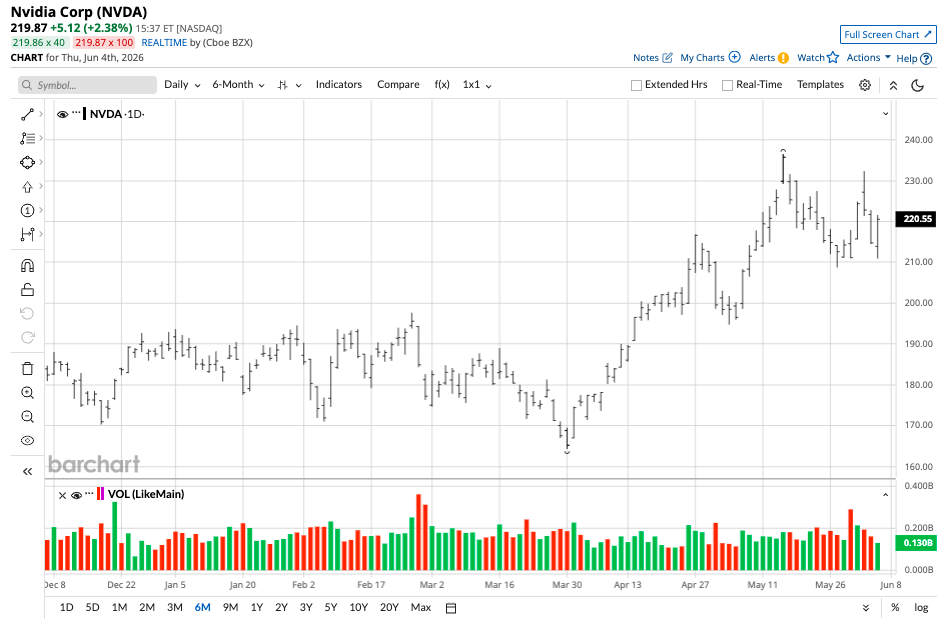

There are plenty of fast-growing companies out there, but Nvidia (NVDA) is in a whole different lane. Thanks to a major global AI buildout and a seemingly insatiable demand for compute, the tech giant has rapidly evolved into a revenue engine operating at industrial scale.

It only takes a quick glance at Nvidia’s last quarterly to get an idea of the sheer volume of cash this company is raking in. That’s why social media has lit up over the past couple of weeks with a new viral claim: Nvidia is generating roughly $1 million in revenue every 129 seconds and $1 million worth of profit every 263 seconds.

That probably sounds like some crazy exaggeration designed for maximum shock value. But when you run the numbers using Nvidia’s actual filings, $1 million every 129 seconds is actually a conservative estimate.

Let’s take a closer look.

Do the Numbers Really Add Up?

The short answer is: Yes. Nvidia released its financial results for the first quarter of fiscal year 2027, and the numbers were massive. The company posted an 85% spike in quarterly revenue, bringing in $81.6 billion and more than $61.2 billion in gross profit.

When you break that revenue figure down, it translates to $10,484 every second of the quarter. That means Nvidia’s making $629,021 per minute, so if you’re aiming for the $1 million mark, 129 seconds is actually a little off.

Depending on your margin assumptions, it’s more like Nvidia is making $1 million every 95-96 seconds. On the profit side of things, this viral claim that’s been doing the rounds is a lot closer. When you account for Nvidia’s high margins, we’re looking at about $1 million every 263 seconds.

Let that sink in for just a minute. The headlines aren’t fake news. If anything, they’ve actually been understating how quickly Nvidia has monetized the AI cycle.

The reason these numbers are so unreal is because Nvidia’s business has fundamentally changed over the past few cycles. This is no longer some gaming GPU company. It’s basically the backbone of the global AI economy, and you can see that from its filings.

More than 80% of its revenue comes from its data center segment, which means all the chips and systems that everybody else is relying on to train and deploy large language models, autonomous systems, recommendation engines — you name it.

That huge level of demand is admittedly coming from a tiny group of customers, but they’re all big hyperscalers. We’re specifically talking about Amazon (AMZN), Microsoft (MSFT), Alphabet (GOOGL)(GOOG), and Meta (META). These giants are shelling out tens of billions of dollars to build out their AI factories, and they all rely on Nvidia GPUs.

That makes Nvidia the AI bottleneck, which is what gives it lucrative pricing power.

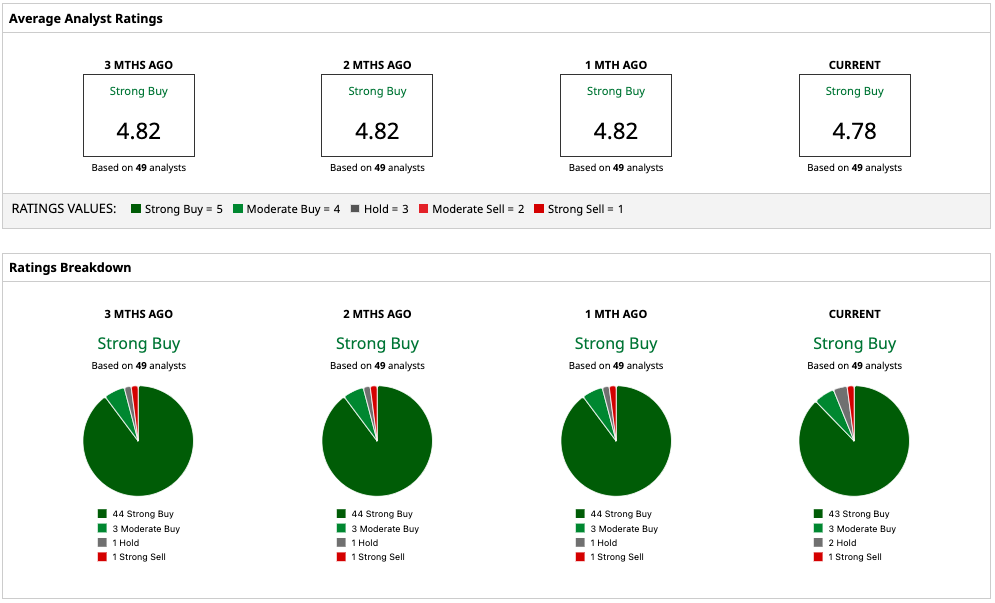

Nvidia isn’t competing in a normal chip market. It dominates the high-end AI accelerator segment, and its GPU architectures are now deeply embedded in all the major cloud ecosystems. That’s why its gross margins have stayed around the 70% mark throughout this AI boom, and it’s why Nvidia will keep riding high as the rest of its fiscal year unfolds.

These big customers are too heavily invested to switch to anyone else, and so Nvidia isn’t really selling chips in the traditional sense. It’s selling access to computational capability — and with demand outpacing supply, those big spenders are going to have to keep paying Nvidia premium prices.

Nvidia’s Success Is a Reflection of the AI Boom

This whole “dollars per second” framing isn’t just some mathematical clickbait (although you did click on this, so it must have worked). It also reveals something deeper about market structure, because Nvidia’s fortunes really boil down to a perfect storm composed of three converging forces.

First, there’s an unprecedented level of capex. Cloud providers are already spending billions and billions on AI infrastructure buildouts — but AI adoption is still in its early stage, which is the second force driving Nvidia’s numbers. Most corporates aren’t anywhere close to full deployment, which means that demand isn’t going to peak for a long time. It’s just going to keep accelerating.

Finally, those supply constraints we mentioned earlier are still favoring sellers. That means Nvidia’s pricing power is totally safe, and the combination of these three elements creates a rare environment in which revenue doesn’t just scale linearly.

The big question for investors is how long this pace will continue.

No growth curve lasts forever — especially at this intensity, and the semiconductor cycle is volatile. Every hardware boom eventually runs into an issue of oversupply, disruption, or demand normalization, right?

Then again, these rules don’t hit Nvidia in quite the same way. Its complete exposure to AI infrastructure means that its fortunes aren’t tied to a product refresh cycle. Nvidia sits at the heart of a structural shift in computing, and so these elements won’t affect the company’s bottom line in the ways we might normally expect.

Even so, investors should be cautious when it comes to extrapolating Nvidia’s epic Q1 results too far into the future. AI deployment will eventually shift into maintenance mode, and this rapid infrastructure buildout will normalize. But it’s not going to happen any time soon, which means Nvidia has plenty of time to adapt.

In the meantime, it’s fair to say Nvidia is operating at a scale of monetization that few companies on Wall Street could even dream of.

On the date of publication, Nash Riggins did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Microsoft%20headquarters%20By%20Peter.jpeg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/NVIDIA%20Corp%20logo%20outside%20building-by%20BING-JHEN_HONG%20via%20iStock.jpg)

/Amazon%20-%20Image%20by%20bluestork%20via%20Shutterstock.jpg)

/Robot%20arm%20industrial%20automation%20manufacturing%20by%20Eakrin%20via%20Adobe%20Stock.jpeg)