Despite an increasing investor interest in AI power infrastructure, Oklo (OKLO) stock has been experiencing a downtrend that doesn’t seem to stop. One reason for this is the heavy discount to future cash flows that the market seems to be giving energy stocks like Oklo. As high as the demand is for power, the fact remains that Oklo will be unable to deliver a single watt of power before 2027.

Once the initial hype subsided, the market started rewarding players who had already started shipping products to the market. Take Bloom Energy (BE), for instance. The stock is up nearly 1,300% in a year, having doubled in the last month alone. The reasoning is simple: Market participants are rewarding companies that are solving the AI power problem today, rather than attempting to do it in the future.

This rotation and disconnect are understandable. Oklo’s inability to generate revenue today is costing its shareholders, but the long-term bull case is only strengthening. Oklo is a small modular reactor (SMR) company. SMRs are a new class of nuclear reactors that are smaller and easier to deploy than traditional nuclear power plants. Depending on demand, multiple smaller power plants can be deployed to mirror large conventional nuclear reactors, which can otherwise take a decade or more to build. Currently, no SMRs operate in the U.S. This unique positioning gives Oklo a huge advantage, which is further strengthened by two structural tailwinds.

Oklo’s Advantage No. 1: Securing Long-Term Margins Through Owner-Operator Model

Companies fulfilling the AI power demand today are able to do so comfortably because hyperscalers are paying a premium to get this power and avoid owning the power plant in the short term. By doing so, they are also keeping a chunk of the operating margin. Oklo, by taking a long-term approach and pursuing an own-and-operate model to sell electricity to customers, is playing a different game. Through ownership of the plants, it can keep most of the operating margin on its balance sheet. This model cannot easily be replicated as existing customers, the hyperscalers, would object to these companies shifting away from the short-term solutions they’re providing.

Oklo’s Advantage No. 2: Forcing Competitors to Play Catch-Up

Oklo’s second major advantage is its licensing strategy. The company’s Aurora-INL, A3F fuel fabrication facility, and the Groves reactor are all pursuing authorization through the U.S. Department of Energy’s (DOE) Reactor Pilot Program as opposed to the standard NRC commercial licensing pathway. The DOE pathway potentially removes three years of regulatory hurdles from the development timeline faced by peers! Once Oklo starts selling electricity, it will carry this inherent advantage for a long time.

About Oklo Stock

Oklo is a U.S.-based company that develops advanced fission power plants to produce reliable, clean, and affordable energy. Its primary product, Aurora Powerhouse, can generate between 15 and 75 megawatts of electricity. The company also works on recycling used nuclear fuel into usable fuel for its reactors and produces radioisotopes.

After a stellar performance in 2025, the company’s stock is down 20% this year. In contrast, the Defiance AI and Power Infrastructure ETF (AIPO) is up over 39% YTD. This difference can easily be explained by the dominance of companies that are serving the power demand today. Oklo investors need not worry about this underperformance, as the company’s objectives are totally different and long-term oriented.

Oklo Reports Another Quarterly Loss

Oklo reported its Q1 2026 earnings on May 12, reporting a loss of $33.1 million. This is similar to the losses reported on prior earnings reports. Oklo had previously reported its fourth-quarter fiscal 2025 earnings on March 17, posting a full-year operating loss of $139.3 million.

The main reason behind the losses is higher payroll and business expenses. Therefore, the loss hardly matters in the grand scheme of things. The company ended 2025 with $1.4 billion in cash and marketable securities. This position was further strengthened by a $1.18 billion capital raise in January 2026.

On May 13, the company’s filing showed it was raising another $1 billion, primarily to fulfill the company’s 1.2 gigawatt agreement with Meta Platforms (META) and a partnership with Nvidia (NVDA).

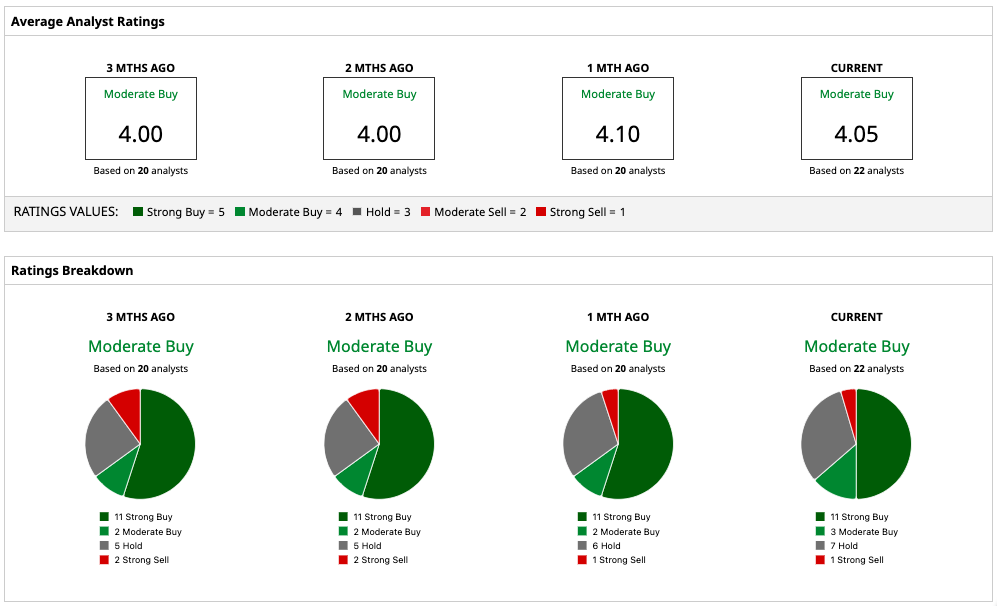

What Are Analysts Saying About Oklo Stock

At least two analysts are expecting a 100% return from Oklo stock over the next 12 months. These include Canaccord Genuity’s George Gianarikas, who has a $125 price target on the stock, and Cantor Fitzgerald’s Derek Soderberg, who has a $122 price target. Both these updates came post-earnings, once again showing that the quarterly loss is nothing to worry about.

The stock carries a consensus “Moderate Buy” rating from 22 Wall Street analysts covering it. Based on their estimates, it has a mean price target of $88.90, reflecting 52% upside from the current levels.

On the date of publication, Jabran Kundi did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/NVIDIA%20Corp%20video%20chip-by%20Antonio%20Bordunovi%20via%20iStock.jpg)

/Space/Rocket%20lift%20off%20by%20Alones%20via%20Shutterstock.jpg)

/A%20close-up%20of%20an%20AMD%20office%20by%20gehapromo%20via%20Adobe%20Stock.jpeg)