Aflac has been treading water for the past six months, recording a small return of 0.8% while holding steady at $115.26. The stock also fell short of the S&P 500’s 9.9% gain during that period.

Is there a buying opportunity in Aflac, or does it present a risk to your portfolio? Dive into our full research report to see our analyst team’s opinion, it’s free.

Why Do We Think Aflac Will Underperform?

We don't have much confidence in Aflac. Here are three reasons you should be careful with AFL and a stock we'd rather own.

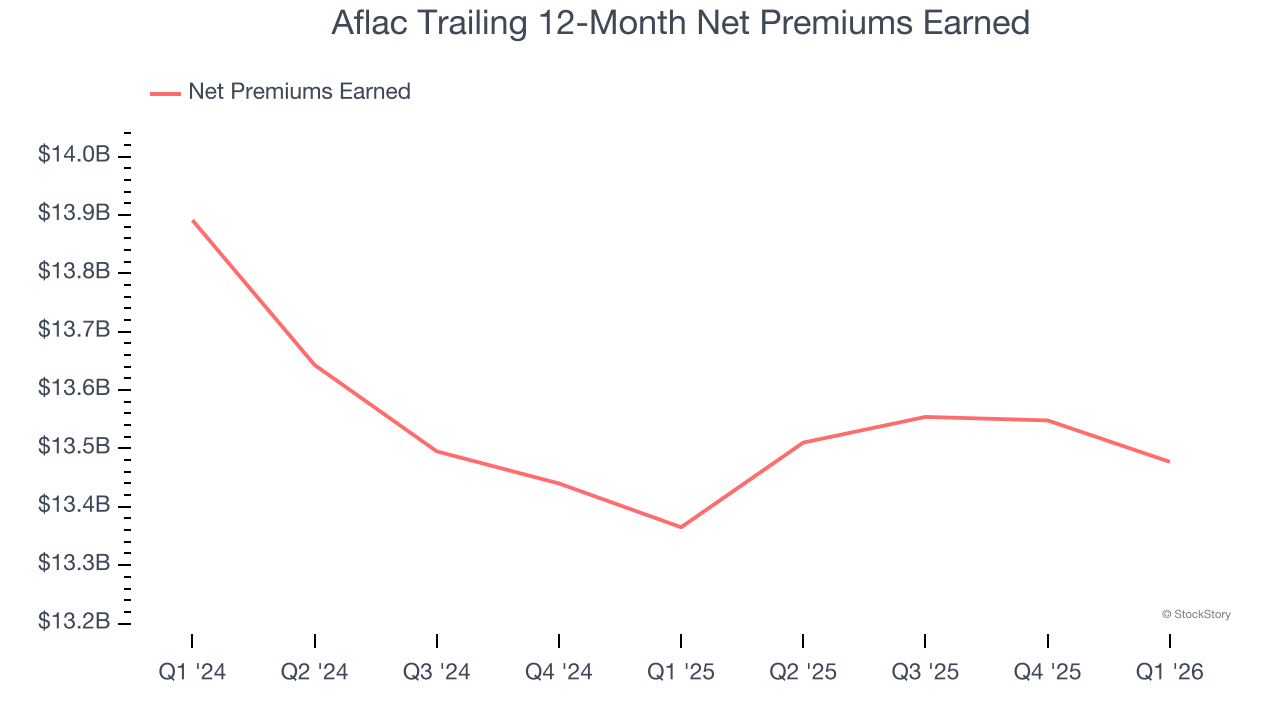

1. Declining Net Premiums Earned Reflect Weakness

When insurers sell policies, they protect themselves from extremely large losses or an outsized accumulation of losses with reinsurance (insurance for insurance companies). Net premiums earned are therefore net of what’s ceded to reinsurers as a risk mitigation and transfer strategy.

Aflac’s net premiums earned has declined by 6.2% annually over the last five years, much worse than the broader insurance industry. This shows that policy underwriting underperformed its other business lines.

2. Revenue Projections Show Stormy Skies Ahead

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect Aflac’s revenue to drop by 2.7%, a decrease from its flat result for the past two years. This projection is underwhelming and indicates its products and services will see some demand headwinds.

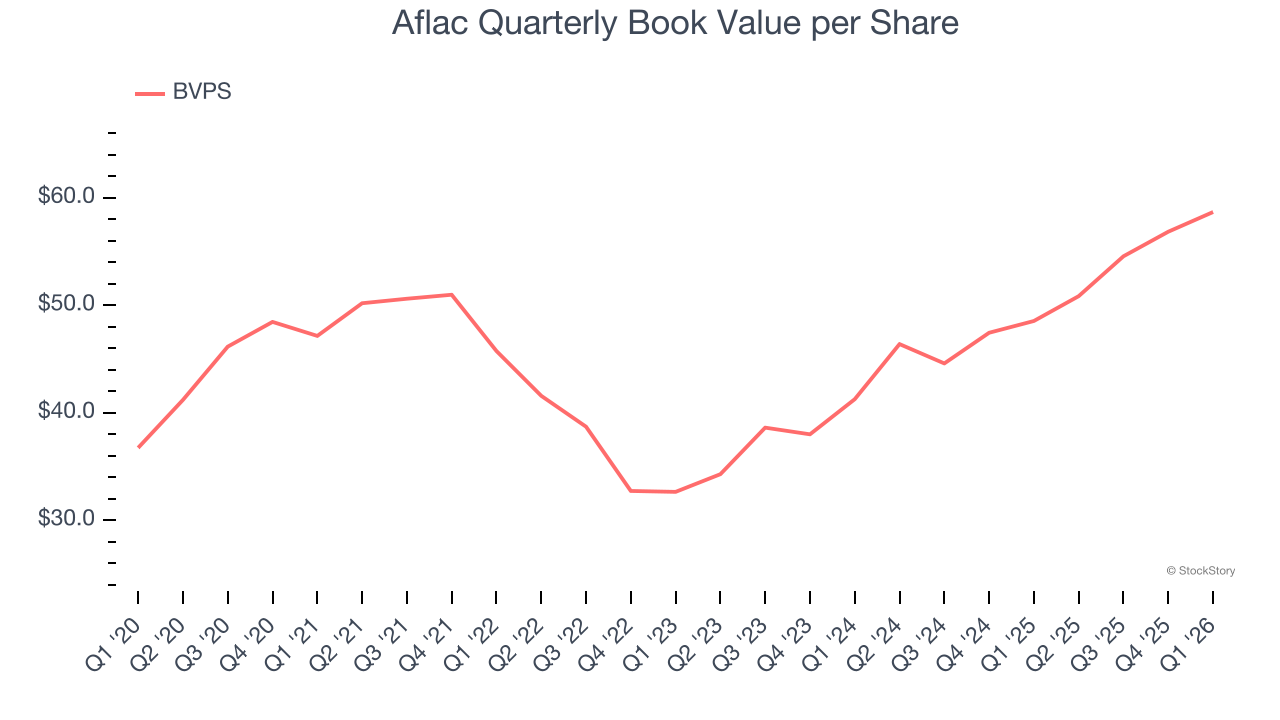

3. BVPS Projections Show Stormy Skies Ahead

An insurer’s book value per share (BVPS) increases when it maintains a profitable pre-tax profit margin and effectively manages its investment portfolio.

Over the next 12 months, Consensus estimates call for Aflac’s BVPS to shrink by 4.8% to $54.37, a sour projection.

Final Judgment

We see the value of companies helping consumers, but in the case of Aflac, we’re out. With its shares lagging the market recently, the stock trades at 2× forward P/B (or $115.26 per share). This valuation tells us it’s a bit of a market darling with a lot of good news priced in - we think there are better opportunities elsewhere. We’d suggest looking at one of Charlie Munger’s all-time favorite businesses.

Stocks We Like More Than Aflac

WHILE YOU’RE HERE: Top 9 Market-Beating Stocks. The best stocks don't just beat the market once. They do it again. And again. Robust revenue growth, rising free cash flow, returns on capital that leave their competition in the dust. The market has already rewarded these businesses.

But our AI platform says the party isn't over. Find out which 9 stocks made the cut this week - FREE. Get Our Top 9 Market-Beating Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.

/Alphabet%20Inc_%20and%20Google%20logos%20by%20IgorGolovinov%20via%20Shutterstock.jpg)

/Technological%20process%20of%20soldering%20chip%20components%20on%20PCB%20board%20by%20I%20Viewfinder%20via%20Adobe%20Stock.jpeg)