/NVIDIA%20Corp%20logo%20on%20phone%20and%20AI%20chip-by%20Below%20the%20Sky%20via%20Shutterstock.jpg)

Large language models (LLMs) have dominated much of the AI debate over the last few years. Scaling token prediction and LLM training were considered reliable metrics to measure progress, irrespective of the cost. This factor played right into the hands of Jensen Huang, who makes the best GPUs in the world, a fundamental requirement for training these AI models.

As intelligent as these systems were, they were still dumb in the sense that they had to be fed data in order to become better at predicting the next token. These static datasets could only make the AI so intelligent, giving rise to the need for superlearners: AI systems that continuously learn from experience rather than static datasets.

Nvidia (NVDA) announced a new engineering collaboration with a London-based startup called Ineffable Intelligence. The startup is led by David Silver, the same man behind the success of DeepMind and AlphaGo. Nvidia is now backing the idea of building an AI that discovers knowledge through interaction rather than just pre-training. This is just another step closer to AI, and one can already imagine the kind of progress a system like this would make in fields such as drug discovery, climate control, cybersecurity, and pretty much any field that progresses based on trial and error.

Huang has already dubbed superlearners as the “next frontier of AI.” By backing Ineffable Intelligence, he is trying to secure a foothold in the technology of the future. He already did this with LLMs. Repeating the same with superlearners could provide an even bigger growth story. That’s because the continuous and real-time feedback that such systems require will test memory bandwidth and interconnects far more than the current systems do. For now, Nvidia’s Grace Blackwell will power the research performed by Ineffable Intelligence, later moving to the Vera Rubin Platform. What comes after that is anybody’s guess, but if Jensen Huang is backing it, you can bet it will be powered by his firm.

About NVIDIA Stock

Nvidia is a fabless semiconductor and AI computing company that designs GPUs, AI accelerators, application programming interfaces (APIs), and system-on-a-chip units. The company operates through the Graphics and Compute & Networking segments. Through its CUDA ecosystem, the company enables industries ranging from autonomous vehicles to scientific research by advancing AI, accelerated computing, and data center infrastructure.

Over the past year, the stock significantly outperformed the S&P 500, delivering returns of around 64.5%. In comparison, the broader index posted gains of about 24% during the same period. The strong momentum has continued this year as well, with the stock gaining approximately 18.1% year-to-date versus the S&P 500’s return of around 7.8%.

Nvidia’s valuation has come down to attractive levels, especially since the stock has had some time away from the spotlight due to the ongoing memory stocks craze, despite the broader semiconductor sector rallying. The muted returns compared to the iShares Semiconductor ETF (SOXX) have cut the stock’s forward P/E by 50% compared to its own five-year average. The market is waiting for wherever AI takes it next. If it is in the direction of superlearners, Nvidia could rewrite its own growth story once more, helping it return to the valuations of the past.

Nvidia Ended 2026 Strong

The company posted its fourth-quarter fiscal 2026 results on Feb. 25. It reported record quarterly revenue of $68.1 billion, comfortably exceeding the consensus estimate by $1.9 billion. This represents growth of 20% from the previous quarter and 73.2% year-over-year. The data center segment also recorded a record revenue of $62.3 billion, rising 22% sequentially and 75% year-over-year. On the earnings side, non-GAAP EPS for the quarter came in at $1.62, beating market expectations by $0.08.

For the first quarter of 2027, revenue is projected to be around $78 billion, compared with the analyst estimates of $72.03 billion. The company expects a GAAP gross margin of 74.9% and a non-GAAP gross margin of around 75%. GAAP operating expenses are estimated at $7.7 billion, while the non-GAAP operating expenses are forecasted at around $7.5 billion. The next earnings report comes out on May 20.

What Are Analysts Saying About NVIDIA Stock

Timothy Arcuri of UBS increased the firm’s price target on the stock from $245 to $275 and maintained a “Buy” rating on May 14. A day earlier, Bank of America Securities analyst Vivek Arya raised the firm’s price target on NVIDIA from $300 to $320 while reaffirming a “Buy” rating. The firm continues to view the stock as one of its top semiconductor picks. BofA expects AI-driven spending to stay stronger for longer.

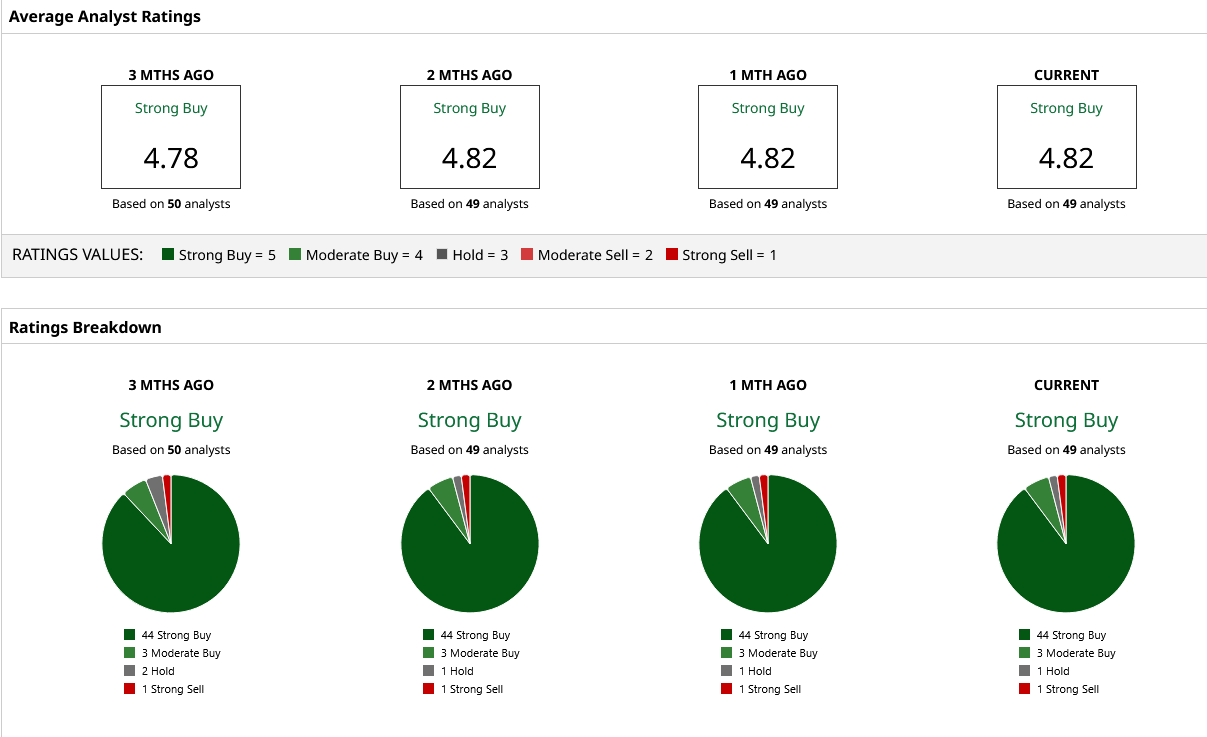

A total of 49 Wall Street analysts currently cover NVIDIA, with the stock holding a consensus “Strong Buy” rating. Based on their estimates, it has a mean price target of $274.01, implying 23% upside from here on.

On the date of publication, Jabran Kundi did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Microsoft%20headquarters%20By%20Peter.jpeg)

/Apple%20products%20on%20desk%20by%20Ake%20Ngiamsanguan%20via%20iStock.jpg)

/Nvidia%20logo%20by%20Konstantin%20Savusia%20via%20Shutterstock.jpg)