Costco (COST) split speculation is getting louder as the warehouse club keeps trading near record territory. The stock has been one of 2026’s standout defensive names, helped by investors leaning into retailers that can keep traffic steady even when consumers are careful with spending.

Costco’s share price has pushed above the $1,000 mark, which naturally fuels talk of a split, but that is more of a market psychology story than a business story. Costco last split its stock in 2000, and the recent chatter does not change the company’s operating outlook or earnings power.

Why investors keep buying Costco stock?

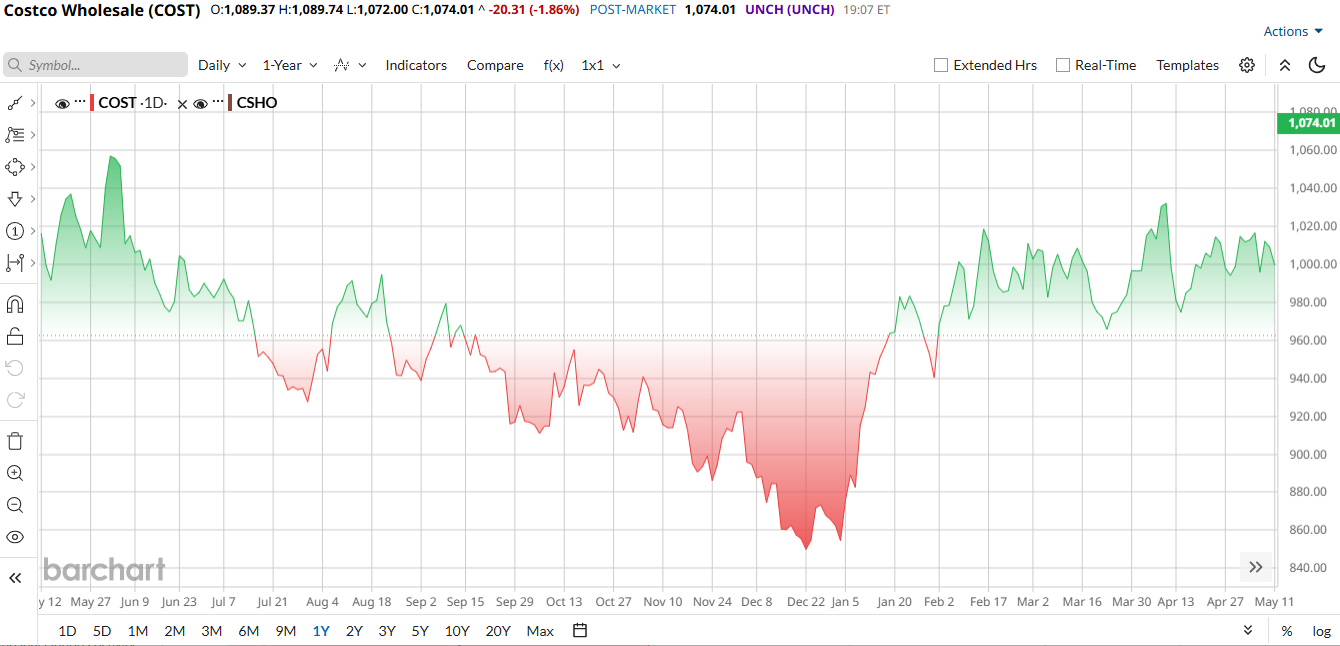

Costco shares have risen about 19% year-to-date in 2026 and recently touched a new high near $1,096, even after a modest pullback on May 20. The move has been driven by the same mix that has supported the stock for years: steady membership income, resilient traffic, and demand for value as shoppers remain price conscious. Costco also continues to look like a relative winner in a defensive retail tape, with investors favoring businesses that can hold margins without leaning too hard on promotions.

The problem, as always with Costco, is price. Barchart shows the stock trading at a trailing P/E of 56x, significantly higher than the sector median of 16. By any normal retail standard, COST is expensive, and investors are paying for consistency, not cheapness.

The Split Talk Is Really About Psychology

A split would not change Costco’s fundamentals, but it could change how the stock trades around the edges. At more than $1,000 a share, COST is increasingly expensive for smaller investors and can feel psychologically stretched even when the business is still performing well. That is why split speculation tends to show up when the stock runs hard.

The company’s business model also supports the case for a split narrative: membership fees, recurring traffic, and a large base of loyal shoppers give Costco a steady earnings engine that keeps the stock in the market’s good graces. Recent results showed the business remains strong, while a stock split would mostly be a liquidity and accessibility story rather than a business catalyst.

Latest Quarter Showed Costco Still Has Momentum

Costco’s most recent quarter, reported on March 5, showed that the business is still delivering. Revenue came in at $69.6 billion, up from a year earlier, while adjusted earnings were $4.58 a share, both above expectations. Same-store sales rose 6.6%, and membership fee revenue continued to expand, helped by the 2024 fee increase. Management also said it would pass tariff-related savings back to shoppers if refunds materialize, reinforcing Costco’s long-standing focus on value. That matters because Costco’s model depends on keeping members loyal while still leaving room for price discipline.

The bigger picture is that Costco has been mixed but still strong over the last four quarters: fiscal third-quarter 2025 revenue and EPS both beat, fiscal fourth-quarter 2025 also beat, and fiscal second-quarter 2025 had an EPS beat even though revenue missed.

In other words, the company has largely kept doing what investors pay it for, defending the top line and protecting profitability through a volatile retail backdrop.

What to Watch in the Next Report

Costco is set to report again on May 28, and the setup looks active. Barchart pegs the expected move at about 1.86%, which suggests traders are bracing for a modest but meaningful reaction. The current-quarter EPS estimate on Wall Street is $4.91, up 14.72% from a year earlier, and the next report will give investors another read on renewal rates, traffic, tariff pass-through, and how much recent store-hour changes are helping sales. Costco has also been expanding aggressively, including new warehouse openings and land buys that point to continued unit growth.

Analysts Stay Constructive, but the Upside Is Not Huge

Wall Street still leans positive, but the tone is careful. JPMorgan has called Costco a “clear market leader,” while keeping an overweight rating and a $1,110 target in a prior note. Morgan Stanley has been among the more bullish voices, while Bernstein has argued the stock can still work even after its strong run.

At the same time, some firms have warned that valuation leaves little room for error.

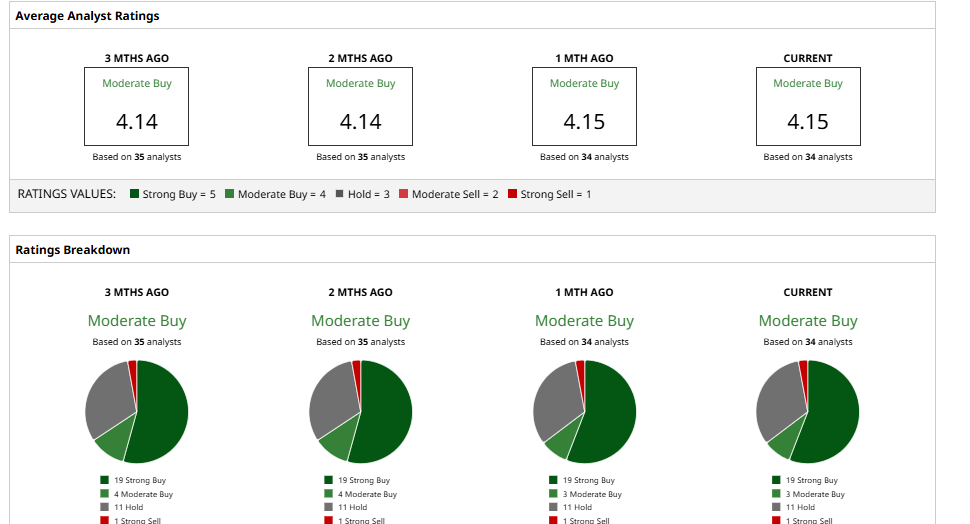

Barchart’s data shows a "Moderate Buy" consensus from 34 analysts, and other recent data points put the average target around the $1,093, implying only modest upside of around 6% from recent prices.

That is the core Costco debate right now that it has outstanding business, premium stock, and a split story that keeps growing louder because the share price keeps doing the talking.

On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20concept%20image%20showing%20a%20lightbulb%20with%20planet%20earth%20in%20a%20mossy%20green%20background%20by%20Capt_Pic%20via%20Shutterstock.jpg)

/The%20CrowdStrike%20logo%20on%20an%20office%20building%20by%20bluestork%20via%20Shutterstock.jpg)

/An%20image%20of%20a%20Tesla%20humanoid%20robot%20in%20front%20of%20the%20company%20logo%20Around%20the%20World%20Photos%20via%20Shutterstock.jpg)