Based in Amsterdam and spun out from Yandex’s international business, Nebius Group (NBIS) has steadily reshaped itself into a full‑stack “neocloud” operator. The firm just posted a standout Q1 2026, with revenue hitting $399 million, up 684% from a year earlier, while its AI Cloud business jumped 841% to $390 million and sent the stock up 15.72% in one day.

That kind of growth is being backed by big, concrete wins. Nebius has a near $27 billion multi‑year AI infrastructure deal with Meta Platforms (META), a 1.2 GW power agreement tied to a possible $20 billion push into the U.S., and approvals in hand for its first gigawatt‑scale AI factory.

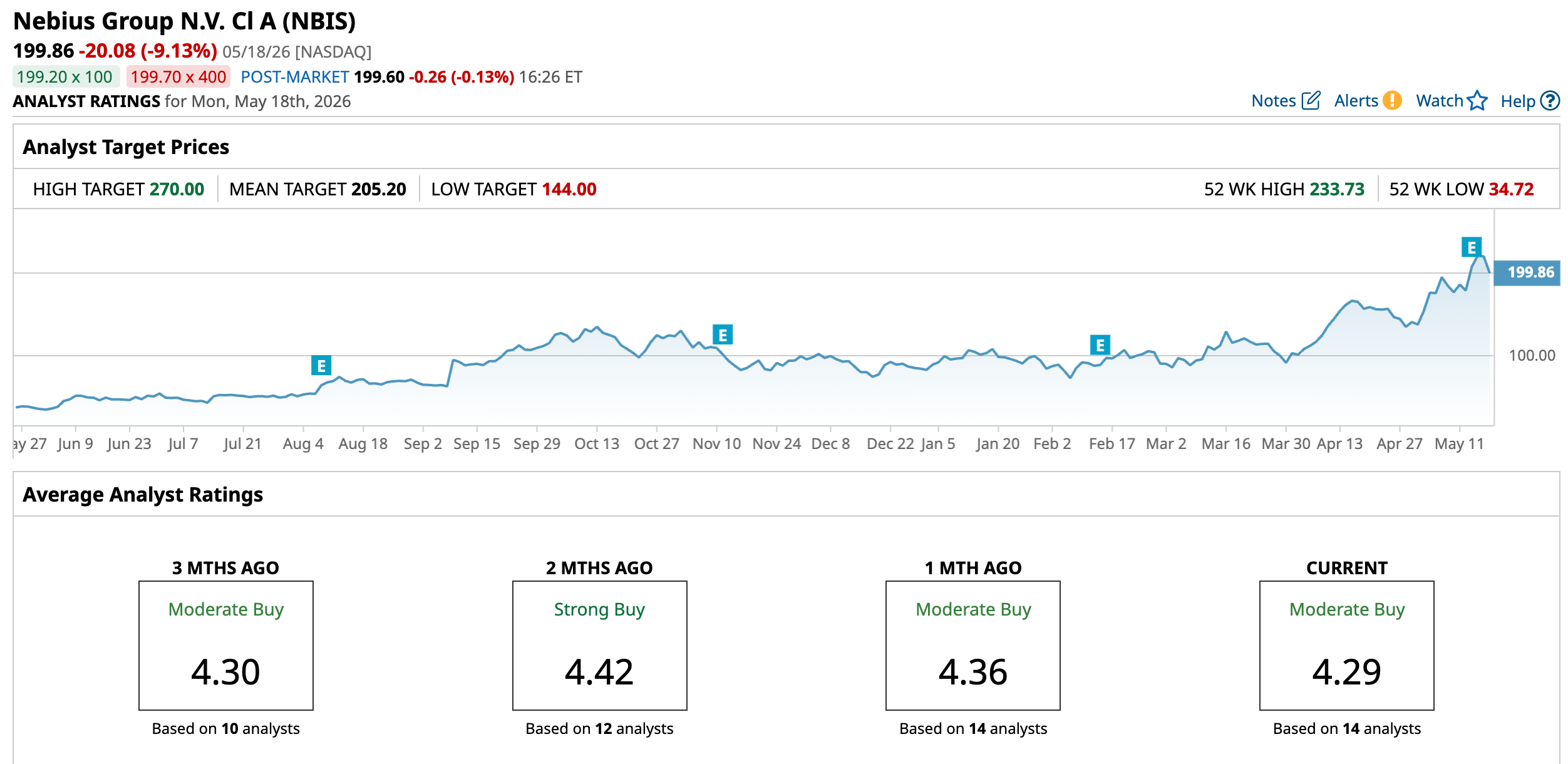

Only a few days after those headlines and the earnings beat, Citi took its call up a notch, lifting its price target on NBIS to a Street‑high $287 from $169 and sticking with a Buy rating.

So, what is Citi seeing in Nebius that makes a $287 target make sense, and are other analysts starting to move in the same direction?

Nebius Numbers Behind The Bull Case

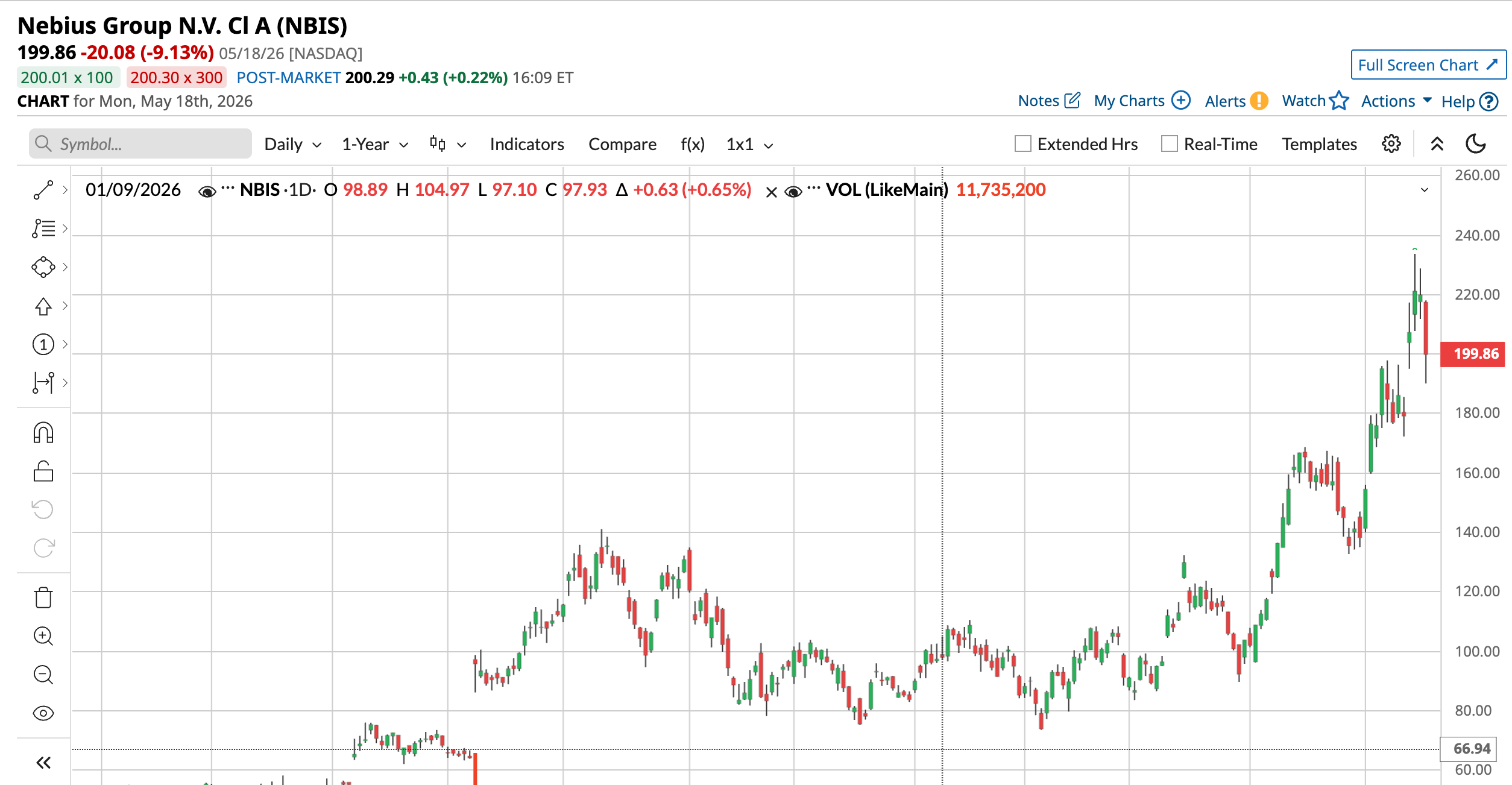

Nebius is a Netherlands-based company that runs cloud infrastructure built around high-density GPU data centers and large-scale computing for enterprise and hyperscale customers. Its stock up 138.17% year-to-date (YTD) and 434.2% over the past 52 weeks. The company is now valued at about $55.65 billion.

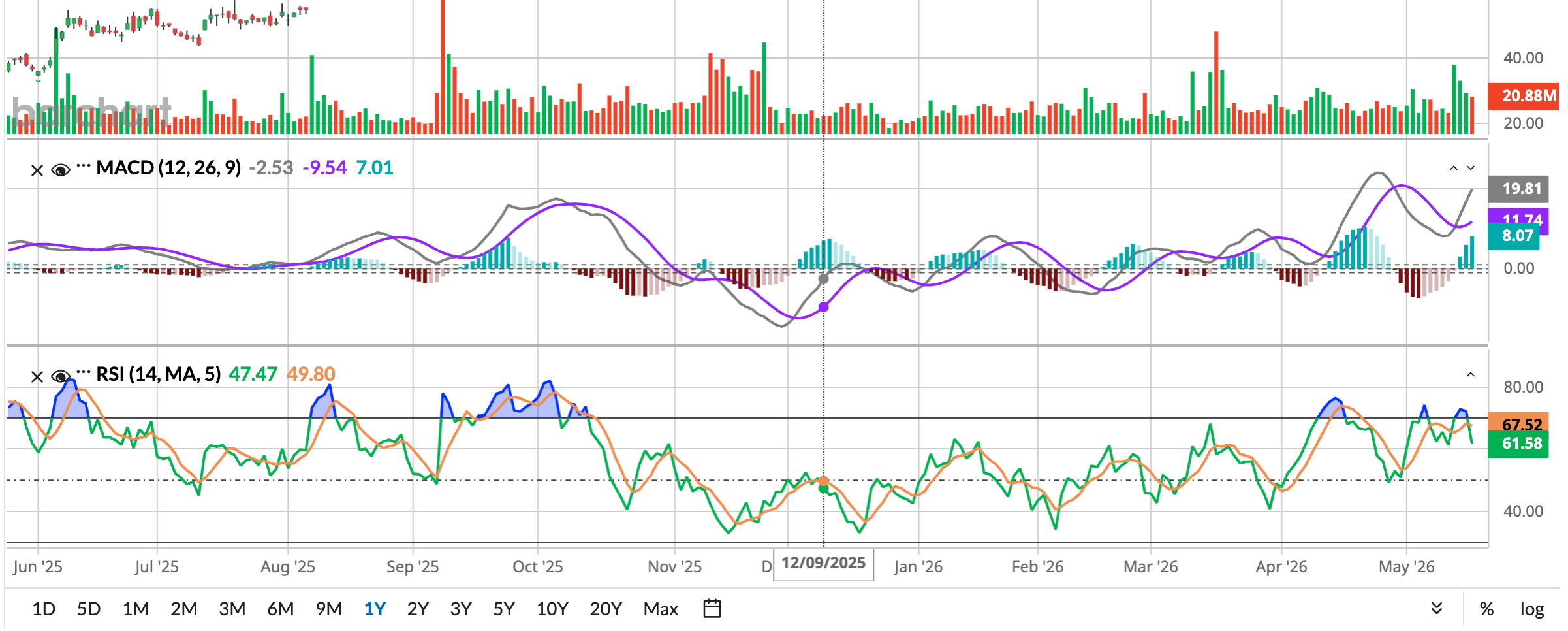

NBIS trades at 16.36 times sales versus a sector median of 3.33 times and 9.16 times book value versus a 4.45 times sector median, showing high growth expectations.

Nebius’ first quarter of 2026 was strong by any measure. The company’s revenue climbed to $399.0 million from $50.9 million a year earlier, a 684% jump as demand ramped quickly. Their March 31 earnings release also came in well ahead of expectations. Nebius reported EPS of -$0.23, far better than the consensus estimate of -$0.81, for a 71.60% upside surprise.

The profitability picture improved sharply on the surface. Its adjusted EBITDA swung from a loss of $53.7 million to a profit of $129.5 million, while net income from continuing operations moved from a $104.3 million loss to a $621.2 million profit.

There was still some pressure underneath those headline numbers. Adjusted net loss widened to $100.3 million from $83.6 million, showing the business is still spending heavily as it expands. And, Nebius is leaning harder into that investment cycle. The company lifted its 2026 capex outlook to $20 billion to $25 billion from $16 billion to $20 billion, with part of that budget going toward 2027 capacity expected to start adding revenue in the first half of next year.

Why Citi Thinks Nebius’ AI Build‑Out Justifies its Target

Nebius is widening its inference toolkit with a planned acquisition of Eigen AI. That deal is meant to strengthen its Token Factory platform and give the company more depth in handling complex inference workloads. Further, the company is building out the hard infrastructure behind that strategy. Nebius has started work on a gigawatt-scale AI factory in Independence, Missouri.

Another important move is the addition of Clarifai’s core team and licensed inference IP. That combination should make Token Factory stronger and help Nebius roll out and manage models more efficiently in real-world use.

Product work is moving alongside these infrastructure and talent bets. Nebius AI Cloud 3.5 introduced serverless AI, aimed at giving developers easy, on-demand compute for practical AI applications without having to manage as much underlying hardware.

Security is getting similar attention as more enterprises test and deploy AI. Nebius has partnered with CrowdStrike (CRWD) to bring unified security across its next-generation cloud setup. That will make the platform more attractive to larger, security-sensitive customers.

NBIS is also tightening its relationship with Nvidia (NVDA) beyond a simple supplier role. The two companies are working together on cloud infrastructure for robotics and physical AI, and Nvidia has separately invested $2 billion into Nebius, backing its long-term buildout plans with real capital.

The platform is gaining more intelligence at the application layer as well. Nebius has agreed to acquire Tavily, which would add agentic search to its cloud offering and give customers better tools for building autonomous systems that need to pull in fresh information.

Taken together, these moves help explain why analysts remain upbeat on NBIS even after the stock’s big run.

Wall Street Is Lining Up Behind NBIS

Nebius’ next big checkpoint is on August 6, 2026, when NBIS is due to report earnings again. For the current quarter ending June 2026, analysts expect EPS of ‑$0.69, compared with ‑$0.38 a year earlier, which points to an estimated year‑over‑year (YOY) decline of 81.58%.

That weaker near-term earnings view has not stopped major banks from leaning into the longer story. Bank of America started coverage with a “Buy” rating, giving Nebius a vote of confidence from a large institution. The firm highlighted a huge addressable market and estimated that AI infrastructure spending could reach about $419 billion by 2028.

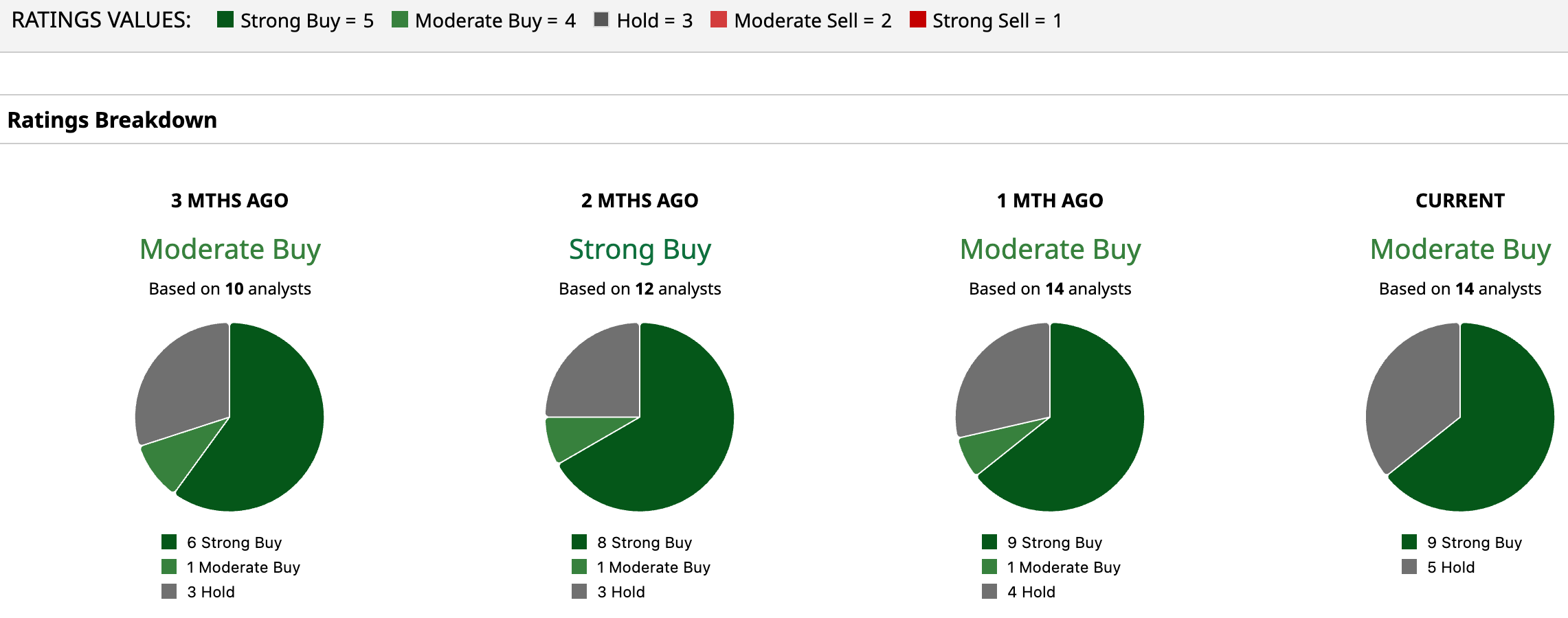

That lines up with the way in which the broader analyst community is examining the stock. Across 14 analysts, the consensus rating sits at “Moderate Buy” rather than an all-in bullish call. The average price target is $205.20, implying a marginal upside of 2.67% from current levels.

Conclusion

Citi’s $287 target shows Nebius is now seen as a core conviction growth story, not just a side trade in the AI theme. The odds still tilt toward more upside over time, as long as management keeps delivering on new capacity and locking in long term deals. Pullbacks are almost guaranteed after a run like this, but the bigger trend still points more toward higher levels than a full reset. In simple terms, this is a name the market is likely to keep re‑pricing as the story develops.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/An%20image%20of%20the%20Snowflake%20logo%20on%20a%20corporate%20office_%20Image%20by%20Grand%20Warszawski%20via%20Shutterstock_.jpg)

/Netflix%20on%20tv%20with%20remote%20by%20freestocks%20via%20Unsplash.jpg)