/The%20UiPath%20logo%20on%20a%20corporate%20office%20by%20Ian%20Dewar%20Photography%20via%20Shutterstock.jpg)

While most artificial intelligence (AI) companies reported blockbuster numbers this earnings season, some are still trying to prove that AI can generate meaningful revenue growth, improve profitability, and deepen customer relationships. UiPath (PATH), however, appears to be making tangible progress on all three fronts, according to its first quarter of fiscal 2027 earnings.

Here are two major green flags and one warning sign investors should be mindful of before considering PATH stock now.

Green Flag No. 1: UiPath Has Finally Reached GAAP Profitability

UiPath has now achieved a significant profitability milestone. It reported its first GAAP profitable quarter, with net income of $0.04, up from a loss of $0.04 in the year-ago quarter. This profitability was driven not just by cost cuts but also by a 17% year-over-year increase in revenue to $418 million, while ARR increased by 12% to $1.9 billion. This shows that UiPath is looking for ways to increase profitability while still expanding its business.

The company also generated $130 million in adjusted free cash flow, highlighting that increased profitability is translating into real cash. It also ended the quarter with a stable balance sheet with no debt and $1.4 billion in cash, cash equivalents, and marketable securities.

Green Flag No. 2: AI Is Driving Bigger and Bigger Deals

Management emphasized that AI was the biggest contributor to the Q1 performance. AI was part of 16 of the company's top 20 deals made in Q1. Notably, customers generating more than $30,000 in ARR increased 7% year-over-year. UiPath continued to gain traction among its largest clients, with customers producing at least $100,000 in ARR increasing 11% to 2,620 and those exceeding $1 million in ARR jumping 18% to 374. Furthermore, its remaining performance obligations (RPO) increased 15% year-over-year to $1.41 billion, while current RPO grew 17% to $988 million.

Red Flag: Customer Retention Has Stabilized, Not Reaccelerated

Despite the encouraging results, the one area that concerned me was that UiPath's retention and growth numbers appear stable rather than accelerating. Net retention rate stood at 108%. While the number is not bad, these levels are lower than many high-growth software companies have achieved during their fastest expansion periods.

Similarly, while ARR growth of 12% is encouraging, it remains far below the growth rates investors once associated with UiPath during its earlier years as a public company. Furthermore, UiPath continues to see customer losses among smaller businesses. While this weakness is being offset by acceleration within larger accounts, investors prefer to see growth across the entire customer bases.

Adding to these concerns is management’s second quarter revenue outlook, which didn’t appear very promising. The company expects revenue between $395 million and $400 million, implying a sequential decline from the first quarter's $418 million. ARR could land around $1.93 billion. The outlook for Q2 reflects uneven quarterly growth patterns. For fiscal 2027, management projects revenue between $1.77 billion and $1.78 billion, a 10% potential growth at mid-point, while ARR could be around $2.06 billion. In other words, while UiPath is doing well, these projections don't provide the assurance of sustained high growth, which would eliminate concerns about its long-term growth trajectory.

The Bottom Line: Is PATH a ‘Buy’ Now?

UiPath achieved its first-ever GAAP profitable quarter, expanded operating margins to 22%, generated strong free cash flow, and showed clear evidence that AI is driving larger customer engagements. At the same time, investors should remain mindful that customer retention has stabilized, which is a good sign for a matured company. However, for a growing company, customer retention should instead be accelerating.

For now, however, the two green flags appear stronger than the one warning sign. UiPath is proving that it can grow profitably while capitalizing on enterprise demand for AI-powered automation. Analysts predict the company’s earnings will increase by 72% in fiscal 2027, followed by a 32% increase in the next fiscal year.

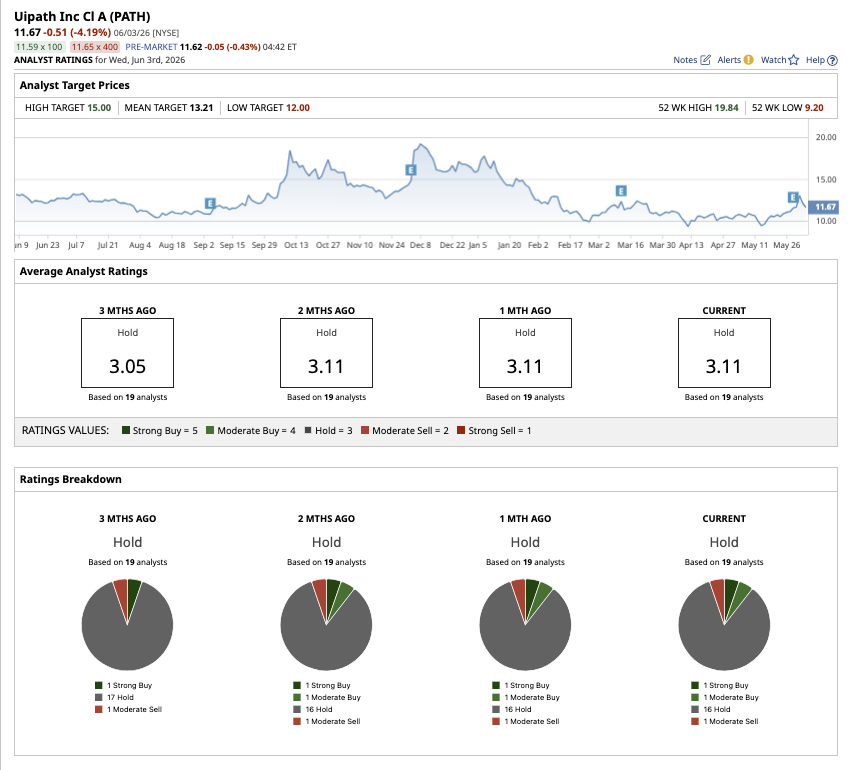

Overall, Wall Street gives PATH stock a consensus “Hold” rating, with 16 out of the 19 analysts covering the stock believing the stock may be worth holding on to now. Meanwhile, one analyst rates the stock a “Strong Buy,” while one says it is a “Moderate Buy,” with one recommending a “Moderate Sell.” PATH stock is down 28% year-to-date. But, based on the average target price of $13.21, the stock has an upside potential of 12% from current levels. Its Street-high estimate of $15 further implies the stock can go as high as 27% in the next 12 months.

On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Semiconductor%20chip%20by%20Mykola%20Pokhodzhay%20via%20iStock.jpg)

/Lululemon%20Athletica%20inc_%20storefront%20by-%20Robert%20Way%20via%20iStock.jpg)