/Leidos%20Holdings%20Inc%20logo%20and%20stock%20chart-by%20T_Schneider%20via%20Shutterstock.jpg)

Reston, Virginia-based Leidos Holdings, Inc. (LDOS) is one of the largest government services contractors in the United States. With a market cap of $15.7 billion, it is a defense, aerospace, information technology, and engineering company that provides advanced technology, cybersecurity, intelligence, and scientific solutions primarily to government agencies and commercial customers.

Shares of this global science and technology leader have struggled to keep up with the broader market over the past year. LDOS has plunged 21% over this time frame, while the broader S&P 500 Index ($SPX) has rallied nearly 23.3%. Moreover, in 2026, LDOS stock is down 30.2%, compared to the SPX’s 7.4% YTD rise.

Narrowing the focus, LDOS has trailed the Global X Defense Tech ETF (SHLD), which has gained 16.6% over the past year.

On May 5, Leidos reported its Q1 FY2026 results, after which the stock declined 7.8% despite the company delivering solid revenue growth, earnings expansion, and raising its full-year guidance. The market reaction appeared to reflect broader valuation concerns and investor caution surrounding acquisition-related costs and future margin sustainability.

During the quarter, Leidos generated revenue of $4.40 billion, up 4% year over year, driven by continued strength across its defense, intelligence, and digital modernization businesses. Non-GAAP EPS increased 5% to $3.13, while adjusted EBITDA reached $614 million with a healthy 14% margin. The company also delivered strong cash generation, reporting $301 million in operating cash flow and $270 million in free cash flow.

For fiscal 2026, ending in December, analysts expect LDOS’ EPS to grow 2.2% to $12.25 on a diluted basis. The company’s earnings surprise history is impressive. It beat the consensus estimate in each of the last four quarters.

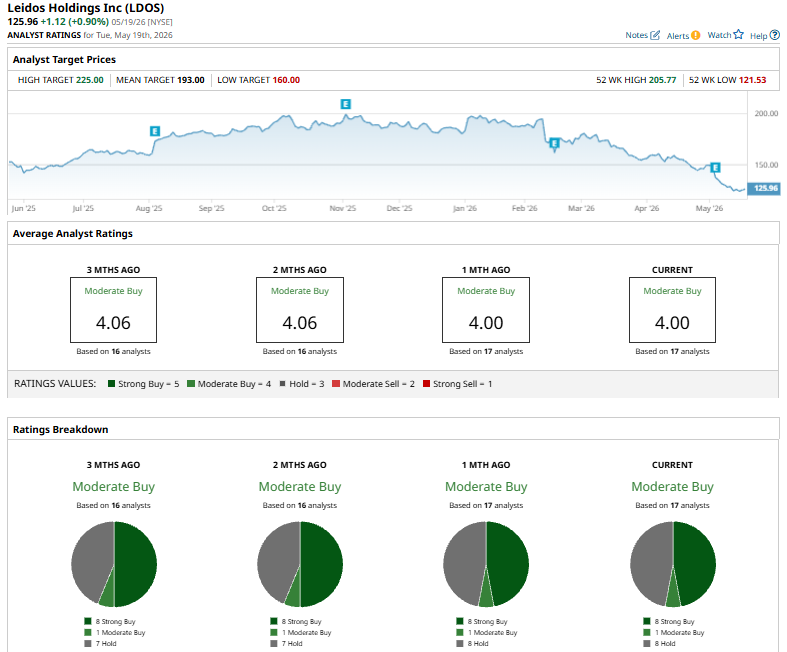

Among the 17 analysts covering LDOS stock, the consensus is a “Moderate Buy.” That’s based on eight “Strong Buy” ratings, one “Moderate Buy,” and eight “Holds.

On May 7, 2026, Citigroup analyst John Godyn maintained a “Buy” rating on Leidos Holdings but lowered the price target to $178 from $232.

The mean price target of $193 represents a 53.2% premium to LDOS’ current price levels. The Street-high price target of $225 suggests an ambitious upside potential of 78.6%.

On the date of publication, Kritika Sarmah did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Nvidia%20logo%20and%20sign%20on%20headquarters%20by%20Michael%20Vi%20via%20Shutterstock.jpg)

/AI%20(artificial%20intelligence)/Ai%20chip%20by%20Quality%20Stock%20Arts%20via%20Shutterstock.jpg)

/AI%20(artificial%20intelligence)/AI%20microchip%20by%20DesignKingBD360%20via%20Shutterstock.jpg)