/Uber%20Technologies%20Inc%20logo%20outside%20offices-by%20Sundry%20Photography%20via%20iStock.jpg)

Uber Technologies (UBER) stock closed higher on June 1 following a joint announcement with an Israeli artificial intelligence (AI) startup Autobrains and Nvidia (NVDA), outlining a robotaxi rollout in Munich.

The initiative will integrate UBER’s ride-hailing platform with Autobrains’ autonomous driving capabilities and NVDA’s Drive Hyperion system, which is engineered for Level 4 autonomy.

The program, structured as an “OEM-agnostic” model, is designed to scale across multiple vehicle platforms and urban markets over time.

Despite the recent gains, UBER shares remain down nearly 20% versus their year-to-date high.

Significance of Autobrains Deal for Uber Stock

UBER unloaded its self-driving business to Aurora Innovation in 2020 and has since pivoted to an asset-light model — working with partners instead of building the autonomous driving technology in-house.

The Munich program is a clean extension of that playbook. Autobrains’ tech is designed to operate on standard automotive sensors and compute systems to cut deployment costs and boost scalability.

That’s a key advantage for UBER as it tries to roll out robotaxi services economically across cities.

According to CEO Dara Khosrowshahi, the company is targeting autonomous vehicle services in 15 cities by year-end, calling it “another trillion-dollar total addressable market.”

UBER stock rallied on Monday because the Autobrains deal, plugging directly into that roadmap, signals the firm’s European AV ambitions are moving from aspiration to execution.

The Autobrains deal, plugging directly into that roadmap, signals UBER’s European AV ambitions are moving from aspiration to execution.

Why Else Are UBER Shares Attractive in 2026?

UBER’s record operating income of $1.9 billion in the latest reported quarter and its guidance for at least 18% constant-currency growth in gross bookings in Q2 make it a compelling buy.

The company repurchased about $3 billion worth of its shares in the first quarter, which reinforces the case for multiple expansion.

At the time of writing, UBER shares are going for 24x forward earnings — a reasonable valuation given the firm’s rapid expansion into the rather huge robotaxi market.

Plus, Uber One has surpassed 50 million subscribers, and the ads business is running at a $2 billion annualized revenue run rate, making UBER even more attractive as a long-term holding in 2026.

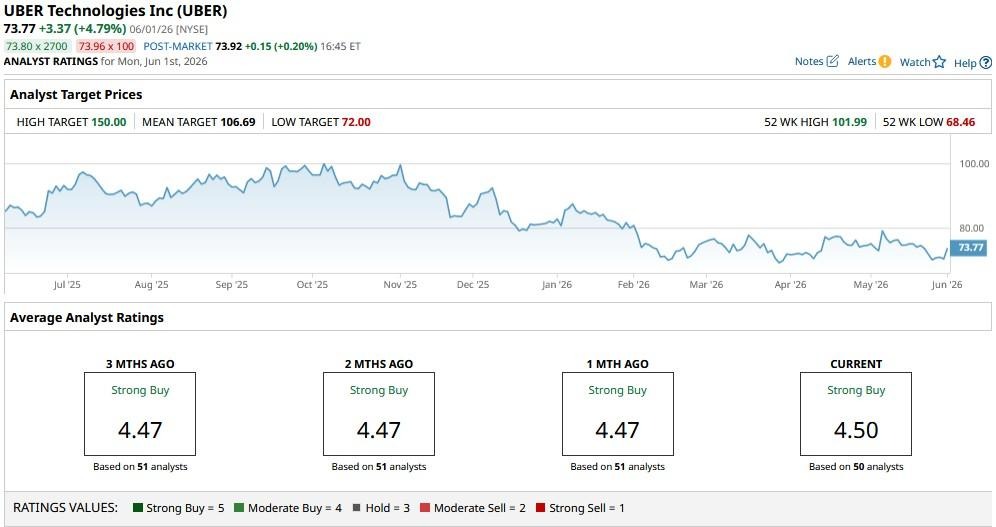

What’s the Consensus Rating on Uber Technologies?

While UBER shares currently sit below their major moving averages (MAs), indicating a strong downtrend, Wall Street remains bullish for the next 12 months.

The consensus rating on Uber Technologies is set at “Strong Buy,” with the mean price objective of nearly $107 signaling potential for another 45% upside from here.

On the date of publication, Wajeeh Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Alphabet%20Inc_%20and%20Google%20logos%20by%20IgorGolovinov%20via%20Shutterstock.jpg)

/Technological%20process%20of%20soldering%20chip%20components%20on%20PCB%20board%20by%20I%20Viewfinder%20via%20Adobe%20Stock.jpeg)