/AI%20(artificial%20intelligence)/Data%20Center%20by%20Caureem%20via%20Shutterstock%20(2).jpg)

I previously covered how Marvell Technology's (MRVL) stock was surging on a hidden growth engine: optical connectivity. There’s another company that offers exposure to the same AI infrastructure bottleneck, but in a different way. Corning Inc. (GLW) is a diversified materials science business that makes the raw materials and equipment for optical networking.

This is just one part of the company’s business, though this might be a turn-off for those looking for optical pure-plays. For others, a stable business outside this segment enables the company to take increased risks on the back of its existing business. This reduces the volatility associated with pure-plays involved in emerging technologies, making Corning an attractive investment.

The company recorded fresh all-time highs last week, and most of the optimism is due to a deal with the Godfather of AI, Jensen Huang. Huang’s Nvidia (NVDA) will help Corning expand its optical connectivity production tenfold, increasing local fiber capacity by more than 50%. While Nvidia will gain strategic supply access, Corning will be able to expand its manufacturing footprint through three new facilities based in Texas and North Carolina.

The company’s bull thesis is pretty straightforward: Every new GPU cluster requires exponentially more optical interconnect infrastructure, and Corning is about to provide that, in partnership with the largest GPU maker in the world.

About Corning Incorporated Stock

Corning Incorporated provides fiber optics, glass, and specialty material products used across various industries globally. The company manufactures products such as optical fiber and cable solutions, display glass, laboratory equipment, and specialty glass & ceramic products. It also offers components and materials used in the healthcare, telecommunications, aerospace, consumer electronics, and automotive industries. Founded in 1851, Corning is headquartered in Corning, New York.

The stock delivered exceptionally strong performance over the past year, clearly outperforming the S&P 500 (SPY). While the broader index gained about 24% during the same period, the stock surged approximately 298% over the last year.

Corning’s forward P/E of 65x is high compared to its own historic valuation. In fact, the stock is expensive on various valuation metrics, but that’s fully justified considering the earnings growth. An average growth rate of 30% through the next four years for a company that just received Nvidia’s backing is a fair valuation.

Corning Posts Strong Earnings

The company posted its first-quarter FY26 results on April 28. Sales increased 18% year-over-year to $4.35 billion, while earnings rose 30% to $0.70 per share. The optical communications segment sales grew 36% year-over-year to $1.85 billion. Net income from the segment came in at $387 million, surging 93% year-over-year. Solar segment reported sales of $370 million, up 80% year-over-year, however, net income declined by $20 million year-over-year to $7 million.

Going forward, second-quarter sales are expected to grow about 14% year-over-year to around $4.6 billion. Earnings are projected to come in between $0.73 and $0.77, rising 25% year-over-year. For the full year, the company anticipates generating much higher free cash flow than in the previous year.

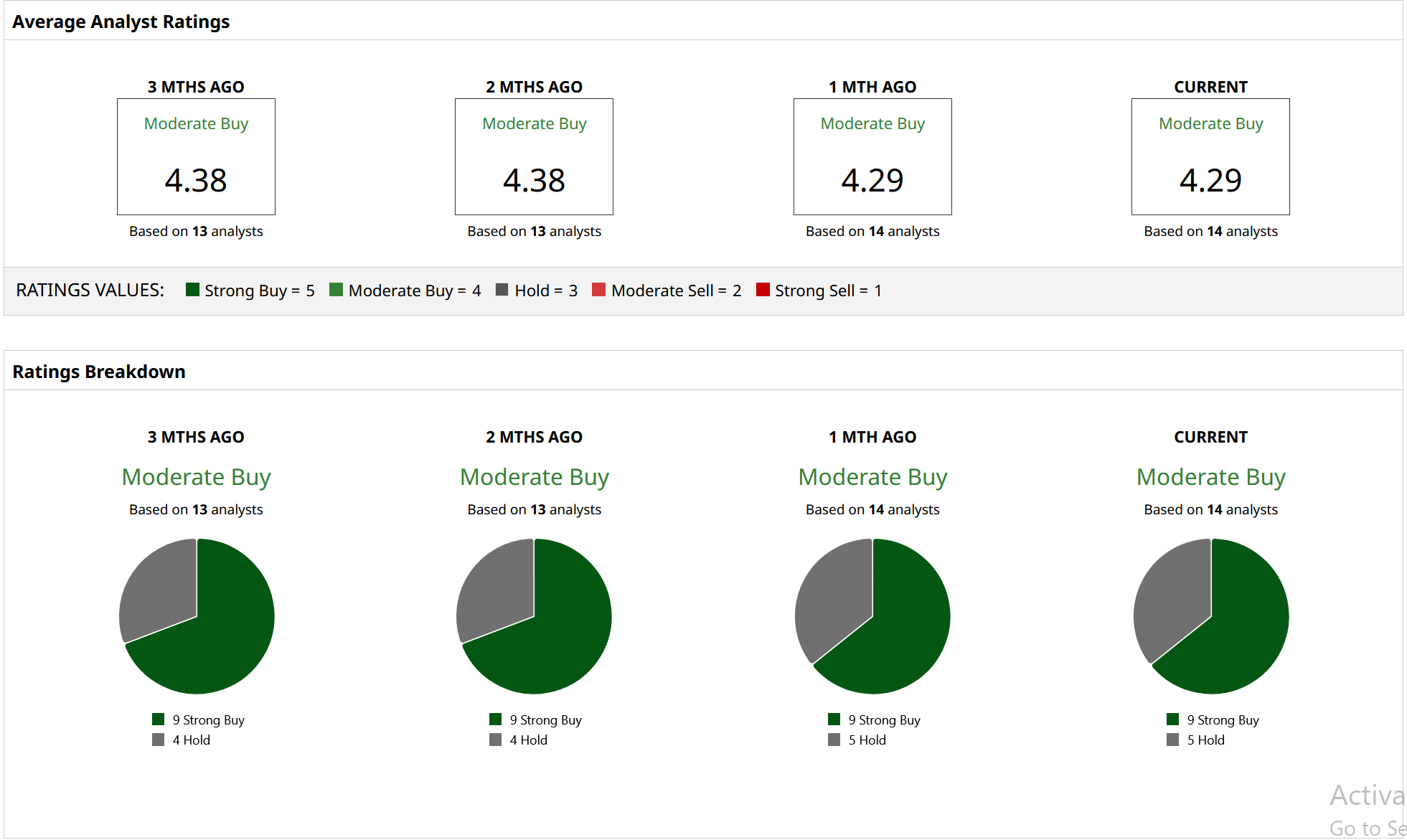

What Are Analysts Saying About Corning Stock

Analyst sentiment has recently turned positive toward the stock, with most of them raising their price targets. According to the latest update on May 11, Mizuho Securities analyst John Roberts increased the firm’s price target on the stock from $190 to $220 while keeping a “Buy” rating. Earlier, on May 8, Morgan Stanley also adjusted its price target upward to $180 from $140 and maintained a “Hold” rating on the shares.

Corning currently holds a consensus “Moderate Buy” rating from 14 Wall Street analysts covering it. According to their estimates, the stock has a mean price target of $200.92, an upside of 12.5% while the highest price target of $230 offers 29% upside from the current levels.

On the date of publication, Jabran Kundi did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Microsoft%20headquarters%20By%20Peter.jpeg)

/NVIDIA%20Corp%20logo%20outside%20building-by%20BING-JHEN_HONG%20via%20iStock.jpg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Amazon%20-%20Image%20by%20bluestork%20via%20Shutterstock.jpg)