/PayPal%20Holdings%20Inc%20sign%20on%20building-%20by%20Sundry%20Photography%20via%20Shutterstock.jpg)

The digital payments space has gotten a lot tougher. Big players like Visa (V), Mastercard (MA), Stripe, Adyen (ADYEY), and Revolut are all fighting harder for market share, and that has put pressure on older platforms. The broader fintech space has struggled as well, with the Global X FinTech ETF (FINX) down 18% over the past year. Still, PayPal (PYPL) has had an even rougher run, falling almost 40% over the past 52 weeks while the S&P 500 ($SPX) has gained 25%.

That is part of why Michael Burry’s increased stake in PayPal stands out. The infamous investor opened a roughly 3.5% position in PayPal in April 2026 at about $49 per share, then added to it in the first quarter. Burry has said the fintech selloff looks more like a technical issue than a sign that the businesses are broken. He also sees PayPal as less exposed to the private credit stress that he believes helped create this setup. With PYPL stock still down more than 80% from its 2021 all-time high, Burry is betting the market has become too negative on the name.

Is Michael Burry spotting a real bargain in PayPal? Or is this just another cheap stock that will stay cheap? Let’s take a closer look.

Inside PayPal’s Latest Financials

PayPal runs a global payments platform that lets people and businesses send, receive, and process money, from online checkout to peer-to-peer transfers and merchant services.

PYPL stock has had a tough run, down 39% over the past 52 weeks. Shares are also down roughly 24% year-to-date (YTD).

That shows up in the valuation, too. The forward price-to-earnings (P/E) ratio of 8.3 times comes in below the sector average of about 10 times.

Even so, PayPal still pays a quarterly dividend of $0.14, giving it a 0.64% yield, with a low 5% payout ratio that leaves room to reinvest. The business is still large in scale, bringing in $33.2 billion in annual revenue and $5.23 billion in net income.

In Q1 2026, revenue grew 7% year-over-year (YOY) to $8.4 billion, while total payment volume rose 11% to $464 billion, showing steady activity on the platform. Profitability was more mixed, with GAAP operating income down 3% and margins slipping to 17.8%. Adjusted EPS still came in slightly higher at $1.34, up 1% YOY, as total transactions increased 7% to 6.5 billion. Cash flow remained solid, with $900 million in free cash flow and $1.7 billion on an adjusted basis, even with the pressure on margins.

What’s Driving PayPal’s Next Phase?

PayPal has signed a multiyear deal with the Seattle Seahawks, becoming the team’s official “fan-to-fan” payments and exclusive digital ticket partner. It is the company’s first direct deal with an NFL team.

Through its integration with Ticketmaster, fans can pay with PayPal more easily, especially for tickets and game-day experiences. This pushes PayPal beyond online shopping and into real-world, high-activity spending where users transact more often.

At the same time, the company is moving into digital advertising with PayPal Ads ID, a tool built on real transaction data from PayPal and Venmo accounts. Instead of relying on guesswork via cookies or device tracking, it uses verified user activity, which makes ad targeting more accurate across devices. With only 21% of the industry reportedly confident in current targeting methods, this gives PayPal a clearer way to make money from its data.

On the payments side, PayPal is also expanding its stablecoin, PayPal USD (PYUSD), to 70 markets. The token allows users to send and receive money faster and at a lower cost across borders. Businesses can access funds almost instantly, which helps with cash flow and reduces delays tied to traditional payment systems.

What Does Wall Street Think of PayPal Stock?

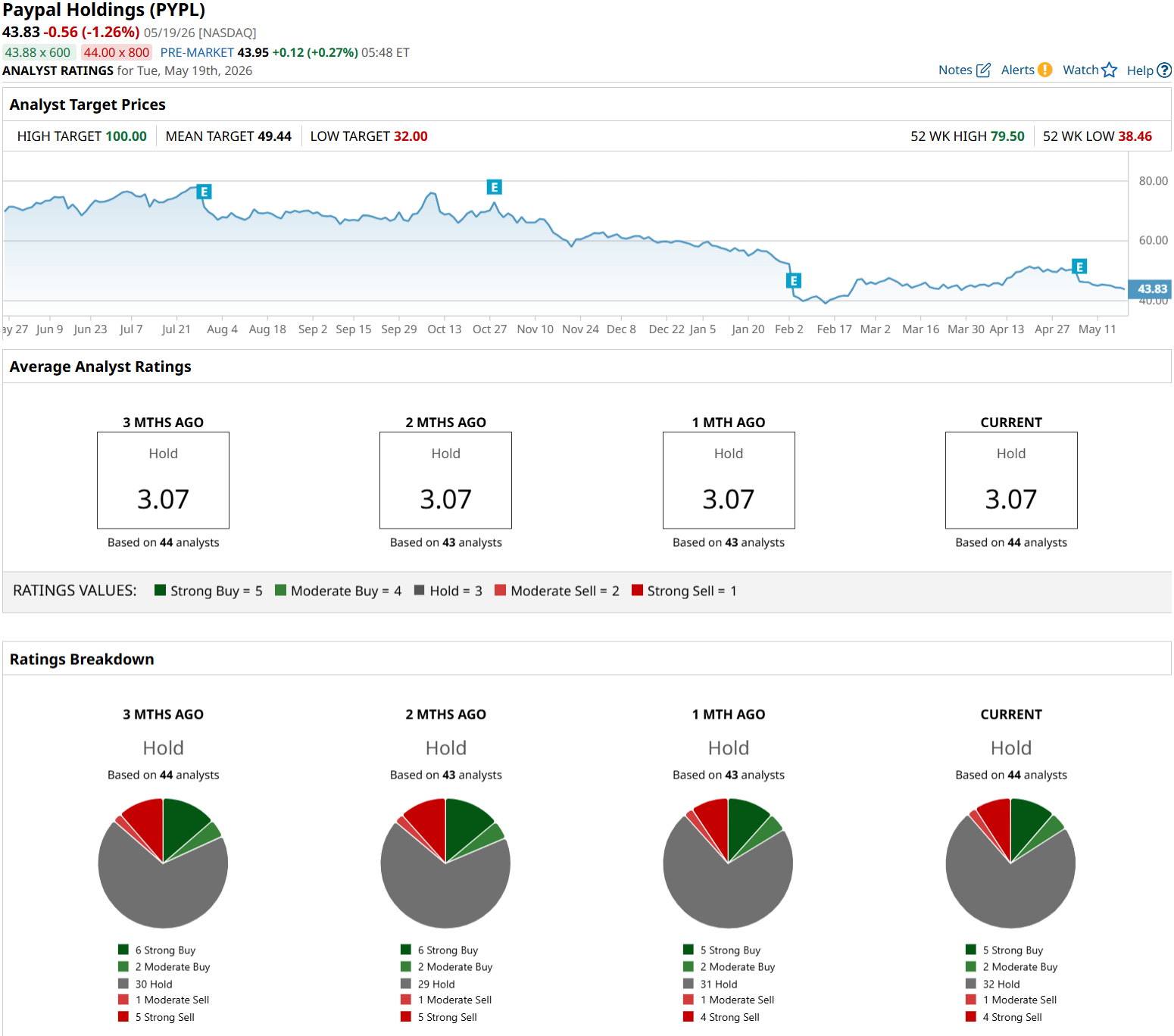

For the June 2026 quarter, analysts expect PayPal to earn $1.29 per share, down almost 8% from $1.40 a year ago. The September quarter is expected to improve slightly, with EPS of $1.35 up less than 1% from $1.34. For full-year 2026, estimates are for EPS of $5.30, almost flat compared to $5.31 in 2025.

That cautious outlook shows up in recent analyst calls. On April 27, BMO Capital analyst Andrew Bauch kept a “Hold” rating with a $52 price target, suggesting some upside but not enough to be bullish. Following Q1 results, Macquarie cut its target from $58 to $50 on May 7, pointing to concerns about how strong growth can be going forward. On May 12, Truist also kept a “Sell” rating with a $44 price target, implying PYPL stock may not have much room to run even at current levels.

Overall, based on 44 analysts with coverage, PYPL stock has a consensus “Hold" rating with an average price target of $49.44. The mean target points to about 11% potential upside from current levels.

Conclusion

Burry’s move to buy PYPL stock adds an interesting layer to the PayPal story, but it does not override the broader reality that growth is still uneven and Wall Street remains cautious. The business is stable and still generating solid cash, and the valuation is clearly compressed, which could appeal to long-term investors willing to wait. However, with earnings growth largely flat in the near term and sentiment still lukewarm, this does not look like a clear breakout setup yet. Shares will most likely trade sideways with a slight upward bias as execution improves rather than staging a sharp rebound anytime soon.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Microsoft%20headquarters%20By%20Peter.jpeg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/NVIDIA%20Corp%20logo%20outside%20building-by%20BING-JHEN_HONG%20via%20iStock.jpg)

/Amazon%20-%20Image%20by%20bluestork%20via%20Shutterstock.jpg)