The metals broke to new lows yesterday and have paused right at the round number this morning, with gold holding just above $4,000 and silver steadying after its drop under $60. Two tests that could have pulled them off those lows came and went recently, and neither did.

One was a blowout from Micron that eased the AI scare. The other was the inflation data the whole market was waiting on. Both passed, and the metals stayed pinned. That tells you who is in charge, and it is not the stock market. It is the dollar and the rate picture.

"The metals stopped falling and stocks bounced. Is the decline over?"

It is the natural question on a day like this, and the answer is: most likely no. This is a pause at the lows, not a turn.

Here is what eased overnight. Micron reported after the close and delivered a large beat with raised guidance, and the stock jumped sharply in after-hours trading. That report was the test for whether the AI selloff that drove Monday and Tuesday would resume, and it calmed it instead. Stocks, copper, and bitcoin are green this morning as a result. The chip panic that spilled into the metals earlier in the week has, for now, reversed.

And the metals did not bounce on the relief. Think about what that means. The thing many assumed was dragging them lower, the stock selloff, eased, and gold and silver did not rally. Yesterday I showed the decline had decoupled from the equity selloff by watching the metals fall while stocks rose. Today shows the same thing from the other side. The stock scare lifted and the metals stayed pinned, because what is pressing them is the dollar and the rate picture, not what the Nasdaq does. Removing the stock fear does not remove the dollar.

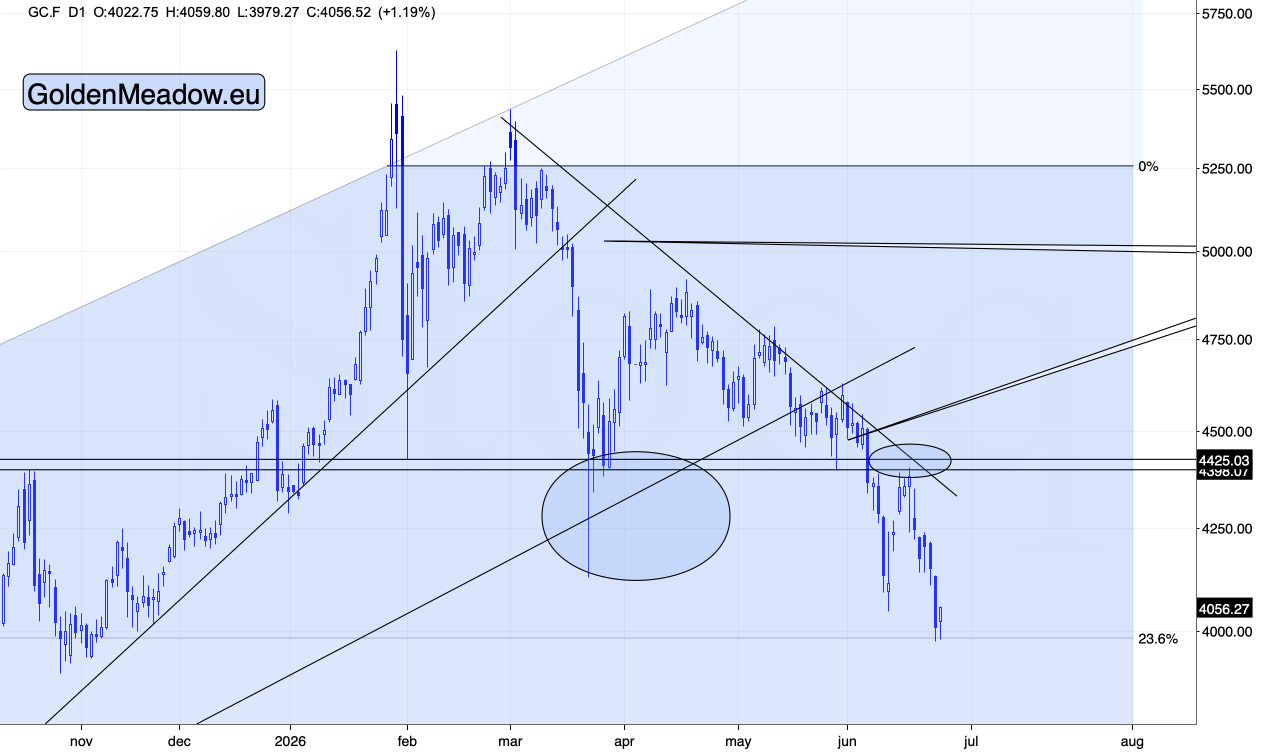

The USD Index is simply taking a breather today. It’s not declining and this is the key thing. The weaker resistance of 102 is just ahead, and the stronger one at 102.87 is further up. I think that when the USD Index moves toward 102.87, the precious metals might slide in a truly profound way. More on that in the full version of this analysis.

The inflation test came in, and it gave the metals no out

The number that could have rescued the metals was this morning's PCE, the Fed's preferred inflation gauge. The only outcome that would have helped them was a soft, downside surprise, the kind that weakens the hike case and lets the dollar slip. It did not come. Core PCE rose to 3.4% over the past year, in line with expectations and a tick above the prior 3.3%, with the monthly pace steady at 0.3%. Inflation is not falling. It is sticky, and it ticked higher.

The rest of this morning's data pointed the same way. First-quarter GDP growth was revised up to 2.1% against the 1.6% expected, and weekly jobless claims fell to 215,000, below the 225,000 the market looked for. The economy looks solid and the labor market looks tight. None of that gives the Fed a reason to ease. If anything, it strengthens the case for the hike already priced at close to 90% odds by year-end, with the short end of the Treasury curve at its most hawkish since February.

So the metals faced the one event this week that could have handed them a dovish escape, and the data shut the door on it. The reaction tells the story. Gold barely moved, the dollar barely moved, and the metals held at their lows. A market that does not rally on its best remaining hope is a market that has run out of reasons to go up.

The AI trade bought time, not a reprieve from the larger problem

One note on Micron, because it matters for the bigger picture even though it does not move the metals today. The beat was real and the demand is real, but look at how the company is paying for it. Micron raised its capital spending plan for this year and signaled a substantial further increase next year. The memory makers are pouring more money into the boom, not less. That is the over-extension I have written about, the spending that runs ahead of the returns. A blowout quarter buys the AI trade more time. It does not resolve the imbalance underneath it, and when that imbalance corrects, the metals will feel it through the liquidity channel.

As for Iran, it has gone quiet, oil is falling again, and the war premium keeps draining. A market still pricing real conflict risk does not let crude slide three days running. The loose ends remain, Lebanon among them, but they are not what is driving this tape.

Technically Speaking

We have a small rebound in gold.

From the technical point of view, it looks like a small verification of the breakdown below the early June low – nothing more.

I’ll skip the parts of the analysis about silver, mining stocks and specific profit-take levels, but I’d like to share with you one insight regarding the upcoming rebound. Namely, I’ll share with you why I think gold is likely bounce more than silver and miners. And that’s connected with how one wants to benefit from the rebound – especially if one is a more advanced trader.

For more advanced traders – if you’re considering using options for the rebound, gold might be the top market for this. Before I provide you with reasons, I would like to write in advance that I will deliberately not provide details for the option trade, because if one needs that from me, it means that they are actually not an advanced trader and would be better off not using options at all. Leveraged ETFs provide bigger bang for the buck as well and while they still carry risk, it’s not as huge as the one involved in option trading.

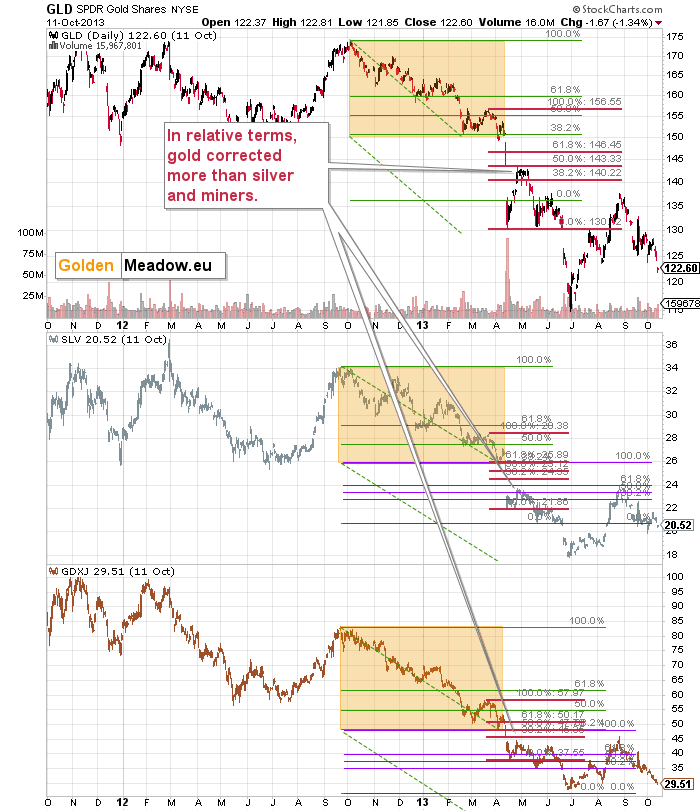

Having said that, the reason is present on the charts featuring how gold, silver, and mining stocks behaved after the sharpest part of their declines in 2008 and 2013.

Back in 2013, GLD corrected 50% of the slide, while SLV and GDXJ didn’t manage to correct even to the 38.2% Fibonacci retracement.

In case of the 2008 decline, we had two corrections. It’s obvious that the second one (late-September one) was way bigger in gold than in silver or miners, so I’m not even marking that on the chart.

The thing that I did mark is the initial, smaller correction. Again, in relative terms, it’s biggest in case of gold.

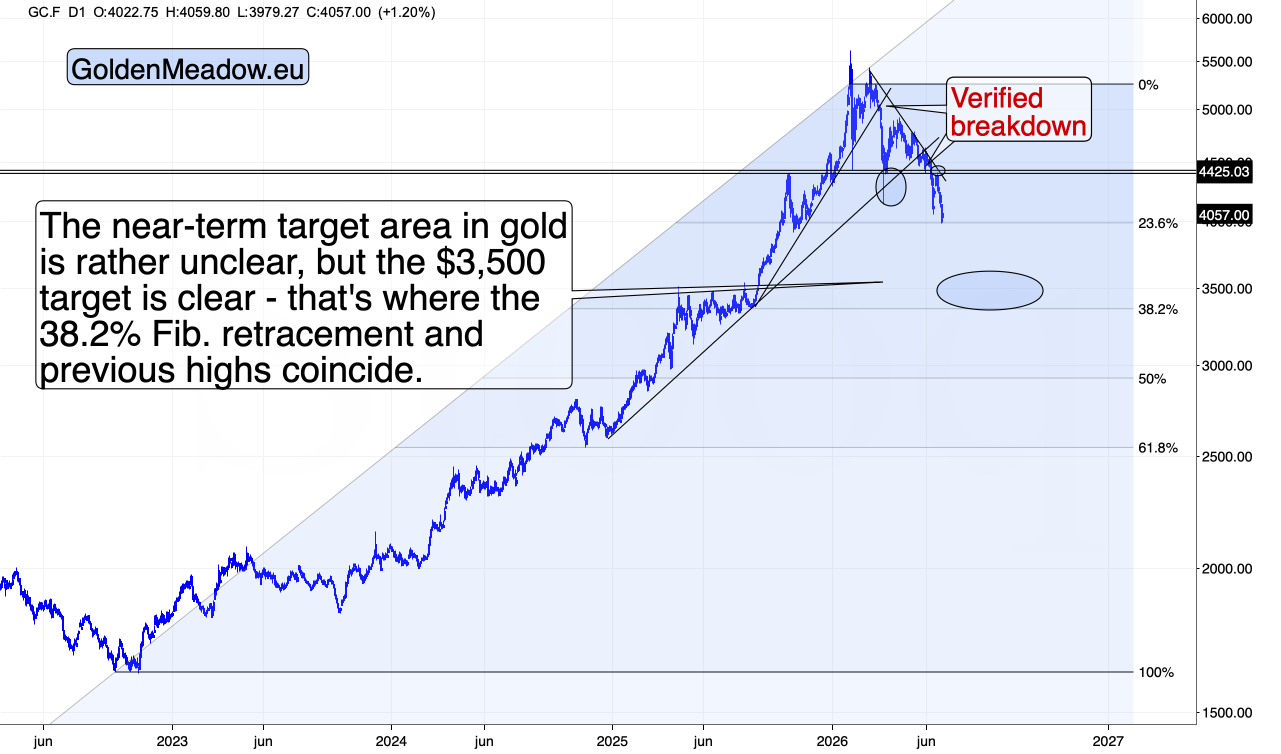

Finally, I’d like to emphasize that at this point it seems that gold will move below $3,500 during the final part of its slide, but I will be able to provide you with more precise targets only after the upcoming rebound. This extends to providing more precise targets for silver and mining stocks. The next bottom and the next corrective top will be important data points that will allow me to elaborate on the analogies and make much better forecasts compared to what I might come up with now. In other words, I need to see if gold indeed slides to $3,500 when USD approaches 102.87, or if something else happens.

Will gold keep magnifying USD’s moves?

Will miners start to be strong on a sustainable basis?

Will stocks finally slide, and if so, how will the precious metals market react?

Those are the questions that we have no replies to and we should have them before making reasonable forecasts for the PMs and miners.

But in general, the reason why I expect gold to eventually move below $3,500 is that it’s already close to $4,000 while the USD Index has barely broken above 100. The latter has much more room to rally, so I see a lot of bearish pressure on the precious metals market beyond a move to $3,500 in gold.

If you’ve been following my analyses and you’re making money on this decline – congratulations.

Thank you for reading my today’s free analysis. More details follow for Gold Trading Alert / Diamond Package subscribers. You will find more information on GoldenMeadow.eu

If you're not ready to subscribe yet, I encourage you to sign up for my free gold newsletter today.

Thank you.

Sincerely,

Przemyslaw K. Radomski, CFA

/A%20Palantir%20sign%20displayed%20on%20an%20office%20building%20by%20Poetra_RH%20via%20Shutterstock.jpg)

/Bundle%20of%20optical%20fiber%20cables%20with%20lights%20by%20volff%20via%20Adobe%20Stock.jpeg)