/AI%20(artificial%20intelligence)/AI%20Infrastructure%20by%20FOTOGRIN%20via%20Shutterstock.jpg)

Nebius Group (NBIS) has quickly emerged as one of the most intriguing and controversial players in the rapidly expanding AI infrastructure landscape. The company recently captured market attention after securing a massive deal with Meta Platforms (META) worth up to $27 billion, a contract that could dramatically reshape its growth trajectory and position it more firmly among the leading “neocloud” providers. For a company that, until recently, primarily served smaller AI startups, this agreement marks a significant step into hyperscaler territory.

At first glance, the investment case may seem straightforward: Nebius is riding the same powerful wave that has propelled the entire AI ecosystem. However, beneath the surface, the story is far more complex. The company is simultaneously ramping capital expenditures, issuing convertible debt, and operating in a highly competitive and capital-intensive industry where execution risk is high.

So what are investors really buying when they purchase NBIS stock? Is this a pure-play opportunity to gain exposure to the AI infrastructure boom before it fully matures or a high-risk bet on a capital-intensive business still proving its long-term economics? Let’s take a closer look!

About Nebius Group N.V. Stock

Nebius Group N.V. is a Netherlands-based technology company. The company was spun out of the international operations of Russian technology group Yandex in 2024. NBIS is focused on building a comprehensive AI infrastructure to serve the global AI industry, with major operations across Europe, North America, and Israel. It is one of several so-called “neoclouds,” smaller cloud computing providers that supply infrastructure capacity for AI workloads. Beyond its core AI infrastructure business, Nebius also owns subsidiaries including Avride, Toloka, and TripleTen, which specialize in autonomous driving technology, AI data services, and educational technology, respectively. It has a market cap of $29.4 billion.

Shares of the neocloud company have rallied 43% on a year-to-date (YTD) basis, driven by massive investments in its AI infrastructure.

What Are You Actually Buying When You Invest in NBIS Stock?

Nebius combines traditional neocloud data centers with its own hardware designs and cloud software solutions. The company’s standing as an AI infrastructure provider has strengthened significantly in recent months, as tech firms race to secure data center capacity to train and run AI models. It had primarily catered to smaller clients such as AI startups, but that changed dramatically last September when Microsoft agreed to buy $17.4 billion worth of capacity over five years. Earlier this week, Nebius secured a cloud-computing deal with Meta Platforms valued at up to $27 billion, which I’ll discuss in more detail later. But first, let’s take a closer look at what Nebius actually does.

Nebius operates AI data centers designed for high-performance computing and AI workloads. The company offers rapid access to large clusters of Nvidia (NVDA) GPUs, including Blackwell and H200. In other words, the company rents high-performance GPU servers to customers who need to train large language models (LLMs) or perform AI inference using pre-trained models. So it’s not really any different from other neocloud providers, right?

However, the key differentiator is that Nebius designs its own data centers, server racks, and cooling systems in-house. By designing its own hardware, Nebius claims about 20% lower electricity consumption than competitors and achieves 100% compute utilization in its clusters, allowing it to offer higher performance at a lower cost. Notably, Nebius deploys modular data centers in cold climates (e.g., Finland) for natural cooling efficiency. Meanwhile, Nebius also provides specialized, high-speed storage solutions that deliver the high read/write throughput needed for large foundational model training.

Beyond just providing hardware, Nebius offers a full-stack platform that simplifies the AI development lifecycle. The company has Nebius Token Factory, a high-performance managed inference platform designed to deploy, optimize, and run open-source LLMs at scale, featuring pay-per-token pricing and high-throughput autoscaling. It also offers AI Studio, a platform that enables researchers and developers to fine-tune models, experiment with open-source models, and deploy them using APIs. In addition, the company offers managed Kubernetes and SLURM orchestration to make it easier to manage intensive AI training workloads.

It is also important to note that Nebius is a Preferred Reference Platform Cloud Partner of Nvidia, giving it early access to next-gen chips and engineering collaboration. The company has said it will be among the first AI cloud providers globally to deploy Nvidia’s Vera Rubin NVL72 systems this year.

Nebius Surges on Meta Deal Before Plunging on Bond Offering

On Monday, Nebius shares surged about +15% after the company announced a cloud-computing deal with Meta Platforms that could be worth up to $27 billion. Nebius will supply $12 billion in dedicated capacity to Meta across multiple locations, based on Nvidia’s next-generation Vera Rubin platform, beginning in early 2027.

In connection with access to these Vera Rubin deployments, Meta has committed to buying additional available compute capacity across select upcoming Nebius clusters, totaling up to $15 billion over five years. Nebius said it plans to sell this capacity to third-party customers of its AI cloud business, with any remaining capacity to be acquired by Meta.

D.A. Davidson analyst Alexander Platt said the Meta deal reinforces Nebius’ status as a leading neocloud provider and is unlikely to be the last hyperscaler deal the company secures. “This new agreement continues to validate Nebius as one of the leading neocloud players, alongside CoreWeave,” Platt said. “We believe the company is well-positioned to bring on at least another customer of similar size to at least the Microsoft contract.”

Meanwhile, Nebius said last week that it would receive a $2 billion investment from Nvidia to support the deployment of more than five gigawatts of computing capacity by the end of 2030.

However, Nebius investors did not celebrate for long, as the stock plunged more than -10% on Tuesday, giving up most of its Meta deal-related gains after the company announced plans to raise $3.75 billion through convertible bonds. The company priced an upsized private offering of $4.0 billion in convertible senior notes on Wednesday. Nebius said it intends to use the money to fuel its growth, including building and expanding data centers, enhancing its AI cloud platform, buying key hardware such as GPUs, and supporting general corporate purposes.

How Did Nebius Perform in Q4?

The company released its fourth-quarter financial results on Feb. 12. Its total revenue stood at $227.7 million, up 547% year-over-year (YoY). The growth was largely driven by continued strong demand for compute capacity across customer types and regions. Notably, core AI cloud revenue, accounting for the bulk of the company’s total revenue, grew even faster, surging 800% YoY to $214.2 million. The company said it operated at peak utilization during the quarter and was fully sold out of capacity in Q4. However, the top-line figure fell short of the consensus estimate of $242.79 million. The company’s Q4 adjusted net loss widened to -$173 million, compared with -$69 million in the same period a year earlier.

Meanwhile, Nebius’ annualized run-rate revenue (ARR), calculated by annualizing the final month’s revenue of the quarter, stood at $1.25 billion, well above the company’s guidance. The company expects to reach an ARR of $7 billion to $9 billion by year-end. The company also noted it closed the year with roughly 170 MW of active power, significantly exceeding its 100 MW target.

CEO Arkady Volozh said capital expenditures totaled about $2.1 billion in Q4, primarily driven by purchases of GPUs and related hardware, as well as data center expansion efforts, including investments in planned greenfield sites. Management also said it is confident in its ability to deliver on the increased target of more than 3 GW of contracted power by the end of 2026. The company also plans to reach between 800 MW and 1 GW of connected power by the end of this year.

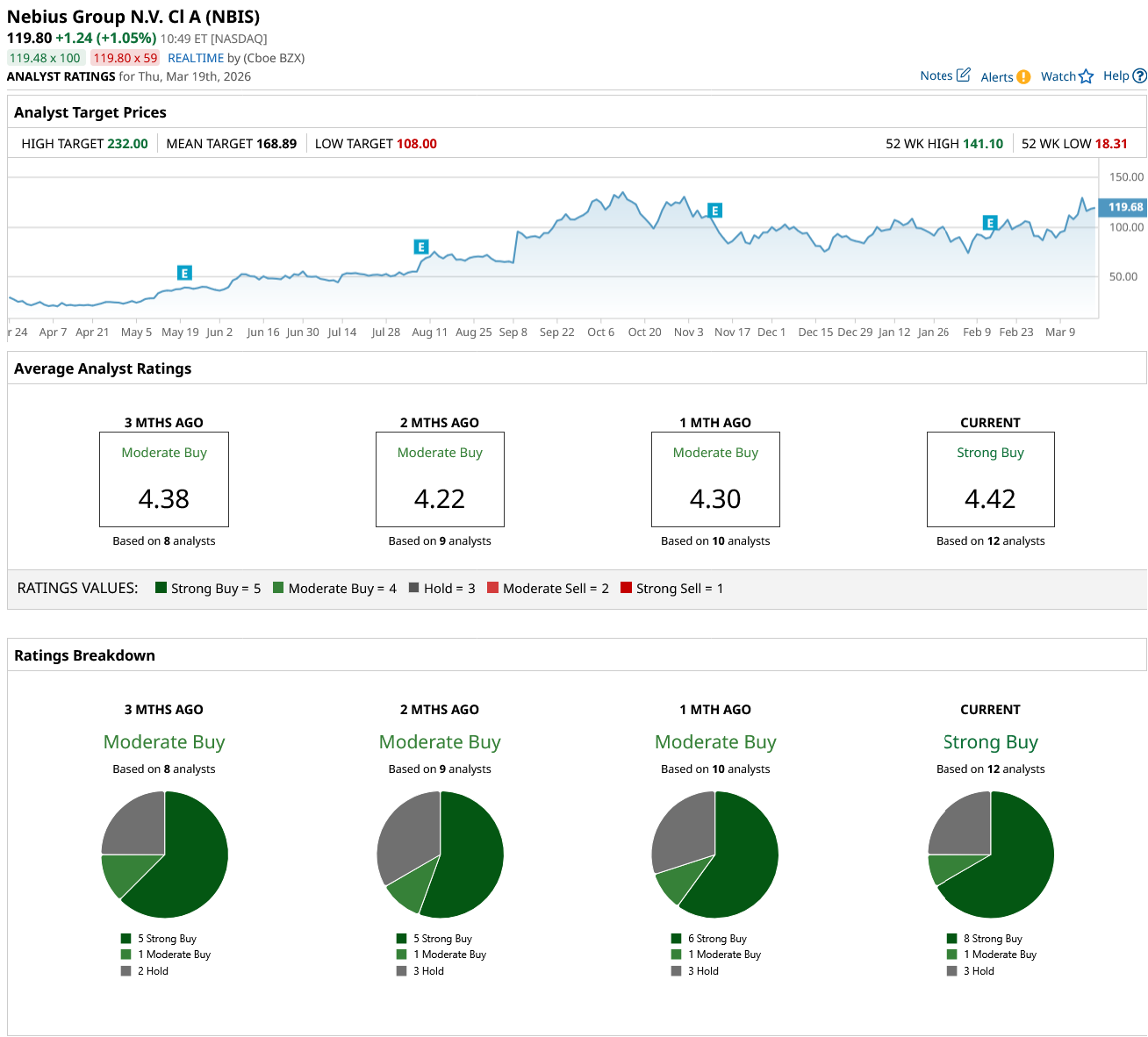

What Do Analysts Expect for NBIS Stock?

Wall Street analysts are highly bullish on Nebius, awarding the stock a “Strong Buy” consensus rating. Of the 12 analysts covering NBIS stock, eight rate it a “Strong Buy,” one assigns a “Moderate Buy” rating, and three recommend holding. The average price target for NBIS stock is $168.89, indicating a potential upside of 41% from current levels.

On Monday, Citi initiated coverage of NBIS stock with a “Buy” rating and a $169 price target. “Nebius positions itself as an emerging AI hyperscaler, not just a GPUaaS provider, with a full‑stack architecture that spans custom data center design, in‑house hardware, orchestration, and an expanding inference and agentic services layer,” Citi analyst Tyler Radke said.

On the date of publication, Oleksandr Pylypenko had a position in: META , NVDA . All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Microsoft%20headquarters%20By%20Peter.jpeg)

/Apple%20products%20on%20desk%20by%20Ake%20Ngiamsanguan%20via%20iStock.jpg)

/Nvidia%20logo%20by%20Konstantin%20Savusia%20via%20Shutterstock.jpg)