/Intel%20Corp_%20Santa%20Clara%20campus-by%20jejim%20via%20Shutterstock.jpg)

Intel (INTC) stock has been on a solid run, extending its rally in 2026. Shares have climbed 89% over the past month and 433% in the past 12 months, reflecting renewed investor confidence in the company’s turnaround strategy and its growing role in the artificial intelligence (AI) ecosystem.

The latest boost to the rally came after The Wall Street Journal reported that Intel has reached a preliminary agreement with Apple (AAPL) to manufacture some of the chips used in Apple devices. According to reports, discussions between the two companies have been ongoing for the past several months.

If finalized, the partnership could represent a major milestone for Intel’s foundry ambitions and signal stronger industry confidence in its manufacturing capabilities.

Intel has been focusing on transforming its foundry business, aiming to rebuild its position as a leading chip manufacturer for both internal and external customers. The rapid expansion of AI infrastructure across the technology sector has created a significant opportunity for Intel to establish itself as a major supplier of advanced semiconductor manufacturing services.

Notably, Intel Foundry generated $5.4 billion in revenue in the first quarter, marking a 20% sequential increase driven by higher Extreme Ultraviolet (EUV) wafer production. External foundry revenue reached $174 million during the quarter. However, the segment continues to report significant losses. Nonetheless, management expects Intel Foundry’s operating loss to improve in the coming quarters.

Investor enthusiasm around Intel also intensified after it confirmed participation in Elon Musk’s Terafab project.

Intel Is Set to Benefit From Solid Demand

Intel appears to be regaining momentum after years of operational setbacks, supported by improving demand for AI infrastructure and stronger execution across key business segments. The chipmaker delivered better-than-expected Q1 results, strengthening investor confidence that its turnaround strategy is gaining traction.

Intel reported Q1 revenue of $13.6 billion, up 7% year-over-year (YOY), with AI-related businesses contributing nearly 60% of total sales. Revenue from these operations surged 40% YOY, highlighting the company’s growing exposure to long-term AI demand trends.

A major growth driver was Intel’s Data Center and AI (DCAI) division, which generated $5.1 billion in revenue, rising 22% YOY. Demand was broad-based as enterprises increased spending on CPUs to support AI workloads, particularly as applications evolve from training models to inference and advanced agentic systems. Demand for custom AI silicon was also strong, with Application-Specific Integrated Circuits (ASICs) revenue nearly doubling YOY.

Intel further strengthened its long-term outlook by securing several strategic agreements in the DCAI segment during the quarter, including a partnership with Alphabet's (GOOGL) Google.

Profitability improved alongside Intel's revenue growth. Adjusted gross margin expanded to 41%, driven by higher sales volumes, improved product mix, and pricing actions. Adjusted earnings benefited from tighter cost controls and operating leverage.

Management expects momentum to continue. Intel forecast Q2 revenue of $13.8 billion to $14.8 billion, implying sequential growth of up to 9%, while the DCAI segment is projected to post double-digit growth. The company also expects Q2 EPS of $0.20, a sharp improvement from the loss reported a year ago.

Is Intel Stock a Buy, Sell, or Hold?

Intel’s remarkable rally reflects growing investor confidence in the company’s turnaround efforts and its expanding role in the AI infrastructure boom. Strong momentum in its DCAI business, improving profitability, strategic partnerships with major tech players like Google, and the potential Apple foundry deal have strengthened the bullish outlook for INTC stock. While Intel’s foundry division still faces profitability challenges, the company is showing signs of operational improvement and positioning itself to benefit from long-term deals.

However, the significant rally in INTC stock suggests that much of the optimism is already reflected in shares. For existing shareholders, holding INTC stock could still make sense as Intel continues executing on its recovery plans, while new investors may prefer to wait for pullbacks before building positions.

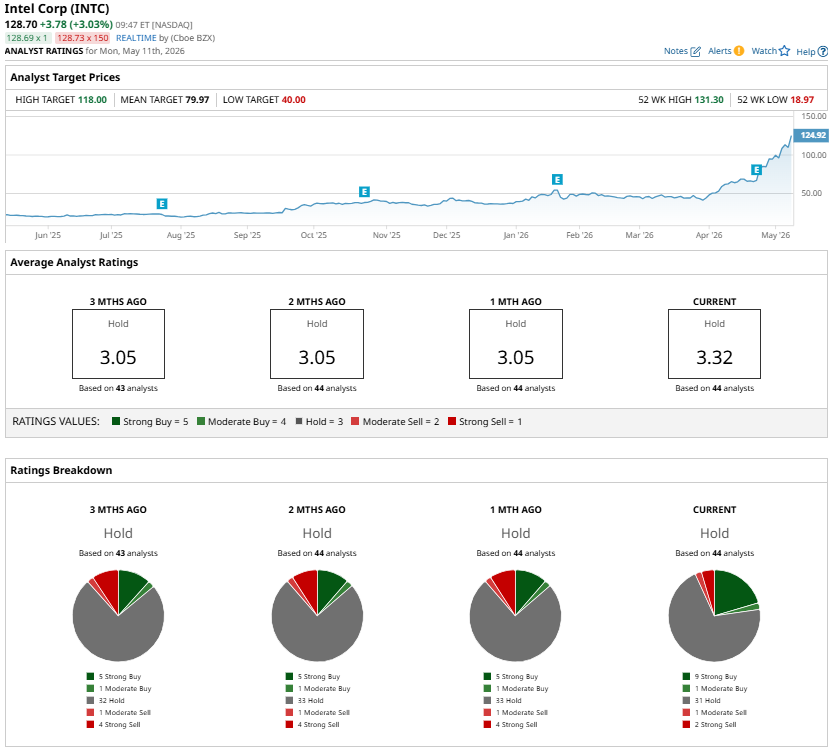

Overall, Intel stock has a consensus “Hold" rating based on 44 analysts with coverage.

On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20Palantir%20office%20building%20in%20Tokyo_%20Image%20by%20Hiroshi-Mori-Stock%20via%20Shutterstock_.jpg)

/A%20hand%20holding%20a%20phone%20with%20the%20Reddit%20logo_%20Mamun_Sheikh%20via%20Shutterstock_.jpg)

/The%20CoreWeave%20logo%20displayed%20on%20a%20smartphone%20screen_%20Image%20by%20Robert%20Way%20via%20Shutterstock_.jpg)

/BlackRock's%20global%20headquarters%20By%20Tada%20Images.jpeg)

/Apple%20logo%20on%20store%20front%20by%20frantic00%20via%20iStock.jpg)