Artificial intelligence (AI) is creating winners and losers across the software industry. Both Salesforce (CRM) and ServiceNow (NOW) have built deep ties with large enterprises, but one is positioned better to leave the other behind in the enterprise AI race over the long run.

The Bull Case for Salesforce

Salesforce is primarily a customer relationship management (CRM) company. Its platform enables companies to manage relationships with existing and prospective customers.

The company’s Agentforce platform delivered annual recurring revenue (ARR) over $1 billion. Meanwhile, Salesforce's AI and data business reached $3.4 billion in ARR. Total revenue in the first quarter of fiscal 2027 increased by 13% year-over-year to $11.1 billion. During the quarter, the company signed 98 deals with more than $1 million in annual contract value. Its current remaining performance obligations (CRPO), or revenue yet to be recognized, now stands at $33.6 billion. Adjusted earnings per share rose 50% YOY to $3.88.

Notably, in the quarter Salesforce processed 28.6 trillion tokens, which were then converted into 3.8 billion agentic work units. This shows that customers are using its AI products at scale, not just testing them. Salesforce's expanding ecosystem, which includes Slack, Data Cloud, Tableau, MuleSoft, and the recently acquired Informatica assets, provides the data foundation for AI agents to perform efficiently. Furthermore, thanks to a new feature called Headless 360, its platform will now be available to AI coding agents and autonomous systems.

Salesforce has long been the dominant player in the customer relationship management market. But now it is increasingly trying to become the leading platform for the emerging "agentic enterprise." Management believes AI could unlock a much larger opportunity by transforming Salesforce from just a software that merely stores information to one that can understand context, reason through problems, and act autonomously. Analysts predict Salesforce’s earnings to increase by 0.21% in fiscal 2027, followed by a 13% increase in fiscal 2028.

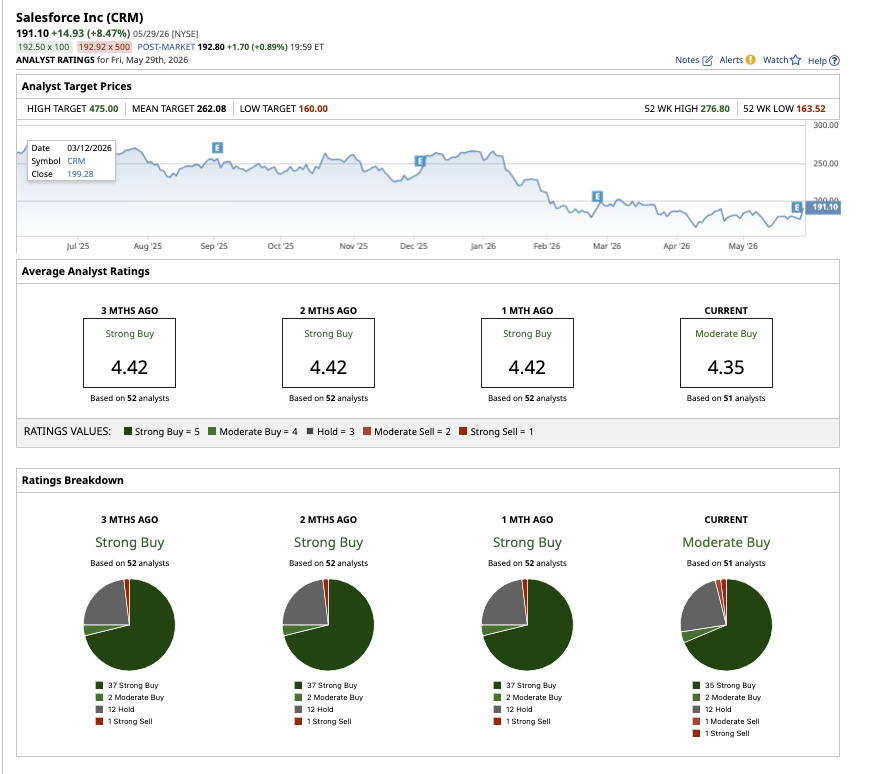

Overall, Wall Street rates CRM stock as a “Moderate Buy.” Out of the 51 analysts that cover the stock, 35 rate it a “Strong Buy,” while two recommend a “Moderate Buy,” 12 rate it a “Hold,” one rates it a “Moderate Sell,” and one suggests a “Strong Sell.” CRM stock has dipped 20% year-to-date, but based on the average target price of $262.08, CRM stock has upside potential of 25% from current levels. Its high target price of $475 suggests the stock could rally 126.6% over the next 12 months.

The Bull Case for ServiceNow

ServiceNow is a cloud software company that helps large organizations automate workflows and business processes across all departments with the help of AI. ServiceNow says its autonomous workforce can handle 90% of employee IT requests, resolving issues far faster than traditional support teams.

In the first quarter, subscription revenue increased 22% YOY to $3.67 billion. Remaining performance obligations climbed to roughly $27.7 billion, up 23.5% YOY. The company’s customer retention rate remains exceptional, with a renewal rate of 97%. The company now counts 630 customers with annual contract values exceeding $5 million. The company also added five more customers above the $50 million spending threshold compared to last year.

Its flagship AI offering, Now Assist, continues to be its star product, with the number of customers spending more than $1 million annually increasing over 130% YOY. Deals over $1 million increased more than 30% in the quarter. It closed 36 deals featuring five or more AI products, a signal that customers are rapidly embracing enterprise-wide AI deployments. While Salesforce dominates the CRM space, ServiceNow sees its CRM business as the next billion-dollar opportunity.

What ServiceNow is doing different is that it isn’t trying to replicate traditional CRM. Instead, it is building what management calls an AI-native CRM that sits on top of business workflows. For example, if a telecom company wants to launch a new product, Salesforce will assist its sales team to manage customer relationships. However, ServiceNow will help with quotations, approvals, order processing, fulfillment, service delivery, and everything else that can be automated with AI.

Notably, its sales CRM annual contract value grew more than 5x YOY, while deal counts increased more than 80%. CRM products were included in 16 of the company's top 20 deals, highlighting growing customer interest.

Interestingly, ServiceNow also isn’t trying to compete directly with AI model providers, like OpenAI, Google, Anthropic, and others. Instead, it aims to be the platform that coordinates and manages AI agents, workflows, and data throughout a company, which management describes as the "AI control tower" for enterprise operations. Analysts predict ServiceNow’s earnings to increase by 20% in 2026, followed by a 28% increase in 2027.

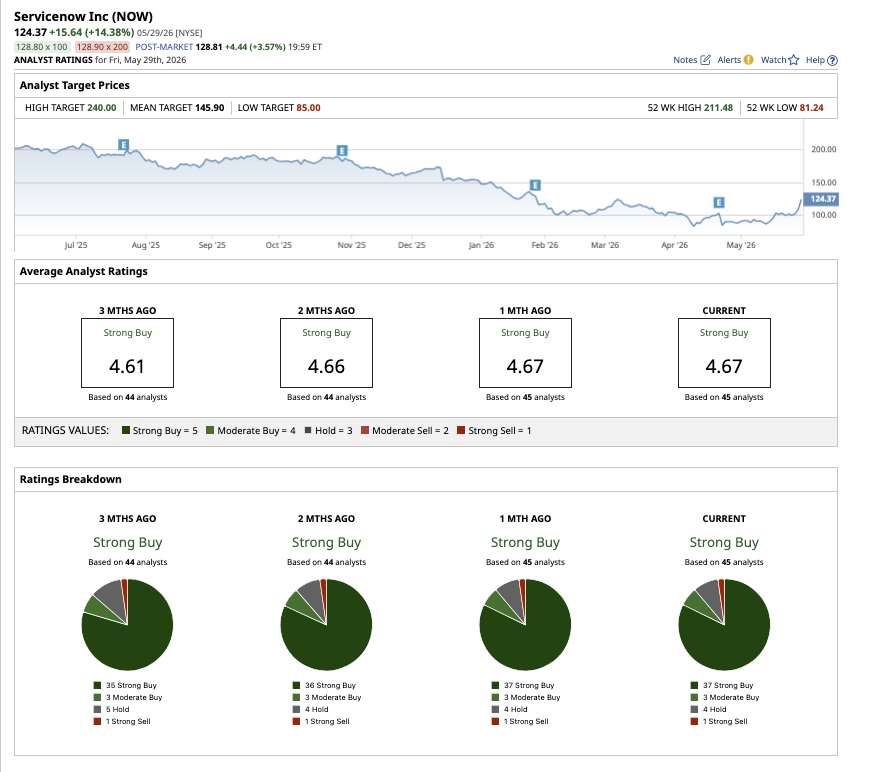

NOW stock has dipped 11% YTD, compared to the broader market gain of 11%. Overall, on Wall Street, NOW stock has a “Strong Buy” consensus rating. Out of the 45 analysts covering the stock, 37 have a “Strong Buy," three suggest a “Moderate Buy," four recommend a “Hold,” and one has a “Strong Sell.” The mean target price for NOW is $145.90, which implies 7.4% potential upside from current levels. Its high price estimate of $240 implies potential upside of 76% over the next 12 months.

Which AI Giant Is the Better Buy for the Next Decade?

Both Salesforce and ServiceNow have a similar business model of generating recurring revenue by selling cloud-based AI software to large enterprises. In this AI era, both are becoming critical software platforms most businesses cannot easily operate without. However, 10 years from now, the case for ServiceNow appears stronger. Nearly every company is under pressure to improve productivity and reduce costs with the help of AI. Thus, workflow automation could be a powerful trend over the next few years, boosting ServiceNow business dramatically.

On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Oracle%20Corp_%20office%20logo-by%20Mesut%20Dogan%20via%20iStock.jpg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Boeing%20Co_%20sign%20at%20airport-by%20sanfel%20via%20iStock.jpg)