Amid anticipation, retail giant Walmart (WMT) is set to report its Q1 earnings on May 21. The tone on Wall Street is bullish for Walmart stock, with many analysts raising the price targets just ahead of earnings. These price targets upgrades imply growing confidence that Walmart might report a better-than-expected quarter, upbeat outlook and long-term growth trends. Amid the economic uncertainty, Walmart stock has surged 21.27% year-to-date (YTD), outperforming the S&P 500 Index ($SPX) gain of 7.72%.

Let’s find out what’s in store for Q1 of fiscal 2027.

Walmart Set For Another Strong Quarter

Wall Street is starting to see Walmart as one of the rare companies capable of delivering defensive stability, consistent growth, digital expansion, and rising profitability all at the same time. In the fourth quarter, Walmart reported revenue growth of 4.9%, with 12.1% increase in adjusted earnings per share. E-commerce sales surged 24% globally, driven by the company’s rapid digital expansion. For the full fiscal year 2026, Walmart’s revenue exceeded $700 billion for the first time in company’s history, with adjusted earnings rising 5.2% to $2.64 per share. E-commerce sales grew nearly 25% for fiscal 2026, surpassing $150 billion for the first time.

Walmart’s rapidly growing higher-margin businesses is another reason for the optimism surrounding the stock. Global advertising revenue jumped 37% in Q4, with membership income went up more than 15% globally. Notably, Walmart said that advertising revenue and membership fees combined made up nearly one-third of its fourth-quarter operating income.

Analysts expect Walmart to report earnings of $0.66 per share, compared to $0.61 in the year-ago quarter. Revenue is expected to increase by 5.5% $174.8 billion. For the full year, management expects sales growth of 3.5% to 4.5%, with earnings per share landing between $2.75 and $2.85. Meanwhile, analysts anticipate revenue and earnings to increase by 6% and 10.6%, respectively.

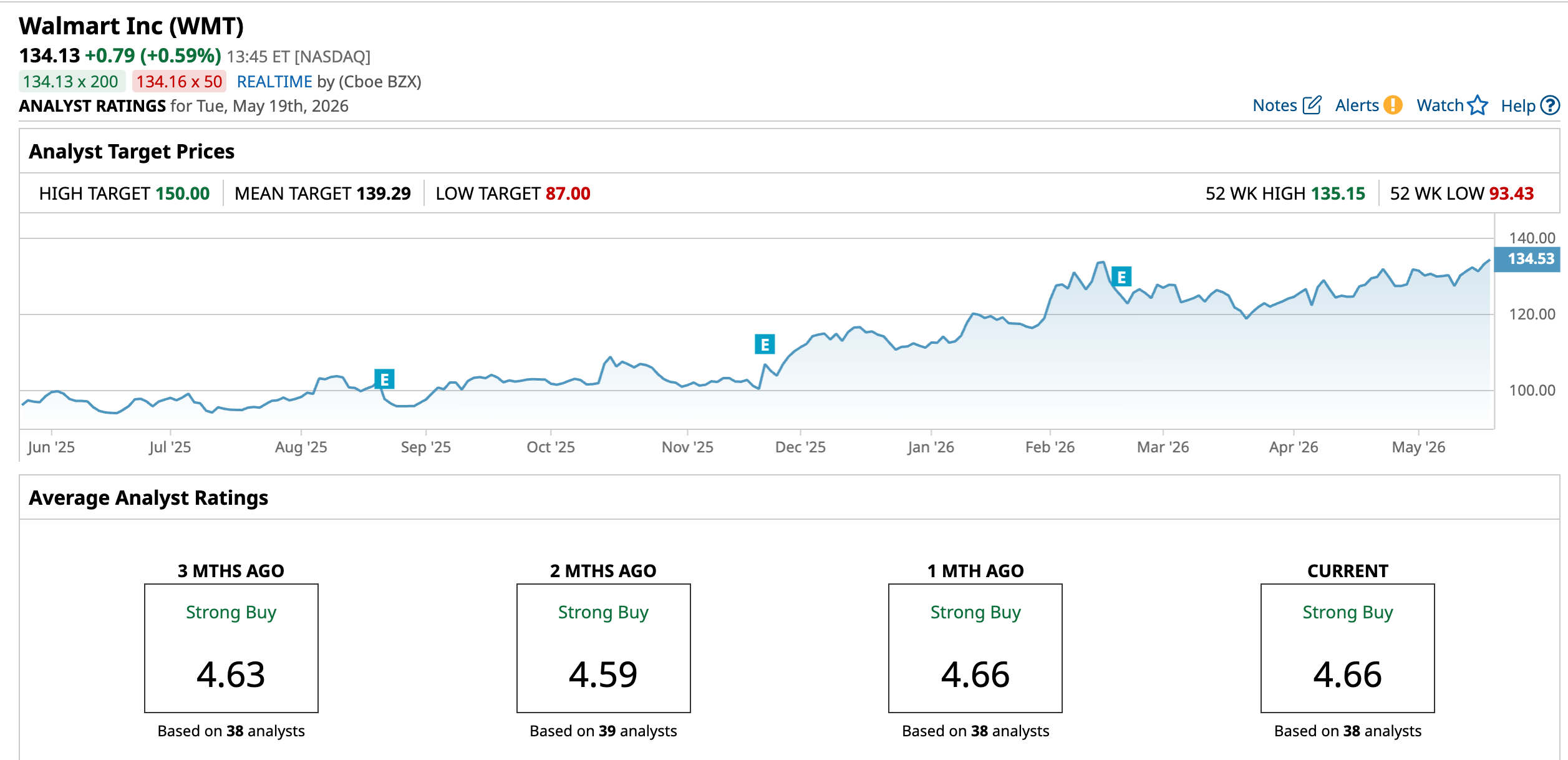

Expecting another strong quarter, Piper Sandler analyst Peter Keith raised the price target to $137 from $130, and maintained his “Overweight” rating. Keith stated that consumer spending has remained resilient despite concerns over higher gas prices hurting discretionary demand. Similarly, Bernstein analyst Zhihan Ma raised the price target on Walmart to $145 from $134, with an “Outperform” rating. The analyst expects the “One Big Beautiful Bill Act” stimulus to support sales momentum among higher-income consumers, but also warned of fuel costs and inflation weighing on earnings quality for some retailers.

Meanwhile, Wolfe Research held on to the “Outperform” rating, while raising the price target to $137 from $135. Wolfe expects Walmart to deliver strong first-quarter results despite potential pharmacy-related headwinds. Furthermore, Evercore ISI, BMO Capital, TD Cowen, BTIG, among others also raised the target price for Walmart ahead of earnings.

Why Wall Street Remains Bullish on Walmart Despite a Weak Economic Scenario

Overall, the reason behind analysts seeming bullish is that they see Walmart as one of the safest and strongest large-cap retailer in an uncertain consumer environment. Even with concerns around inflation, fuel prices, and weaker discretionary demand, Walmart has stayed resilient and appears to be gaining traffic and market share. Furthermore, Walmart’s scale, grocery dominance, pricing power, and ability to attract high-value consumers during tougher economic cycles makes it stronger than its competitors. This probably explains Wolfe Research calling it an “all-weather compounder.”

Investors are increasing considering Walmart as a combination of a defensive consumer staple, a technology-enabled platform, and a long-term market-share winner. These factors explains why Walmart is trading at a premium of 45.44 times forward fiscal 2027 earnings.

Another reason could be that Walmart’s higher-margin businesses, including e-commerce, advertising, memberships, and marketplace operations, which are boosting its long-term earnings profile beyond traditional retail. Plus, its AI and automation investments could improve margins over time. Walmart’s resilience is one reason why it has successfully maintained its status as a Dividend King, by paying and increasing dividends for the past 52 years.

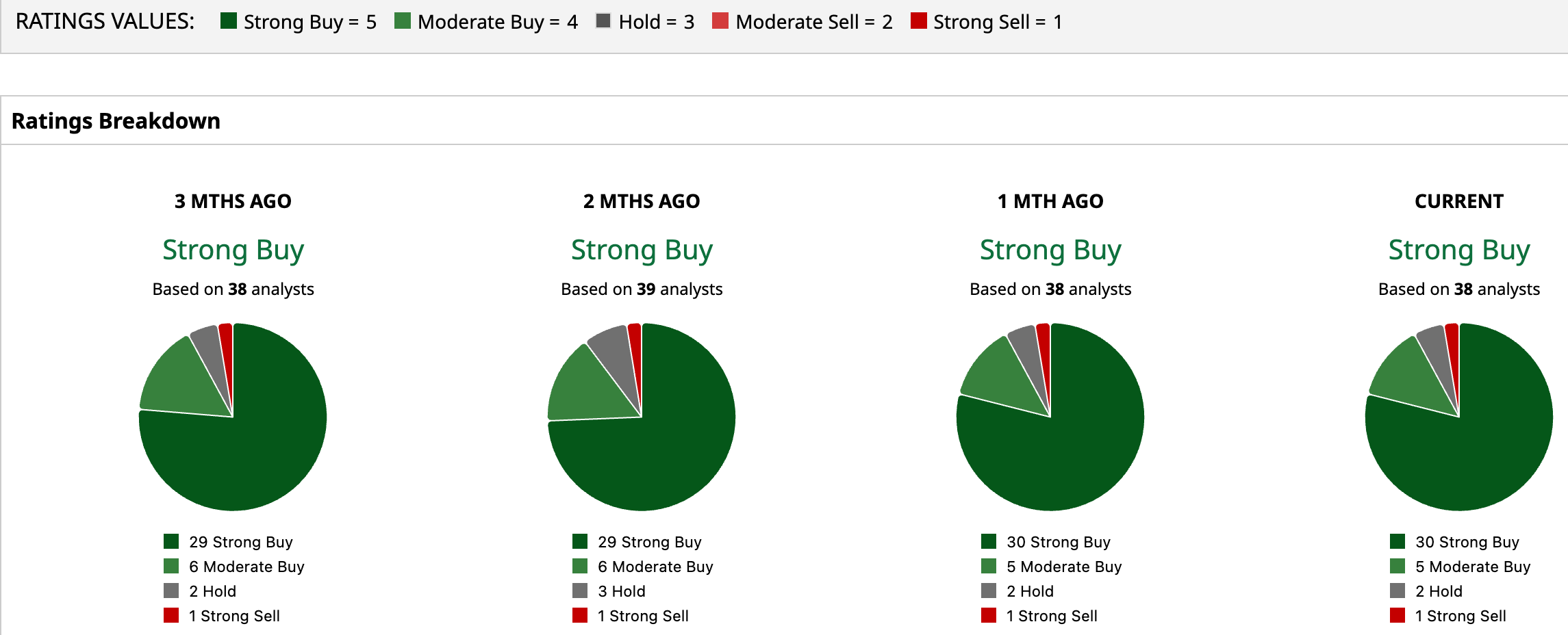

Hence, Walmart stock holds a consensus “Strong Buy” rating on the Street. Of the 38 analysts covering the stock, 30 rate it a “Strong Buy,” five say it is a “Moderate Buy,” two rate it a “Hold,” and one says it is a “Strong Sell.” Analysts at Bank of America, TD Cowen, D.A. Davidson, and a few others have assigned a high price estimate of $150 for WMT stock, which implies an upside potential of 11.8% from current levels.

I believe these price upgrades are not just about one quarter. Analysts view Walmart as a stronger, long-term growth stock rather than just a defensive retailer. Overall, it appears that Walmart could emerge as a long-term winner, even if the broader retail environment weakens.

On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Microsoft%20headquarters%20By%20Peter.jpeg)

/Apple%20products%20on%20desk%20by%20Ake%20Ngiamsanguan%20via%20iStock.jpg)

/Nvidia%20logo%20by%20Konstantin%20Savusia%20via%20Shutterstock.jpg)