/AI%20(artificial%20intelligence)/Hands%20of%20robot%20and%20human%20touching%20on%20big%20data%20network%20connection%20by%20PopTika%20via%20Shutterstock.jpg)

Since the start of this year, the software sector has faced a consistent sell-off. The narrative is that AI is going to wipe out a lot of enterprise software companies. The market has bought into this narrative so heavily that even a company like Salesforce (CRM) has taken a hit. The stock is down 28% YTD, trading at a massive discount. The non-GAAP forward P/E of 13.5x is nearly half the IT sector average forward P/E. A stock that led its peers now finds itself trading at half its value, which says a lot about the negative sentiment.

Are things really that bad? I don’t think so. There is an opportunity to buy a great business with solid fundamentals that has become disconnected from the share price.

The assumption that AI will completely obliterate software is wrong. We recently learned how Starbucks dropped its ambitious plans to replace baristas, proving that it is easier said than done. Yes, there are certain software companies that may go out of business, but to say that a market leader like Salesforce will end up with a similar fate is wrong. In the future, companies are not going to instruct an AI agent to build a regulation-compliant, custom CRM from scratch. It is a costly endeavor that might get even costlier in the future. Instead, companies are more likely to deploy an AI layer on top of their existing systems. This, too, can be costly as the Starbucks example showed. But if executed properly, it can provide the perfect balance between cost and practicality, and I think that is where we are headed in the future.

Salesforce has a distinct role to play if the above scenario plays out. The company already has a vast customer base, which it will need to deploy AI agents in its enterprise systems. Salesforce’s Agentforce does exactly this, and has grown from 3,000 customers to over 23,000 in just five quarters. It is the fastest-growing product in the company’s history, with the company reporting in Q1 that the product had already surpassed the $1 billion annual recurring revenue (ARR) milestone. The success of Agentforce makes the stock one of the most attractive AI software stocks right now, especially after the stock price dip. However, there’s a catch.

The success of Agentforce will cannibalize the company’s core business. We’re talking about nearly $40 billion in annual revenue that will get hit, and this is what explains the negative sentiment for this market leader. In my view, this again isn’t such a big deal. As long as Agentforce is successful, it will help the company survive and then grow even faster. If that takes a few quarters, so be it.

For now, investors fear that the move away from the per-seat charging model will eat into the company’s core business. What they don’t see is that charging by usage could become even more lucrative when companies start leveraging AI agents to perform more tasks than they do through their employees today. The opportunity is there, and getting in early while the market discounts this opportunity is the best way to maximize returns.

About Salesforce Stock

Salesforce is a cloud software company that offers customer relationship management (CRM) and AI-powered business applications. Its AI-powered product portfolio includes Agentforce, Data 360, Informatica, and Slack. The company’s products help businesses manage customer services, sales, commerce, marketing, data, and analytics. The company serves a wide range of industries, such as financial services, automotive, health care, life sciences, manufacturing, and government.

Over the past year, Salesforce shares have declined by around 28%, with most of the loss occurring after a sharp pullback in early 2026. Before this decline, the stock traded largely sideways and remained relatively stable. In comparison, the iShares Expanded Tech-Software Sector ETF (IGV) declined about 4% during the same period. This indicates that Salesforce underperformed the broader software sector, primarily due to its weaker year-to-date performance.

Informatica Drives Salesforce’s Revenue Growth

The company posted its Q1 fiscal 2027 results on May 27, reporting revenue of $11.13 billion. Revenue came in above guidance, mainly supported by stronger-than-expected contributions from Informatica's on-prem business and the timing of professional services revenue. Current remaining performance obligations (CRPO) reached $33.6 billion. It posted a non-GAAP operating margin of 34.8% and a GAAP operating margin of 21.1%. During the quarter, operating cash flow totaled $6.7 billion.

Looking ahead, Salesforce raised the midpoint of its fiscal 2027 revenue guidance to $45.9 billion to $46.2 billion. Moreover, the company maintained its non-GAAP operating margin guidance of 34.3% while adjusting the GAAP operating margin guidance to 20.6% due to higher restructuring expenses. For the second quarter, revenue is expected to range from $11.27 billion to $11.35 billion.

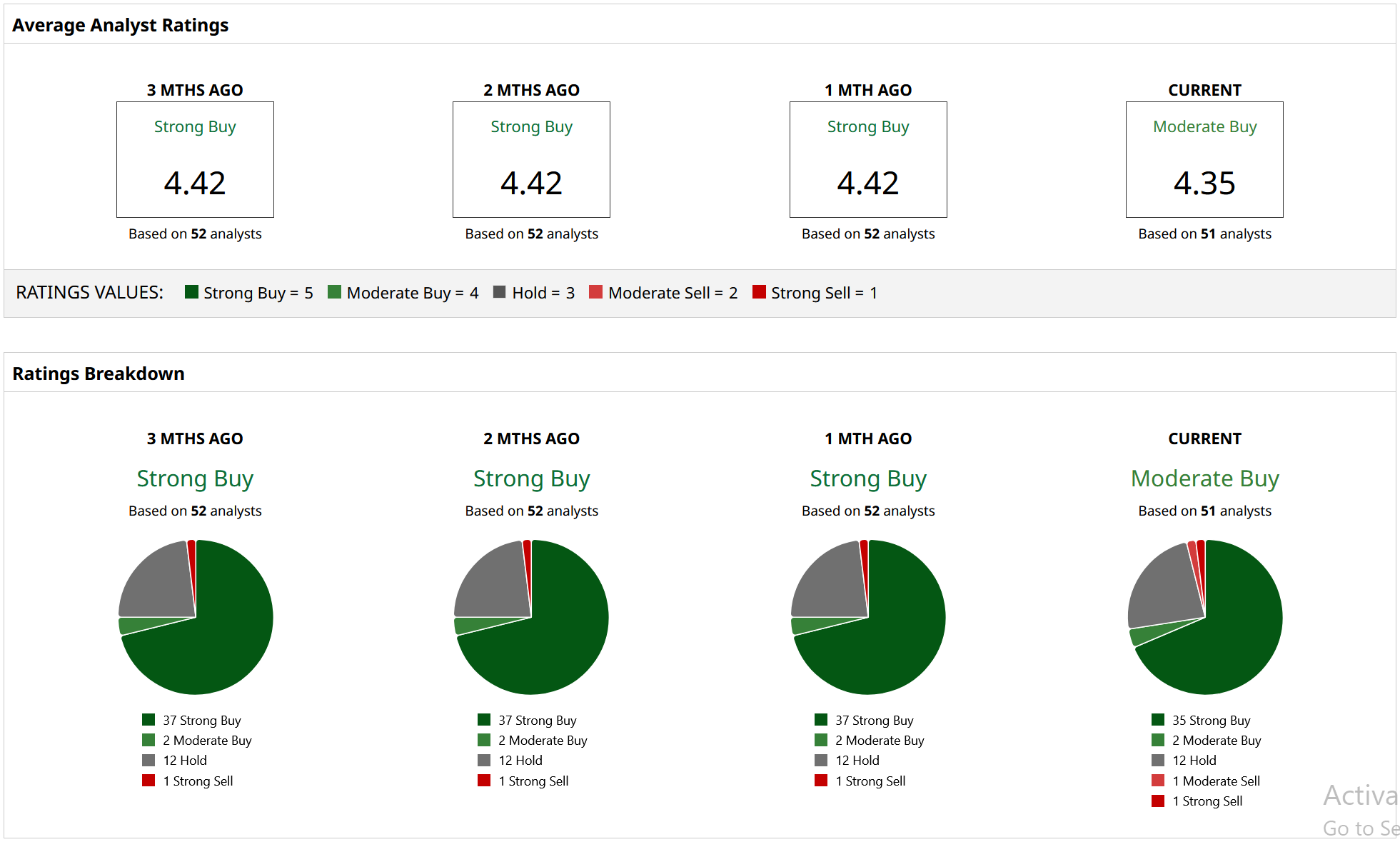

What Are Analysts Saying About Salesforce Stock?

As per recent updates, most financial services firms have maintained their ratings and price targets on the stock, suggesting there is no major shift in short-term sentiment. Barclays has reaffirmed its “Buy” rating on the shares along with a price target of $236. A day earlier, Truist Financial also reiterated its “Buy” rating and a $280 price target on the stock.

Salesforce holds a consensus “Moderate Buy” rating from 51 Wall Street analysts covering it. According to their estimates, the stock carries a mean price target of $261.77, which reflects 37% upside from the current levels. In addition to this, the highest price target of $475 stands out for investors, implying a potential upside of 149% from here on.

On the date of publication, Jabran Kundi did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.