/Advanced%20Micro%20Devices%20Inc_%20office%20sign-by%20Poetra_RH%20via%20Shutterstock.jpg)

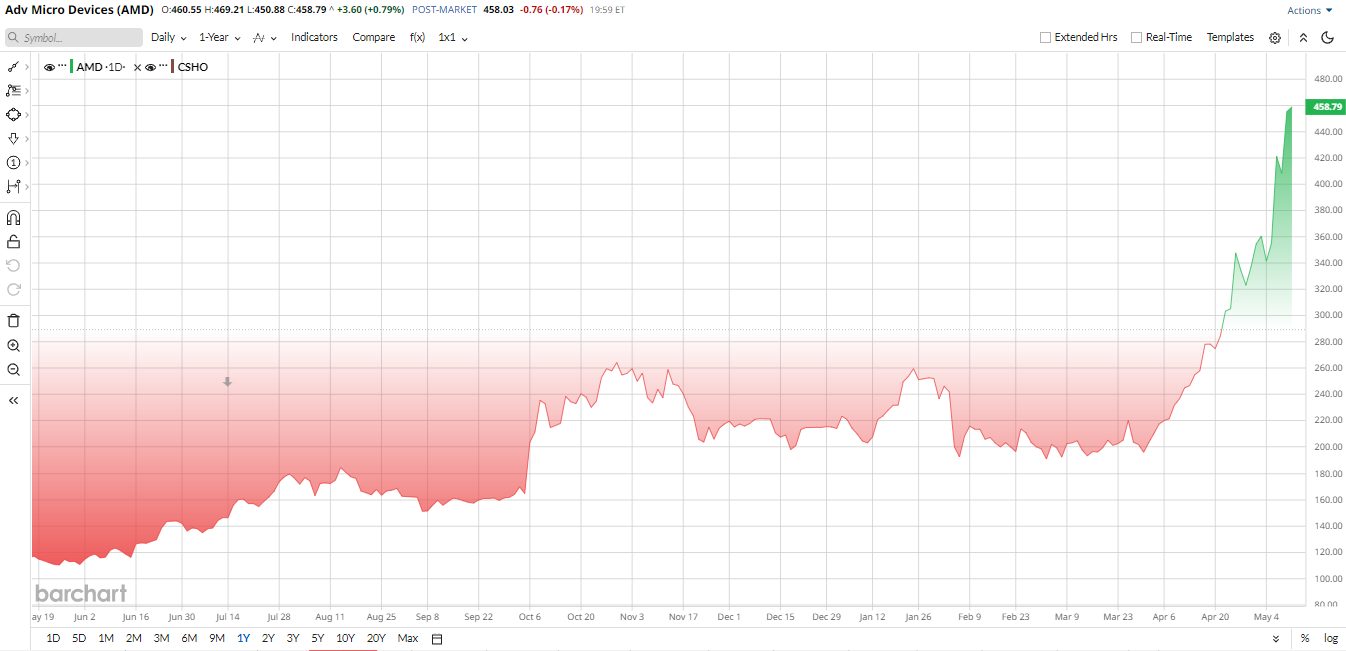

Advanced Micro Devices (AMD) has become one of the most closely watched stocks in the semiconductor market. After a choppy start to 2026, the AI trade regained momentum in April, and AMD quickly joined the rally. AMD stock has pushed to fresh highs as investors have grown more convinced that the company is not just playing catch-up in AI but could be standing at the center of a much bigger long-term shift in data-center spending.

That is where the new bull case comes in. GF Securities recently argued that AMD is a key beneficiary of a “server CPU super cycle,” where server processors become a major backbone of AI infrastructure. The firm sees the server CPU market expanding from roughly $26 billion in 2025 to $135 billion by 2030. AMD already holds about 41% revenue share in server CPUs, so it is well-positioned if that growth plays out.

In other words, the market is not just rewarding AMD for what it has already done — it is also pricing in what this business could become over the next several years.

How Is AMD Stock Performing?

The move in AMD stock has been impressive. Shares are up more than 300% over the past year and up roughly 104% year-to-date (YTD). That kind of gain does not happen without a powerful story behind it. A big part of the move comes from AI demand, stronger data-center revenue, and the idea that large customers want a second source beyond Nvidia (NVDA). When investors see demand stretching into 2027 and beyond, they tend to pay up for the stock.

The valuation is still hard to ignore, however. AMD is not cheap by normal standards. Shares trade at more than 126 times trailing earnings and around 21 times sales, which is rich compared with the broader semiconductor group. Even so, the premium starts to look more reasonable when you compare it with AMD’s growth.

On forward estimates, AMD trades at about 62 times 2026 earnings and around 35 times 2027 earnings. That is still expensive, but it is easier to justify if the CPU and AI cycle keep building.

AMD Topped Q1 Earnings Estimates

Advanced Micro Devices' first-quarter 2026 results gave AMD stock another lift. Revenue came in at $10.3 billion, up 38% from a year earlier and ahead of Wall Street expectations. Adjusted EPS rose 43% to $1.37 per share, also above estimates.

Free cash flow was the standout. AMD generated a record $2.56 billion in quarterly free cash flow, more than triple the level from a year ago. The data-center segment led the way, with revenue of $5.77 billion, up 57% year-over-year (YOY). Client and gaming revenue also improved, while the embedded segment added another layer of support.

Management also provided upbeat guidance in the Q1 report. AMD guided Q2 revenue to $11.2 billion, above analyst expectations and a sign that demand remains strong. That outlook matters because it suggests the company is not seeing a slowdown in the near term, even after such a sharp run in the stock.

Analysts Are Turning More Bullish on AMD Stock

Now to the part that Wall Street is watching closely. GF Securities believes AMD’s server CPU business could grow 73% in 2026, pointing to tight supply and surging demand from AI infrastructure customers as major drivers.

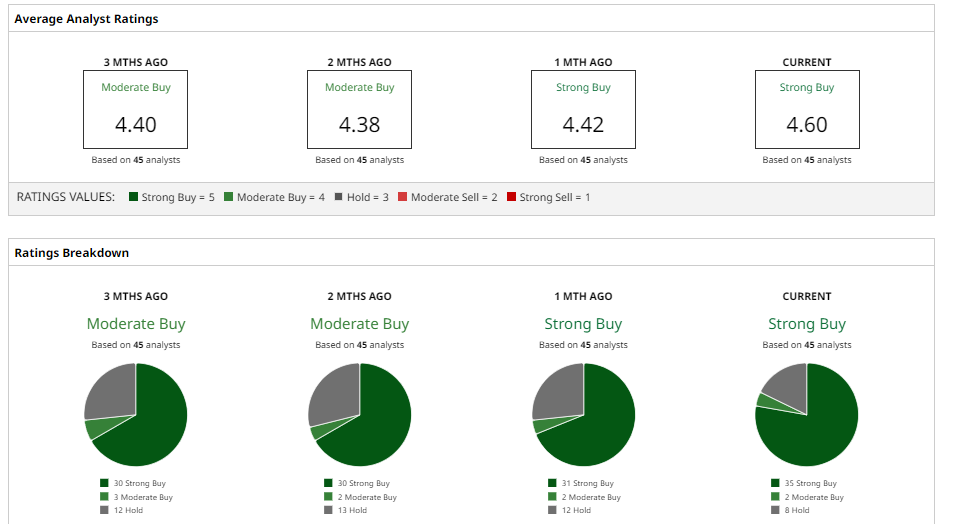

Other analysts have raised their targets on AMD stock. Goldman Sachs recently set a $450 price target on AMD, while Wedbush and Stifel followed with raises to $450 as well. Similarly, DA Davidson moved its price target to $425. Overall, the stock has a consensus “Strong Buy” rating from Wall Street. The average price target of $442.44 represents potential upside of 3% from current levels.

The message is clear: AMD is no longer just a comeback story. Instead, it is being treated as a long-term AI infrastructure winner.

On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Apple%20products%20on%20desk%20by%20Ake%20Ngiamsanguan%20via%20iStock.jpg)