/MSCI%20Inc%20magnified%20website-by%20Mehaniq%20via%20Shutterstock.jpg)

With a market cap of around $42.4 billion, MSCI Inc. (MSCI) is a leading global provider of investment decision-support tools and services. The New York-based company serves asset managers and institutional investors through index solutions, risk and portfolio analytics, ESG and climate tools, and private capital data and workflows.

The company's shares have underperformed the broader market over the past 52 weeks. MSCI stock has surged 4% over this time frame, while the broader S&P 500 Index ($SPX) has rallied nearly 27.4%. Moreover, shares of the company are up 1.5% on a YTD basis, compared to SPX’s 8.8% gain.

Looking closer, shares of the company have outpaced the State Street Financial Select Sector SPDR ETF’s (XLF) 2.9% rise over the past 52 weeks and 5.6% fall in 2026.

MSCI shares surged 5.4% on Apr. 21 after the company reported stronger-than-expected Q1 FY2026 results, driven by robust growth across its Index, Analytics, and asset-based fee businesses. It reported revenue of $850.80 million, up 14.1% year over year, while organic revenue growth reached 13.3%. Much of the growth was fueled by strong demand for the company’s index products and analytics solutions, as well as higher ETF-linked asset-based fees. Adjusted EPS came in at $4.55, up 13.8% year over year, comfortably ahead of analyst expectations.

For the fiscal year ending in December 2026, analysts expect MSCI’s adjusted EPS to grow 13.5% year over year to $19.62. The company’s earnings surprise history is promising. It beat the consensus estimates in the last four quarters.

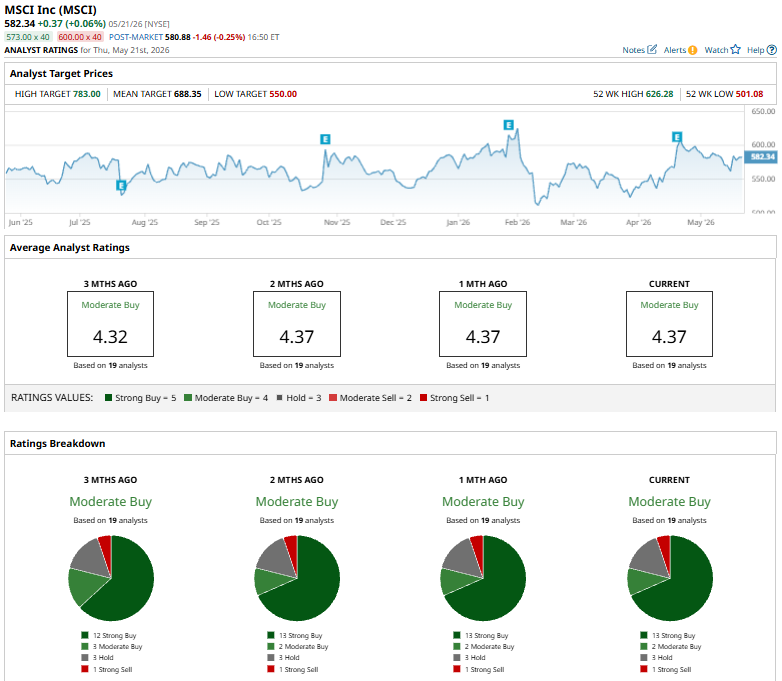

Among the 19 analysts covering the stock, the consensus rating is a “Moderate Buy.” That’s based on 13 “Strong Buy” ratings, two “Moderate Buys,” three “Holds,” and one “Strong Sell.”

The consensus is bullish than three months ago when the stock had 12 “Strong Buy” suggestions.

On Apr. 22, UBS raised its price target on MSCI to $720 from $710 while maintaining a “Buy” rating, following the company’s strong first-quarter performance. The firm highlighted that MSCI’s Index subscription run-rate growth returned to double digits for the first time since Q1 2023, reflecting improving business momentum. Management attributed the strong results to better execution, ongoing product innovation, and increased adoption of AI tools.

The mean price target of $688.35 represents an 18.2% premium to MSCI’s current price levels. The Street-high price target of $783 suggests a 34.5% potential upside.

On the date of publication, Kritika Sarmah did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Intuit%20Inc%20logo-by%20Mojahid%20Mottakin%20via%20Shutterstock.jpg)

/A%20photo%20of%20a%20Sandisk%20Solid%20State%20Drive%20by%20Top%20Popular%20Vector%20by%20Shutterstock.jpg)