/Broadcom%20Inc%20logo%20on%20building-by%20Poetra_%20RH%20via%20Shutterstock.jpg)

Artificial intelligence (AI) has become the defining force behind the stock market’s rally in recent years, reshaping industries and creating enormous demand for next-generation computing power. At the center of that transformation is the semiconductor industry, where companies supplying the backbone of AI infrastructure have emerged as some of Wall Street’s biggest winners. One name leading that charge is Broadcom (AVGO).

Best known for its diversified chip and software business, Broadcom is rapidly cementing itself as a dominant AI player through its custom AI accelerators. The company has partnered with several hyperscalers to design specialized AI chips that can deliver significant cost and efficiency advantages over traditional GPU-based systems used for AI training and inference. That strategy has become a major catalyst behind Broadcom’s explosive rally.

The company has already secured high-profile custom silicon partnerships with Meta (META) and Alphabet (GOOG) (GOOGL) while OpenAI has also teamed up with Broadcom on custom AI accelerators following an agreement signed last October. As hyperscalers increasingly look for cheaper and more power-efficient alternatives to traditional AI hardware, Broadcom appears well-positioned to capture a larger share of the booming AI infrastructure market.

Now, with Broadcom already established as one of the biggest beneficiaries of the AI boom, investors are eagerly awaiting the company’s fiscal 2026 second-quarter earnings report, set for release on Wednesday, June 3, after the closing bell. Thus, ahead of this event, here’s a closer look at AVGO stock.

About Broadcom Stock

Headquartered in San Jose, Broadcom has quietly become one of the most influential companies powering the digital economy. Unlike consumer-facing tech giants, Broadcom largely operates behind the scenes, supplying the chips and infrastructure software that keep data centers, broadband networks, enterprise systems, and cloud platforms running. Its business combines a vast semiconductor portfolio focused on connectivity and data processing with an expanding infrastructure software segment built through strategic acquisitions.

That positioning has placed Broadcom at the heart of some of the biggest trends in technology, particularly artificial intelligence and cloud computing. In 2026, much of the company’s momentum has been driven by soaring demand for custom AI accelerators and the high-speed networking hardware needed to connect massive GPU clusters powering advanced AI workloads. And investors have certainly taken notice.

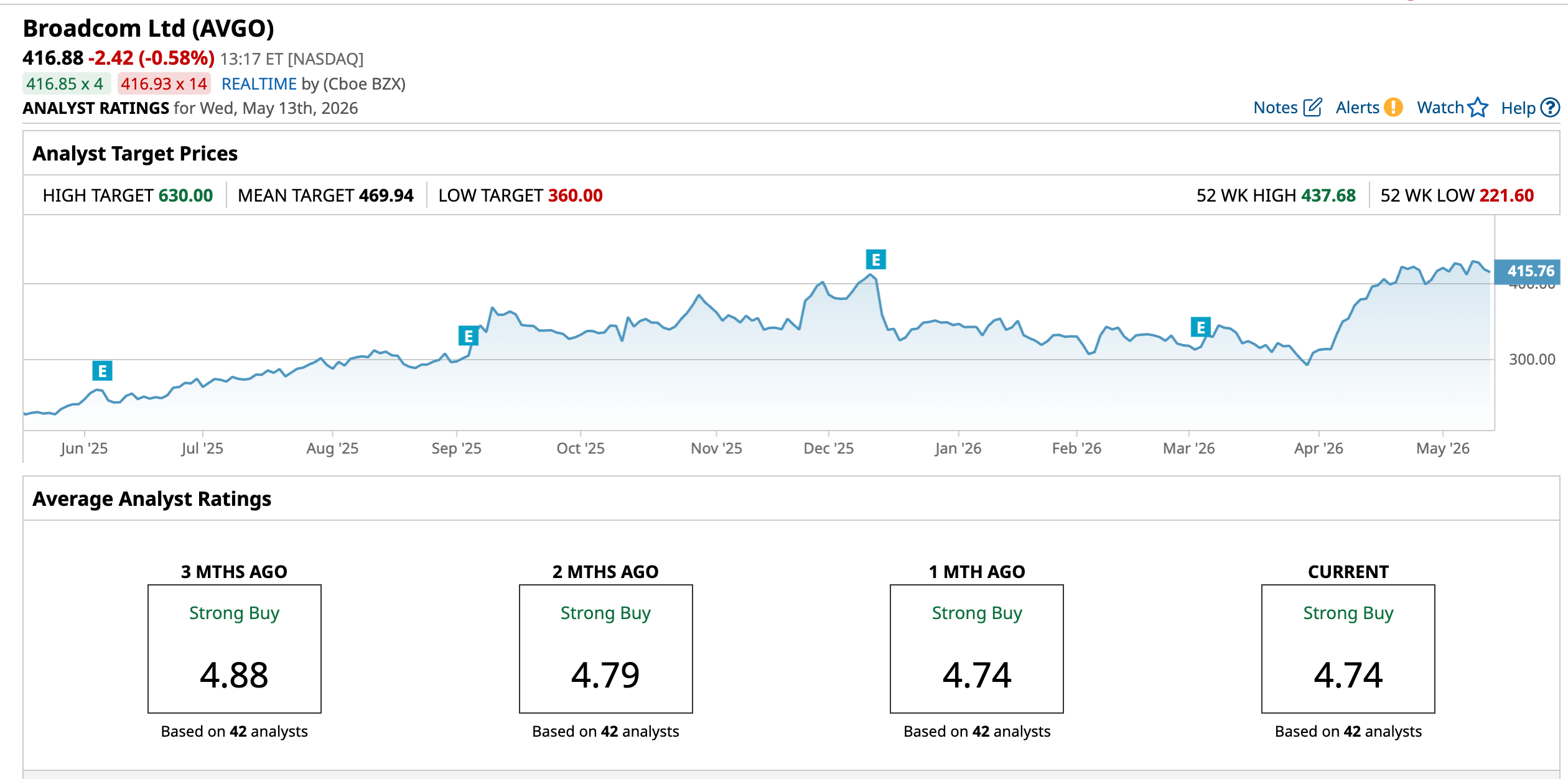

With a market capitalization approaching $2 trillion, Broadcom’s stock has rallied 78.86% over the past year, comfortably outperforming the broader S&P 500 Index’s ($SPX) 26.41% gain during the same period. The momentum has continued in 2026, with shares climbing 20.11% year-to-date (YTD) versus the broader market’s 8.7% rise. The stock also touched a record high of $437.68 recently on May 6 and currently sits only 4.7% below that level.

Boadcom’s Q1 Earnings Snapshot

Broadcom delivered a powerful start to fiscal 2026, with its first-quarter results in early March further cementing the company’s growing influence in the AI infrastructure market. Revenue climbed to a record $19.31 billion, up 29% year-over-year (YOY), driven by relentless demand for AI semiconductor solutions and slightly ahead of Wall Street’s $19.29 billion estimate.

The biggest driver of that growth was the Semiconductor Solutions segment, where revenue surged 52% annually to $12.51 billion, more than offsetting continued weakness across several non-AI legacy businesses. AI-related semiconductor revenue stood out once again, skyrocketing 106%YOY to $8.4 billion as demand for custom AI accelerators and AI networking hardware remained exceptionally strong.

Broadcom’s Infrastructure Software segment, strengthened by the company’s 2023 acquisition of VMware, generated $6.8 billion in revenue during the quarter. Growth in the segment was relatively modest at 1% YOY, largely reflecting VMware’s ongoing transition away from perpetual licenses toward a subscription-based business model.

Profitability remained equally impressive. Adjusted EBITDA rose 30% from the prior year to a record $13.1 billion, representing 68% of total revenue. Non-GAAP earnings came in at $2.05 per share, up 28% YOY and slightly above analysts’ consensus estimate of $2.04 per share. The company ended the quarter with $14.17 billion in cash and cash equivalents, compared to $16.18 billion in the previous quarter.

Additionally, Broadcom generated $8.26 billion in operating cash flow and spent just $250 million on capital expenditures, resulting in free cash flow of $8.01 billion, a 33% increase from the prior year. That strong cash generation continued to fuel aggressive shareholder returns, with the company returning $10.9 billion during the quarter through $3.1 billion in dividends and nearly $7.8 billion in share repurchases.

With Broadcom’s next earnings report now on the horizon, investors will be closely watching whether the company can sustain its explosive AI-driven growth trajectory. For fiscal second-quarter 2026, the company projected revenue of roughly $22 billion, while adjusted EBITDA is expected to remain near 68% of revenue. And, management forecast another sharp acceleration in AI demand, guiding for AI semiconductor revenue of approximately $10.7 billion in the upcoming quarter.

What Do Analysts Think About Broadcom Stock?

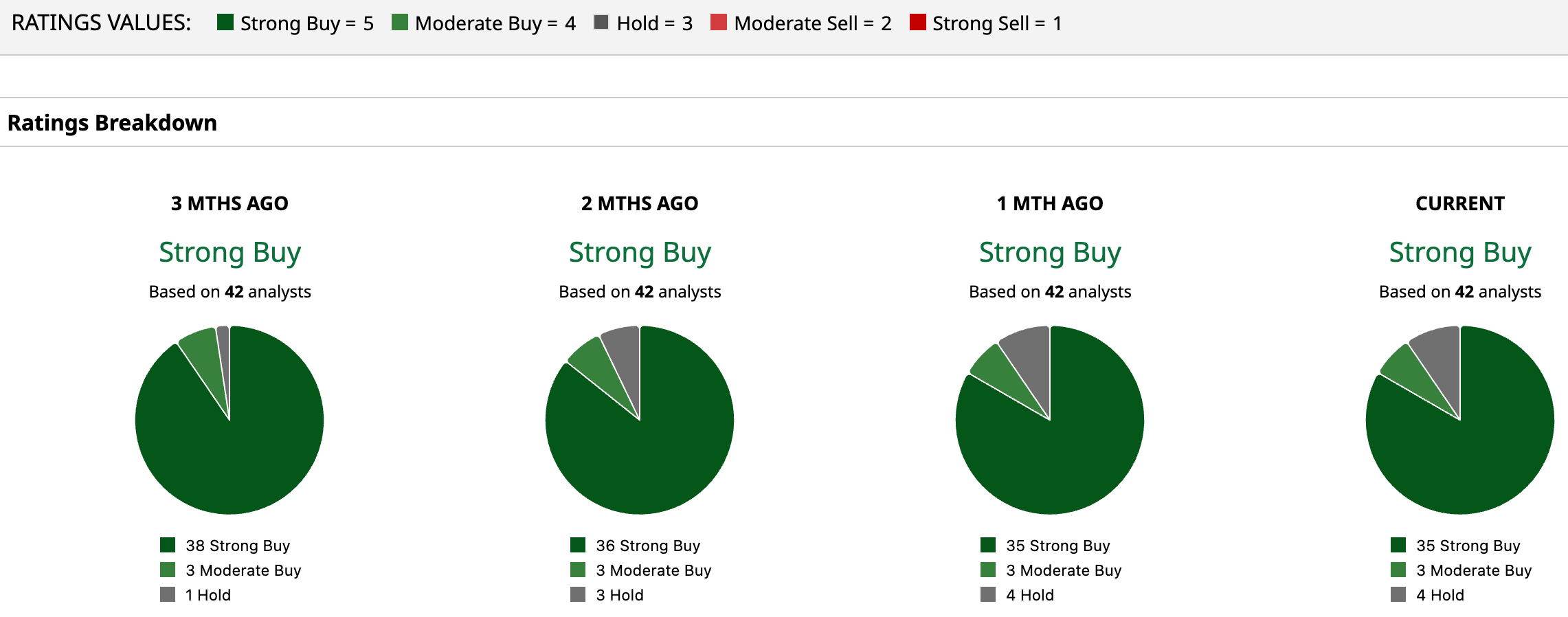

As Broadcom’s next earnings report draws closer, Wall Street continues to grow increasingly optimistic about the AI giant’s long-term potential. The stock currently holds a consensus “Strong Buy” rating, with 35 of the 42 analysts covering Broadcom issuing “Strong Buy” recommendations, while three rate it “Moderate Buy” and only four remain on the sidelines with “Hold” ratings.

Even after the stock’s massive rally, analysts still see room for further upside. The average price target of $469.94 implies 12.7% upside from current levels, while the Street-high target of $630 suggests the stock could climb another 51.1% from here.

On the date of publication, Anushka Mukherji did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20Palantir%20office%20building%20in%20Tokyo_%20Image%20by%20Hiroshi-Mori-Stock%20via%20Shutterstock_.jpg)

/A%20hand%20holding%20a%20phone%20with%20the%20Reddit%20logo_%20Mamun_Sheikh%20via%20Shutterstock_.jpg)

/The%20CoreWeave%20logo%20displayed%20on%20a%20smartphone%20screen_%20Image%20by%20Robert%20Way%20via%20Shutterstock_.jpg)

/BlackRock's%20global%20headquarters%20By%20Tada%20Images.jpeg)

/Apple%20logo%20on%20store%20front%20by%20frantic00%20via%20iStock.jpg)