Summertime is finally here, which means it's time for baseball, barbeques, and beverages. But in 2026, it's also time to break out the credit card as sky-high prices on commodities like oil and beef are squeezing consumers.

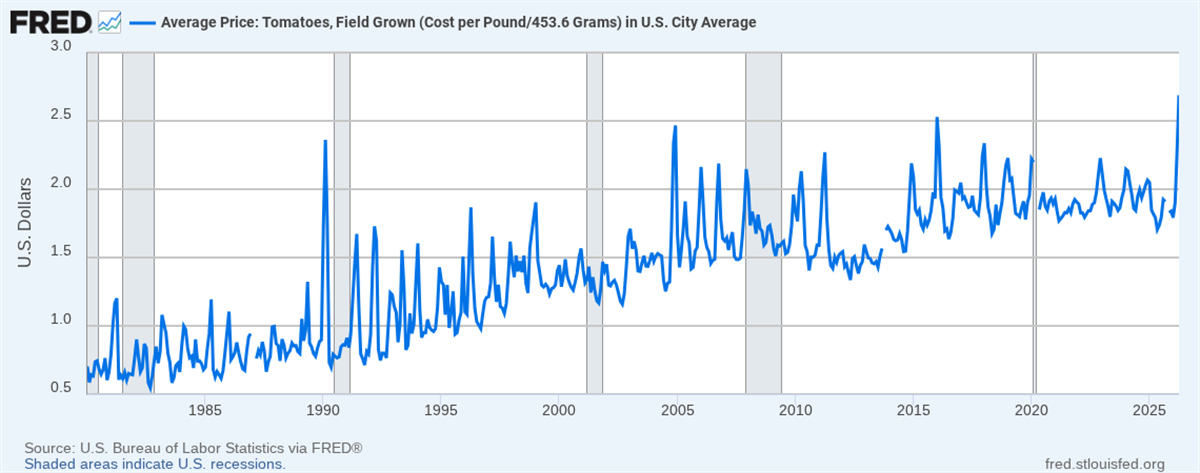

And if you’ve been to the produce section lately, you may have experienced another shock. Tomato prices have soared to their highest level ever, and the acceleration appears to be gaining intensity.

The tomato price spike happened rapidly this spring due to a confluence of factors. According to the Bureau of Labor Statistics, prices per pound leaped to $2.69 in April, an increase of nearly 40% year-over-year (YOY) and the highest reported figure since 1980.

A drastic price spike like this usually isn’t caused by a single event, and tomatoes are currently facing a three-pronged storm:

Supply: Mother Nature will always have the biggest influence over fresh crops like tomatoes, and a poor 2026 growing season shoulders significant blame for the current predicament. Unusually cold weather in Florida, combined with a wet growing season, stunted stifle harvests this year, and now these shortages are being felt in the consumer staples sector.

Transportation: The war in Iran rears its ugly head again, as soaring diesel prices are making it more expensive to transport fresh tomatoes. Unlike commodities such as oil or gold, tomatoes are highly perishable. They must be transported by truck at timely intervals, which means producers must pay the elevated costs or risk spoiling their product. Tomatoes also can’t be hedged in the futures market like other agricultural commodities, such as grain or sugar, so buyers are completely exposed to the spot price.

Tariffs: As tomato consumption grew, so did the supply of imports. Domestic producers account for only 30% of the total supply, and a 2025 Texas A&M study found that about 90% of imported tomatoes come from Mexico. But that didn’t stop the Trump administration from slapping a 17% tariff on fresh tomatoes imported from Mexico on the grounds of unfair trade practices. The tariff was initiated last July after the growing season had mostly concluded, so consumers are feeling more of the effect this year as price increases are passed on.

The tomato is one of the most consumed vegetable (yes, vegetable) on the planet, so plenty of public companies have exposure to it. But two companies stand out for the wrong reason: both were already facing business headwinds before tomato prices took off, and higher input costs could add more pressure to margins at a time when pricing power looks limited.

The Campbell’s Company: Massive Guidance Cut Underscores Structural Breakdown

The Campbell’s Company (NASDAQ: CPB) is more than just soups now.

The Meals and Beverages segment produces Prego, V8, Pacific Foods, Campbell's Soup, and the recently acquired Sovos Brands, featuring the premium Rao's sauces.

The Snacks division owns Pepperidge Farm, Lance, Cape Cod, and Snack Factory. So far, 2026 has been a messy year for both segments.

The company slashed its fiscal 2026 EPS guidance by 26% during its Q2 earnings report in March, while snack margins were down 7%.

Snacks are facing headwinds from GLP-1s and consumer tradedowns, while the Rao’s acquisition looks increasingly ill-advised as consumers balk at $9 jars of pasta sauce.

The chart is ugly as well, with the stock down around 20% in the last three months and facing resistance at the 50-day moving average. Don’t let the false breakout fool you, either. The last time the stock poked its head above 50 on the Relative Strength Index (RSI), it resulted in a massive washout just a few sessions later.

Conagra Brands: Tomato Exposure Runs Deep Through Product Offerings

Conagra Brands Inc. (NYSE: CAG) is the $6 billion firm behind a variety of tomato-infused consumer brands like Hunt’s, RAGU, Healthy Choice, Chef Boyardee, Bird's Eye, and more.

Unlike Campbell’s, Conagra actually reported organic sales growth over 2% in its fiscal Q3 2026 earnings report in April, but plummeting margins offset the headline numbers.

Operating margins declined by 213 basis points in the period, and the company expects cost of goods sold (COGS) inflation of 7% in the fiscal year.

Additionally, free cash flow was cut nearly in half from the prior year, which makes the current almost 11% dividend yield look like a bright red warning sign.

Also like CPB shares, CAG experienced a brief bull trap in February, where the stock briefly crested the 50-day and 200-day moving averages for the first time in over a year. But this rally was short-lived, and the stock quickly resumed its downward momentum with steady resistance at the 50-day moving average. The RSI is also in bearish territory but hasn’t yet reached oversold status, so there’s likely plenty of downside ahead before any recovery is attempted.

Where Should You Invest $1,000 Right Now?

Before you make your next trade, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis.

Our team has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and none of the big name stocks were on the list.

They believe these five stocks are the five best companies for investors to buy now...

The article "Tomato Prices Are Spiking, and These 2 Food Stocks Could Feel the Squeeze" first appeared on MarketBeat.

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Semiconductor%20chip%20by%20Mykola%20Pokhodzhay%20via%20iStock.jpg)

/Lululemon%20Athletica%20inc_%20storefront%20by-%20Robert%20Way%20via%20iStock.jpg)