The artificial intelligence (AI) boom is triggering a massive power scramble, and suddenly, nuclear energy is in fashion. As tech giants hunt for reliable electricity to run data centers and AI systems, Oklo (OKLO) has emerged as one of the market’s most talked-about nuclear startups.

The California-based company is developing compact fast reactors designed for quicker deployment and scalable clean-energy production. That vision has quickly turned Oklo into one of Wall Street’s favorite next-generation energy stories. But this week also proved that the stock remains a high-risk, high-reward bet.

OKLO slid sharply after its first-quarter report, tumbling 22% over the following four trading sessions as investors reacted to widening losses, rising cash burn, and one harsh reality. The company still is not generating revenue. For a pre-commercial nuclear startup, patience is part of the deal. Yet in today’s market, investors increasingly demand proof instead of promises, so the pressure to execute is rising fast. That is exactly the reason that July 4 suddenly matters so much.

The date is more than symbolic patriotism. The United States Department of Energy wants advanced nuclear reactors to achieve criticality by then, essentially proving they can sustain a controlled nuclear chain reaction safely and reliably. Oklo is aiming to hit that milestone through projects tied to its Aurora reactor and the Groves isotope reactor in Texas. If successful, it would mark one of the most important technical validations in the company’s history.

Even after the selloff, William Blair still sees Oklo as a serious long-term player in advanced nuclear energy. And for investors, July 4 could be more than a holiday. It may become the moment investors decide whether this nuclear moonshot is finally becoming real.

About Oklo Stock

Founded in 2013 and based in Santa Clara, Oklo is developing advanced fast-fission reactors aimed at delivering reliable, carbon-free energy for modern industrial needs. Established by MIT graduates Jacob DeWitte and Caroline Cochran, the company focuses on compact nuclear systems designed for scalable deployment across AI data centers, defense infrastructure, and industrial operations.

Valued at $10.83 billion by market cap, Oklo has secured key milestones within the U.S. nuclear sector, including a Department of Energy site-use permit, fuel awards from Idaho National Laboratory, and a landmark advanced reactor license application with the Nuclear Regulatory Commission.

Since going public through a SPAC merger in 2024, OKLO has delivered one of the wildest rides in the market. Shares have surged 488.93% since debuting and are still up more than 53.2% over the past year. This is seen as an extraordinary run for a company that has yet to generate meaningful revenue.

As investors searched for companies capable of powering the AI boom, Oklo quickly became a favorite bet. This is probably because if AI data centers are going to consume massive amounts of electricity, the world will need stable, carbon-free power sources, and small modular reactors could become part of that solution. That excitement reached a fever pitch last October, when the stock soared to a high of $193.84 amid intense enthusiasm around next-gen nuclear infrastructure.

But in 2026, investors started looking beyond the excitement and focusing more on the business itself. Oklo is pre-revenue, and the company continues spending heavily on reactor development, fuel expansion projects, and long-term growth plans. Its latest quarterly report made investors even more cautious after losses came in higher than expected, raising fresh concerns about the amount of money and time it may take before Oklo finally becomes commercial.

As sentiment shifted, the stock pulled back sharply, down 70% from its all-time high and has fallen 19.47% year-to-date (YTD), showing how quickly momentum can reverse for high-growth companies built largely on future expectations.

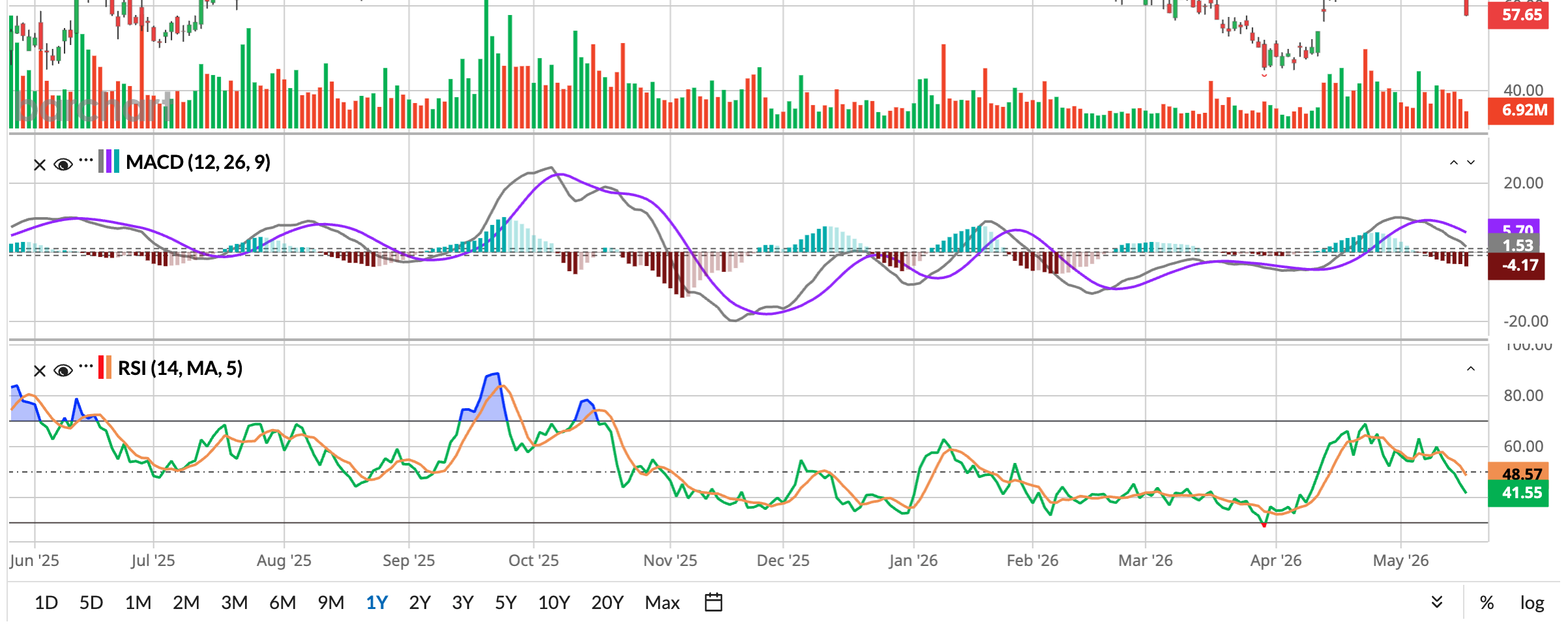

Technically, the chart signals investors are turning more cautious in the near term. Trading volume has been flashing more red days lately, a sign that sellers still have the upper hand. The 14-day RSI has cooled to 41.65, which basically says the stock has lost its earlier momentum but is not deeply oversold yet.

The MACD oscillator is also signaling weakening momentum in OKLO. A few days ago, the MACD line slipped below the signal line, typically viewed as a bearish technical crossover that suggests selling pressure is building. But now, the line is slightly above the signal line. At the same time, the histogram has moved deeper into negative territory, indicating that bullish momentum has continued fading in recent weeks.

Oklo’s Widening Q1 Losses

Oklo released its fiscal 2026 first-quarter results on May 12, and shares of the advanced nuclear startup slid 5.76% as investors reacted to widening losses, heavy spending, and the reality that the company is still years away from generating meaningful revenue. Oklo remains firmly in development mode, pouring cash into reactor engineering, fuel systems, infrastructure, licensing, and long-term deployment plans as it races to commercialize its Aurora nuclear platform.

For the quarter, Oklo posted a net loss of $33.1 million, or -$0.19 per share, sharply higher than the $9.8 million loss or -$0.07 per share reported a year earlier. Much of the increase came from a rapid rise in operating expenses, which climbed to $51.2 million from $17.9 million last year as the company expanded hiring across technical and administrative teams and ramped up stock-based compensation.

Research and development spending alone surged to $27 million in Q1, reflecting aggressive investment in reactor design, fuel development, and commercialization technology. General and administrative expenses also jumped to $24.2 million as Oklo continued building the organizational backbone needed to support a future large-scale nuclear business.

Still, beneath the headline losses, Oklo showed investors that it now has an enormous financial runway. The company ended the quarter with roughly $2.5 billion in cash and marketable securities, largely fueled by a successful at-the-market equity offering program that generated approximately $1.2 billion in net proceeds. Management says the capital will help fund expansion across its power, fuel, and isotope businesses as the company pushes toward commercialization.

And operationally, the company continues stacking up milestones. At Idaho National Laboratory, Oklo cleared an important regulatory hurdle after the U.S. Nuclear Regulatory Commission approved the Principal Design Criteria for its Aurora powerhouse project – a key framework that supports future licensing approvals. Further, the company confirmed excavation work is already underway for the deep foundations tied to its first commercial reactor unit.

Meanwhile, Oklo says its newly acquired Atomic Alchemy subsidiary remains on track to pursue criticality for the Grove reactor by July 4 while also engaging with its first potential isotope customer ahead of expected commercial isotope revenue next year.

The company is leaning heavily into partnerships tied to the AI boom. Management highlighted collaborations with NVIDIA Corporation and Los Alamos National Laboratory focused on advanced reactor engineering and plutonium-based fuel development. In Ohio, Oklo is continuing work on its planned 1.2-gigawatt power campus through its partnership with Meta Platforms, including submitting PJM interconnection applications needed to eventually connect future reactors to the regional grid and support rapidly expanding AI-driven data center demand.

Analysts monitoring Oklo predict the company’s losses to widen by 7% year-over-year YOY to -$0.77 per share in 2026, and then expand by 24.7% annually to -$0.96 per share in fiscal 2027.

What Do Analysts Expect for Oklo Stock?

Despite the market’s recent nerves, not everyone on Wall Street is backing away from OKLO, with some analysts still believing OKLO remains one of the more promising names in the advanced nuclear space. Like William Blair analyst Jed Dorsheimer, recently reiterated his “Outperform” rating after the report, pointing to the company’s steady progress across its power, fuel, and isotope businesses.

He acknowledged that Oklo is still a pre-revenue company carrying meaningful risk, but argued that the broader environment is starting to work in its favor as nuclear energy gains stronger political and regulatory support in the U.S.

Even so, he made clear this is far from a risk-free bet. The analyst noted that some challenges, like regulatory shifts at the Nuclear Regulatory Commission, growing competition from other reactor technologies, funding pressures, and execution challenges, could influence how quickly Oklo turns its nuclear ambitions into commercial business.

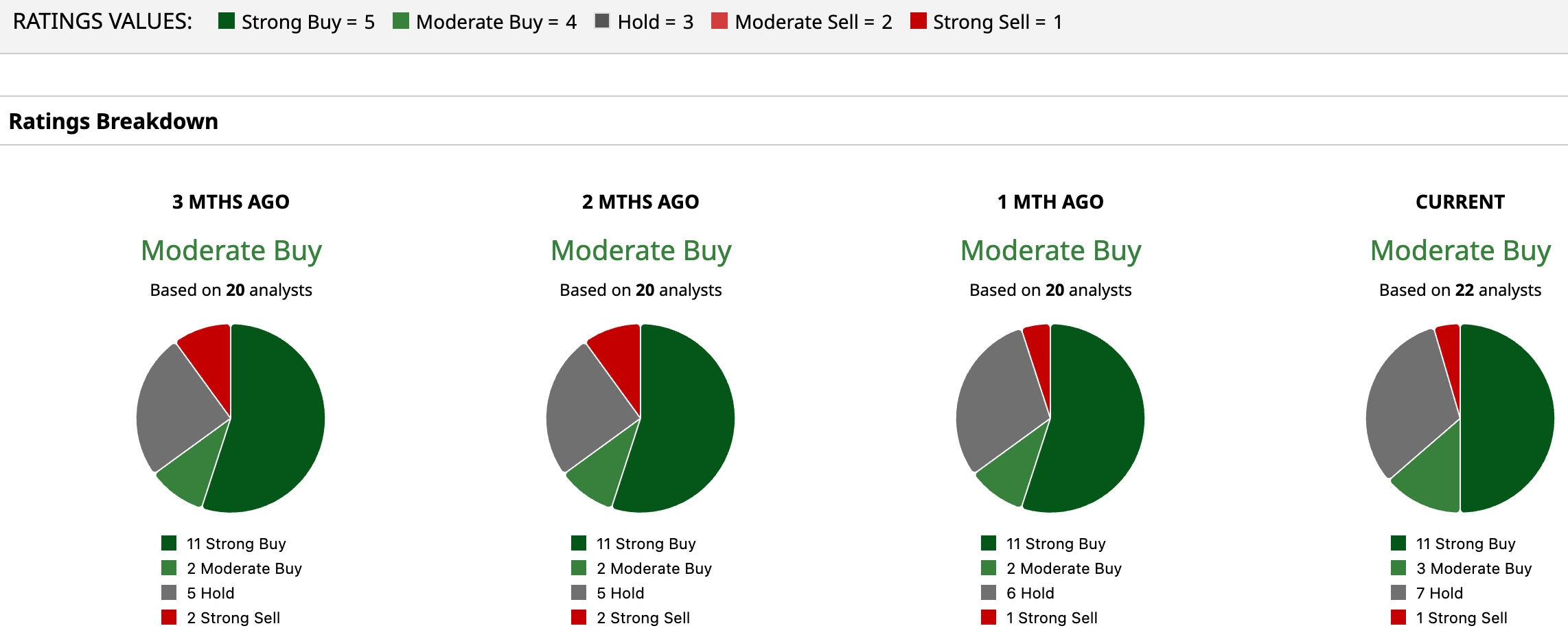

Wall Street analysts continue to view Oklo as one of the more intriguing long-term plays in the growing race for advanced nuclear power and AI-driven energy infrastructure, despite all the panic surrounding OKLO lately. The stock has a consensus “Moderate Buy” rating, reflecting continued optimism that Oklo could emerge as a major player in the next-gen clean-energy infrastructure. Among the 22 analysts covering the stock, half of them suggest a “Strong Buy,” three recommend a “Moderate Buy,” while seven remain on the sidelines with “Hold” ratings. Just one analyst is still firmly in the bear camp, sticking with a “Strong Sell” rating.

The average price target of $88.90 implies potential gains of 53.8% from current levels, while the Street-high target of $130 suggests shares could soar as much as 124.5% from here.

Conclusion

Criticality may sound like a technical nuclear term, but for OKLO, it could become the moment that changes everything. If Oklo successfully proves its reactor can sustain a controlled chain reaction by the July 4 target, investors would finally get real-world proof that the company’s fast-reactor technology actually works.

And right now, proof is exactly what Wall Street wants.

Oklo is a pre-revenue company, which means investors are betting on future potential, not current profits. That is why the stock stumbled after its latest earnings report, as rising losses, growing cash burn, and a new $1 billion equity offering raised fresh dilution concerns.

Naturally, investors started wondering why the company even needs more capital when it already holds roughly $2.5 billion in cash and marketable securities and expects relatively modest 2026 cash burn. The additional funding could be meant for future investments, reactor development, and broader corporate needs. But it also reflects a simple reality of the nuclear industry – building reactors takes enormous amounts of money long before revenue starts showing up. Meanwhile, the fundraising could signal that management is preparing aggressively for its next major phase of development rather than simply plugging financial holes.

With its first planned powerhouse deployment still years away, execution now matters more than hype. If the company keeps hitting milestones, maintains progress toward criticality, and strengthens partnerships with tech giants, investor sentiment could turn around quickly.

On the date of publication, Sristi Suman Jayaswal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Netflix%20open%20on%20tablet%20by%20rswebsols%20via%20Pixabay.jpg)