/A%20photo%20of%20a%20Sandisk%20Solid%20State%20Drive%20by%20Top%20Popular%20Vector%20by%20Shutterstock.jpg)

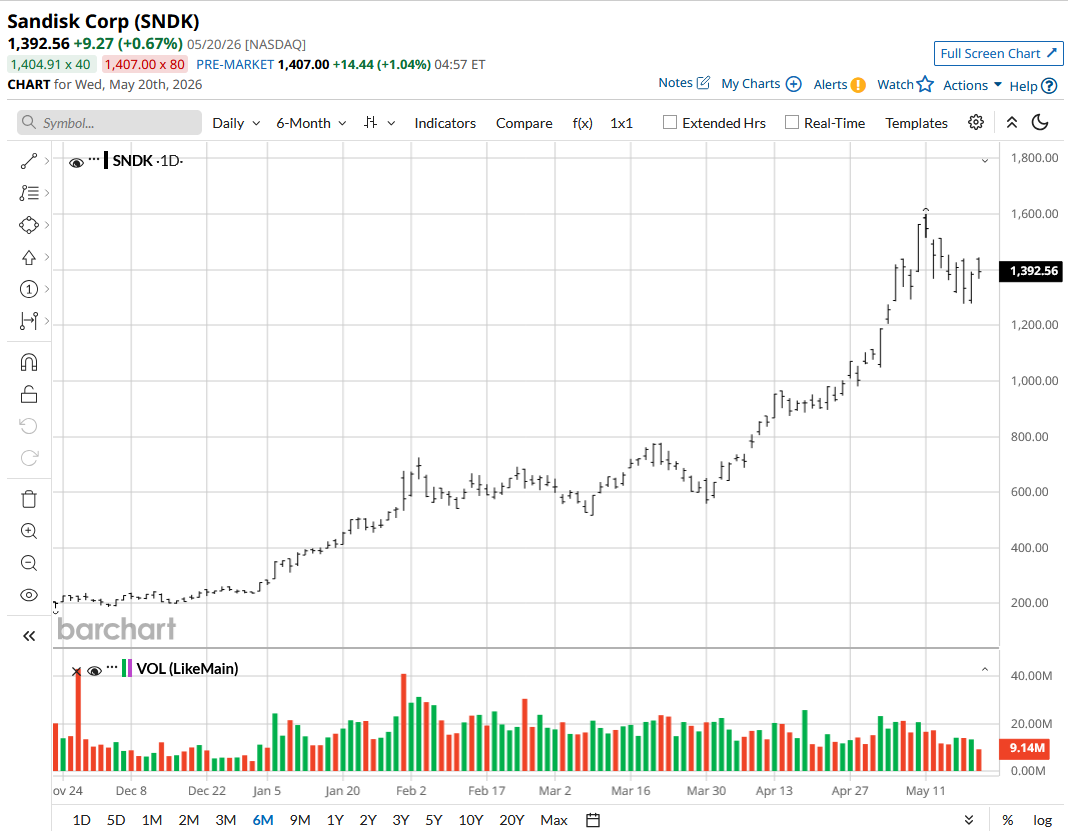

SanDisk (SNDK) stock has taken some beating in the last two weeks, after the stock nearly tripled in a matter of weeks on the increasing demand for memory chips. As is always the case, many had started calling it a dangerous rally as the stock went past the $1,500 mark. Citi analysts have now come up with their assessment of the situation, and there’s good news for the bulls: The investment firm has set a $2,025 price target for the stock, reflecting another 45% upside.

It is hard to back a stock to gain another 45% when it is already up 54% in a month. But Citi has good reasons to be bullish on the stock. The main reasons are the gross margins and the pricing power. The 80% gross margins that the company is now enjoying showcase how strong its pricing power is in the current environment. Just one year ago, the number stood at 26.4%. That’s not all. The operating expenses aren’t increasing as much as the top line is, which shows the company is managing the high demand efficiently. The profitability and the business momentum are likely to stay strong going forward, which is where Citi’s optimism comes from.

The second factor is the buyback. The company is using $6 billion to buy back its stock. Considering how high the stock is right now compared to last year, it would probably not have authorized this decision if it didn’t believe the stock was undervalued. Citi sees this as confirmation of an opportunity at current levels.

About SanDisk Stock

SanDisk operates as a manufacturer, developer, and seller of data storage devices and solutions based on NAND flash technology. The company operates across the global markets, including the United States, the Middle East, Asia, Europe, and Africa. Its product portfolio includes solid-state drives for desktops, gaming consoles, laptops, and set-top boxes.

The company’s stock is up over 3,890% in a year. These are staggering returns, and considering that analysts still believe there’s another 45% upside shows how strong the demand is. Memory stocks and the CPU usage surge have both contributed to the iShares Semiconductor ETF (SOXX) gaining 25% in the last one month. This trend could continue if SanDisk fulfils Citi’s price target.

SanDisk’s valuation metrics confirm Citi’s views. The stock’s forward P/E of 21.7x is by no means expensive, even after a 3,890% run. The 2027 and 2028 P/E multiples are hovering just above 7.5x, which is incredible for a company with such growth prospects. It must be added, though, that there is one good reason why this valuation is so attractive. Memory stocks just a few years ago almost saw their revenue get cut in half due to the cyclical nature of the industry. As a result, they did not aggressively pursue capacity expansion. Doing so now would take another three to four years, which is again a massive ask as it could become a huge drain on the company if AI takes a different advancement route and doesn’t rely on memory as much (Google’s TurboQuant algorithm being one example).

SanDisk’s Q2 Revenue Beats Guidance Range

The company reported its third-quarter fiscal 2026 earnings on April 30. Revenue for the quarter reached $5.95 billion, representing an impressive 97% sequential and 251% year-over-year increase. Growth was mainly driven by both stronger pricing and a shift toward higher-value customers. Non-GAAP gross margin came in at 78.4% with non-GAAP EPS of $23.41. Adjusted free cash flow totaled just under $3 billion, while cash flow from operations was $3.04 billion.

Looking ahead, the company expects fourth-quarter revenue between $7.8 billion and $8.3 billion. GAAP gross margin is projected to range from 79% to 81%. Non-GAAP earnings are estimated to range between $30 and $33 per share. On the expenses side, non-GAAP operating expenses are expected to be somewhere between $480 million and $500 million. Management forecasts non-GAAP interest and other income to be $10 million to $30 million.

What Are Analysts Saying About Sandisk Stock

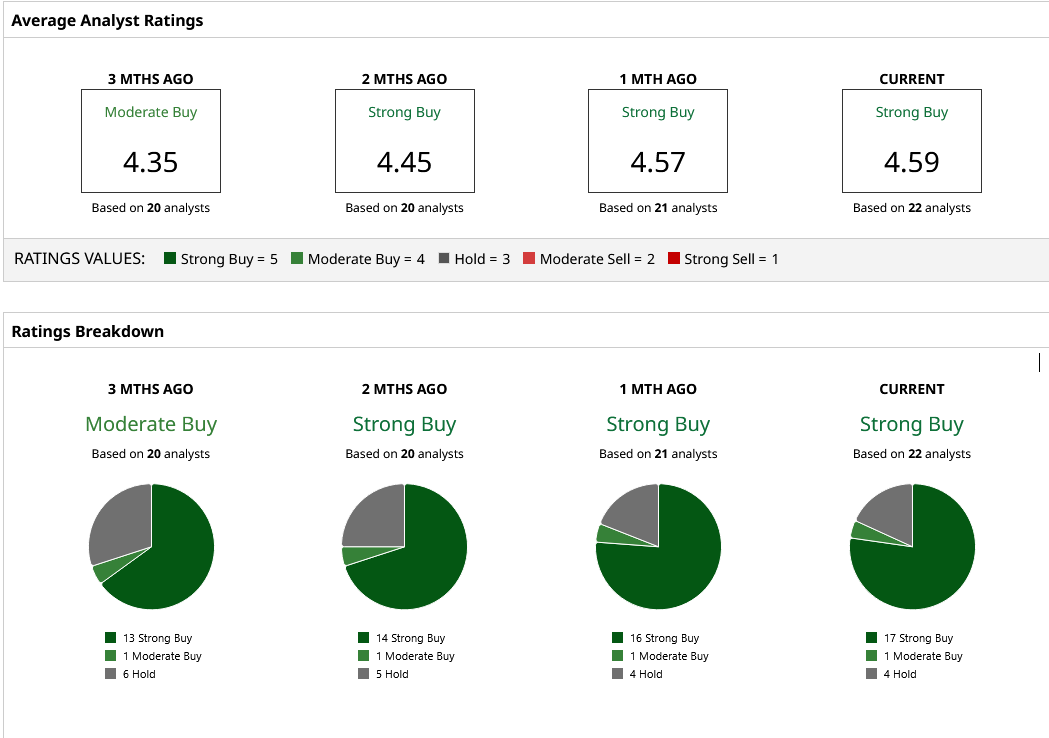

Citi isn’t the only one bullish on the stock. On May 18, Melius Research also upgraded its price target from $1,500 to $2,350, an even higher price target than Citi. According to 22 Wall Street analysts covering the stock, it carries a consensus “Strong Buy” rating. The most bullish analyst forecast sees the stock reaching as high as $2,590, almost double the current share price!

On the date of publication, Jabran Kundi did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Microsoft%20headquarters%20By%20Peter.jpeg)

/NVIDIA%20Corp%20logo%20outside%20building-by%20BING-JHEN_HONG%20via%20iStock.jpg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Amazon%20-%20Image%20by%20bluestork%20via%20Shutterstock.jpg)