Biotechnology giant Amgen (AMGN) entered what it calls its “springboard year.” The company is facing a critical transition year with patent expirations and increasing biosimilar competition pressurizing its legacy products. But the company is now ready with a fast-growing portfolio of newer medicines that appears to be reshaping its future growth profile. And Wall Street expects this dividend-paying health care stock to climb roughly 30% from current levels.

Currently, Amgen stock is trading 13% below its 52-week high of $391.29. Let’s find out if this dividend stock is a buy on the dip now.

Amgen Calls 2026 a ‘Springboard Year’

Amgen is a biotechnology company that develops and sells medicines for serious diseases, including cancer, heart disease, osteoporosis, inflammation, and rare disorders. The decline of its legacy drugs Prolia and XGEVA was obvious in the first quarter, with combined revenue down 32% year-over-year (YOY). This was driven by biosimilar competition following loss of exclusivity. However, Amgen’s newer drugs are quickly becoming the financial backbone of the business. Overall product sales increased 4% YOY.

Among Amgen’s strongest performers in Q1 was cholesterol-lowering therapy Repatha, which reported sales growth of 34% YOY to $876 million. Notably, Repatha has reported reduced cardiovascular events by 31% in "high-risk diabetes patients without known significant atherosclerosis.” The therapy also showed a nominal 32% reduction in cardiovascular death risk and a nominal 24% reduction in all-cause death. These findings suggest that Repatha has the potential to become a major long-term cardiovascular franchise.

Furthermore, its osteoporosis drug Evenity also reported 27% YOY increase in sales to $562 million. The drug now commands 65% share of the U.S. bone-builder market. Rare disease therapies grew 25% YOY to $1.2 billion, led by a 188% increase in Uplizna sales. Management believes the therapy has the potential to become the first-line and first-switch choice for generalized myasthenia gravis patients.

Amgen’s innovative oncology portfolio also reported 25% YOY increase in sales. Imdelltra has rapidly become a standard-of-care treatment in second-line small cell lung cancer. Meanwhile, Blincyto is being widely used to treat CD19-positive B-cell precursor acute lymphoblastic leukemia. Management stated the company is on track to deliver sustained long-term growth through its expanding portfolio and late-stage pipeline.

The Obesity Opportunity Could Transform Amgen

Perhaps, Amgen’s biggest long-term growth opportunity is MariTide, its experimental obesity and diabetes treatment. Amgen is trying a different approach with MariTide through weekly, every eight weeks, and 12-week dosing schedules. Management believes this could prove to be major convenience advantage for patients compared to existing obesity therapies that often require weekly injections. Additionally, Amgen also reported encouraging tolerability results through three-step dose escalation strategies, with reductions in nausea and vomiting. The company will soon begin multiple Phase 3 trials for MariTide.

The obesity market is rapidly growing, with many biotech players trying their luck with their anti-obesity drugs. While Eli Lily (LLY) and Novo Nordisk (NVO) rule the market for now, I believe the market will be huge enough to accommodate many new players with better treatments. And, if MariTide is commercially successful, Amgen might position itself to compete in one of the world's fastest-growing market.

Amgen is also using artificial intelligence (AI) across research, development, manufacturing, and operations. In the quarter, capital expenditures totaled $700 million with major investments across facilities in Ohio, North Carolina, and Puerto Rico.

Dividend Remains the Main Attraction

For income investors, Amgen’s dividend remains the main attraction with a track record of 14 years of dividend growth. Its forward dividend yield of 3.04% stands out from many large-cap health care peers. Its forward payout ratio of 43.4% also makes the dividends seem sustainable.

Importantly, Amgen’s dividend is supported by strong free cash flow generation. In the quarter, it generated $1.5 billion in free cash flow while investing aggressively in pipeline development. Amgen also increased its quarterly dividend by 6% to $2.52 per share. It also plans to repurchase shares worth $3 billion for the full year.

Should Investors Buy the Dip?

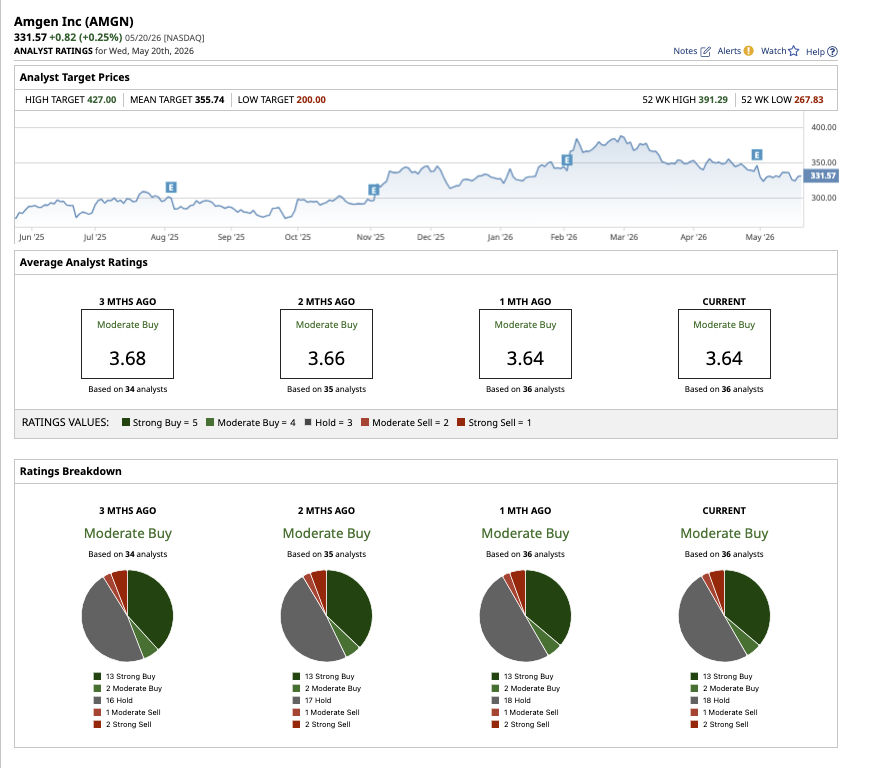

Analysts have assigned a mean target price of $355.74, which points to a 10% upside from current levels. But the most bullish estimate of $427 suggests a 26% upside. Overall, the stock is a “Moderate Buy” on Wall Street. Of the 36 analysts covering the stock, 13 rate it a “Strong Buy,” two say it is a “Moderate Buy,” 18 rate it a “Hold,” one say it is a “Moderate Sell,” and two recommend a “Strong Sell.”

Wall Street’s bullish outlook is understandable. Amgen has a built a new portfolio to outgrow the decline of aging legacy medicines over the next several years. Its diversified portfolio across cardiovascular disease, oncology, rare disease, inflammation, and obesity further strengthens its bullish case. Along with its dividends, the stock also has a defensive side as health care demand tends to remain resilient regardless of economic conditions.

Amgen is a compelling buy-the-dip opportunity if investors are willing to tolerate near-term patent-expiration pressure for long-term upside.

On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Microsoft%20headquarters%20By%20Peter.jpeg)

/Apple%20products%20on%20desk%20by%20Ake%20Ngiamsanguan%20via%20iStock.jpg)

/Nvidia%20logo%20by%20Konstantin%20Savusia%20via%20Shutterstock.jpg)