/Akamai%20Technologies%20Inc%20logo%20on%20building-by%20Sundry%20Photography%20via%20Shutterstock.jpg)

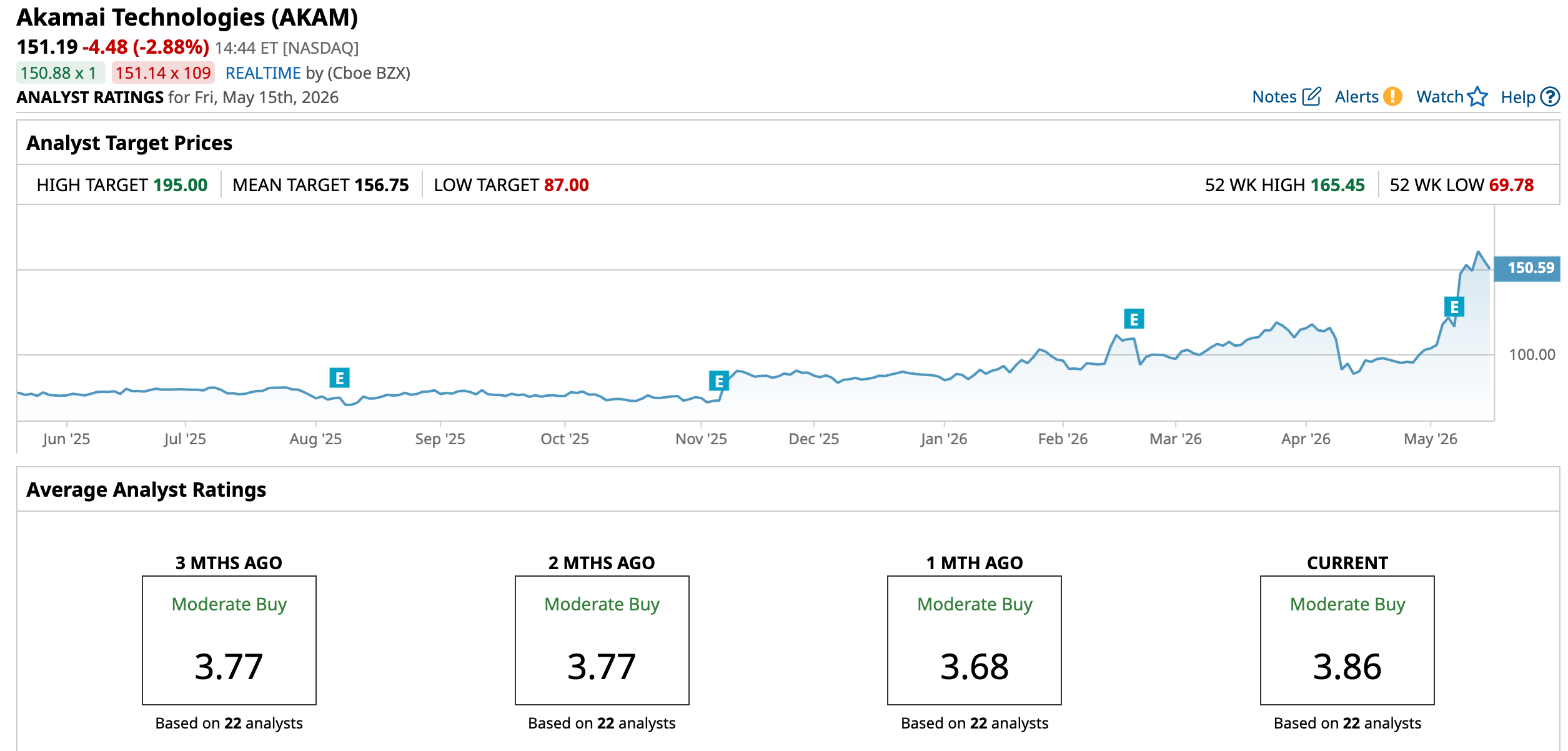

Shares of Akamai Technologies (AKAM) are surging after a major vote of confidence from Bank of America signaled that Wall Street may finally be rethinking the company’s identity. Long viewed as a mature delivery network provider, Akamai is increasingly being recognized as a serious player in AI infrastructure and edge computing, prompting BofA to upgrade the stock to “Buy” from “Neutral” while sharply raising its price target to $175 from $130.

The bullish call comes as investors digest Akamai’s accelerating transformation from a legacy internet-services company into a fast-growing cloud and artificial intelligence (AI) infrastructure platform. Analysts pointed to the company’s recent $1.8 billion cloud infrastructure agreement, reportedly tied to AI workloads, as evidence that Akamai is beginning to win meaningful business in the rapidly expanding AI ecosystem.

With demand rising for distributed AI computing, edge inference, and cloud infrastructure outside traditional hyperscalers, Wall Street is starting to view Akamai as a potential beneficiary of the next wave of AI spending.

About Akamai Stock

Akamai Technologies is a cloud computing and cybersecurity company best known for its global content delivery network (CDN), edge computing infrastructure, and internet security solutions. Founded in 1998 and headquartered in Cambridge, Massachusetts, the company serves enterprises worldwide with services spanning cloud infrastructure, API security, DDoS protection, and AI-ready edge computing platforms.

Once viewed primarily as a legacy internet infrastructure provider, Akamai is increasingly repositioning itself as a next-generation AI and cloud infrastructure player following major investments in distributed computing and large-scale AI workloads. The company currently has a market cap of $22.6 billion.

Shares of Akamai have staged a remarkable rally in 2026 as investors increasingly embrace the company’s transition from a legacy content delivery network provider into an AI and cloud infrastructure play. The stock is now up 72.79% year-to-date (YTD) and has surged 97% over the past 52 weeks, making it one of the best-performing infrastructure software names in the market.

Momentum accelerated sharply in May after Akamai disclosed a massive $1.8 billion AI cloud infrastructure agreement tied to a leading frontier AI model provider. On May 8, the stock exploded 26.6% intraday following the announcement and stable quarterly results, triggering a major re-rating from Wall Street analysts.

The stock has been seeing sharp spikes lately. Shares jumped another 7.7% intraday on May 13, after Bank of America upgraded the stock to “Buy” and raised its price target to $175, arguing that Akamai should no longer be viewed as a legacy internet company but as an emerging AI infrastructure platform. Moreover, the stock hit a fresh 52-week high of $165.45 on May 13.

Over the past five trading sessions alone, Akamai shares increased 2.06%, fueled by analyst upgrades, growing enthusiasm around edge AI computing, and optimism surrounding the company’s rapidly expanding cloud infrastructure business. However, the stock saw a pullback of 3% in the last session.

AKAM currently trades at a premium compared to the sector median and its own historical average at 36.36 times forward earnings.

Cloud Business Gaining Traction

Akamai Technologies reported its first-quarter 2026 financial results on May 7. The company posted first-quarter revenue of $1.1 billion, up 6% year-over-year (YOY). The strongest performance came from Cloud Infrastructure Services (CIS), where revenue surged 40% YOY to $95 million, highlighting Akamai’s growing positioning in AI and cloud computing infrastructure.

Security revenue climbed 11% YOY to $590 million, continuing to be the company’s largest and most profitable segment. Meanwhile, delivery and other cloud applications revenue declined 7% YOY to $389 million.

Profitability metrics were mixed as Akamai increased investments in GPU infrastructure and AI cloud capacity. Non-GAAP operating income declined 8% YOY to $283 million, while non-GAAP operating margin compressed to 26% from 30% in Q1 2025. Non-GAAP EPS came in at $1.61, down 5% YOY. Adjusted EBITDA declined 3% YOY to $427 million.

Operationally, the biggest development was Akamai’s announcement that a “leading U.S.-based frontier model provider” committed $1.8 billion over seven years for cloud infrastructure services. Reports later indicated the customer was Anthropic, marking one of the largest AI infrastructure agreements in Akamai’s history. The deal acts as validation that the company is becoming a meaningful AI infrastructure provider.

Another notable strategic shift was Akamai’s decision to begin reporting Cloud Infrastructure Services as a standalone revenue category for the first time, underscoring management’s intention to position the segment as a primary long-term growth engine.

Furthermore, Akamai issued second-quarter 2026 revenue guidance of $1.075 billion to $1.10 billion and projected non-GAAP EPS between $1.45 and $1.65. For the full year 2026, the company expects revenue between $4.445 billion and $4.55 billion and non-GAAP EPS of $6.40 to $7.15, while forecasting a non-GAAP operating margin of around 26%.

Analysts forecast EPS of $4.15 for fiscal 2026, a 5.9% decline, followed by a 13% rise to $4.69 in 2027.

What Do Analysts Expect for Akamai Stock?

In addition to Bank of America, many other analysts have shown optimism around the company’s prospects.

Recently, Morgan Stanley raised its price target on Akamai to $165 from $120 while maintaining an “Overweight” rating, citing accelerating momentum toward double-digit growth.

Also, DA Davidson raised its price target on Akamai to $185 from $125 while maintaining a “Buy” rating, citing surging demand for the company’s AI-focused Cloud Infrastructure Services business.

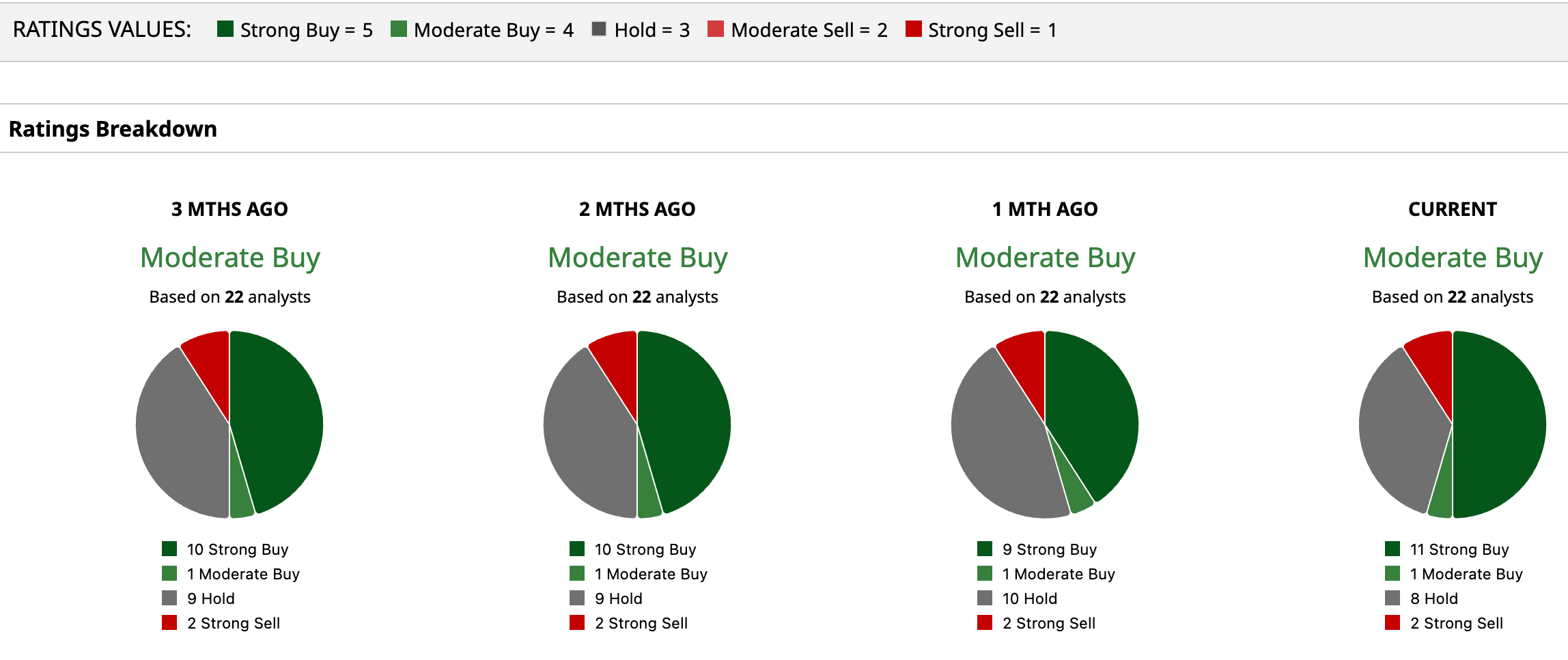

Overall, AKAM has a consensus “Moderate Buy” rating. Of the 22 analysts covering the stock, 11 advise a “Strong Buy,” one suggests a “Moderate Buy,” eight analysts are on the sidelines, giving it a “Hold” rating, and two recommend a “Strong Sell.”

With the average analyst price target of $156.75, Akamai shows a 3.7% upside. while the Street-high target price of $195 suggests that the stock could rally as much as 29%.

On the date of publication, Subhasree Kar did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Alphabet%20Inc_%20and%20Google%20logos%20by%20IgorGolovinov%20via%20Shutterstock.jpg)

/Technological%20process%20of%20soldering%20chip%20components%20on%20PCB%20board%20by%20I%20Viewfinder%20via%20Adobe%20Stock.jpeg)