/Teradyne%2C%20Inc_%20logo%20o%20building-by%20Michael%20Vi%20via%20Shutterstock.jpg)

Valued at a market cap of $57.4 billion, Teradyne, Inc. (TER) designs, develops, manufactures, and sells automated test systems and robotics products. The North Reading, Massachusetts-based company's diverse product portfolio includes test platforms for system-on-a-chip (SoC) devices, high-bandwidth memory (HBM), and storage systems, with a significant recent focus on supporting AI infrastructure and data center technologies.

This tech company has significantly outperformed the broader market over the past 52 weeks. Shares of TER have soared 311.6% over this time frame, while the broader S&P 500 Index ($SPX) has gained 31%. Moreover, on a YTD basis, the stock is up 76.6%, compared to SPX’s 8.3% rise.

Narrowing the focus, TER has also outpaced the State Street Technology Select Sector SPDR ETF’s (XLK) 51% rise over the past 52 weeks and 19.4% YTD uptick.

On Apr. 28, TER delivered stronger-than-expected Q1 results, yet its shares plunged 19.4% in the following trading session. The company’s net revenue grew 87% year-over-year to $1.3 billion, topping analyst estimates by 4.9%. Additionally, its adjusted EPS came in at $2.56, rising sharply from the year-ago quarter and comfortably surpassing consensus expectations of $2.11.

Despite the strong quarterly performance, investor sentiment remained weak after the release, although the stock rebounded the next day with a 12.1% gain.

For the current fiscal year, ending in December, analysts expect TER’s EPS to grow 79% year over year to $7.09. The company's earnings surprise history is promising. It topped the consensus estimates in each of the last four quarters.

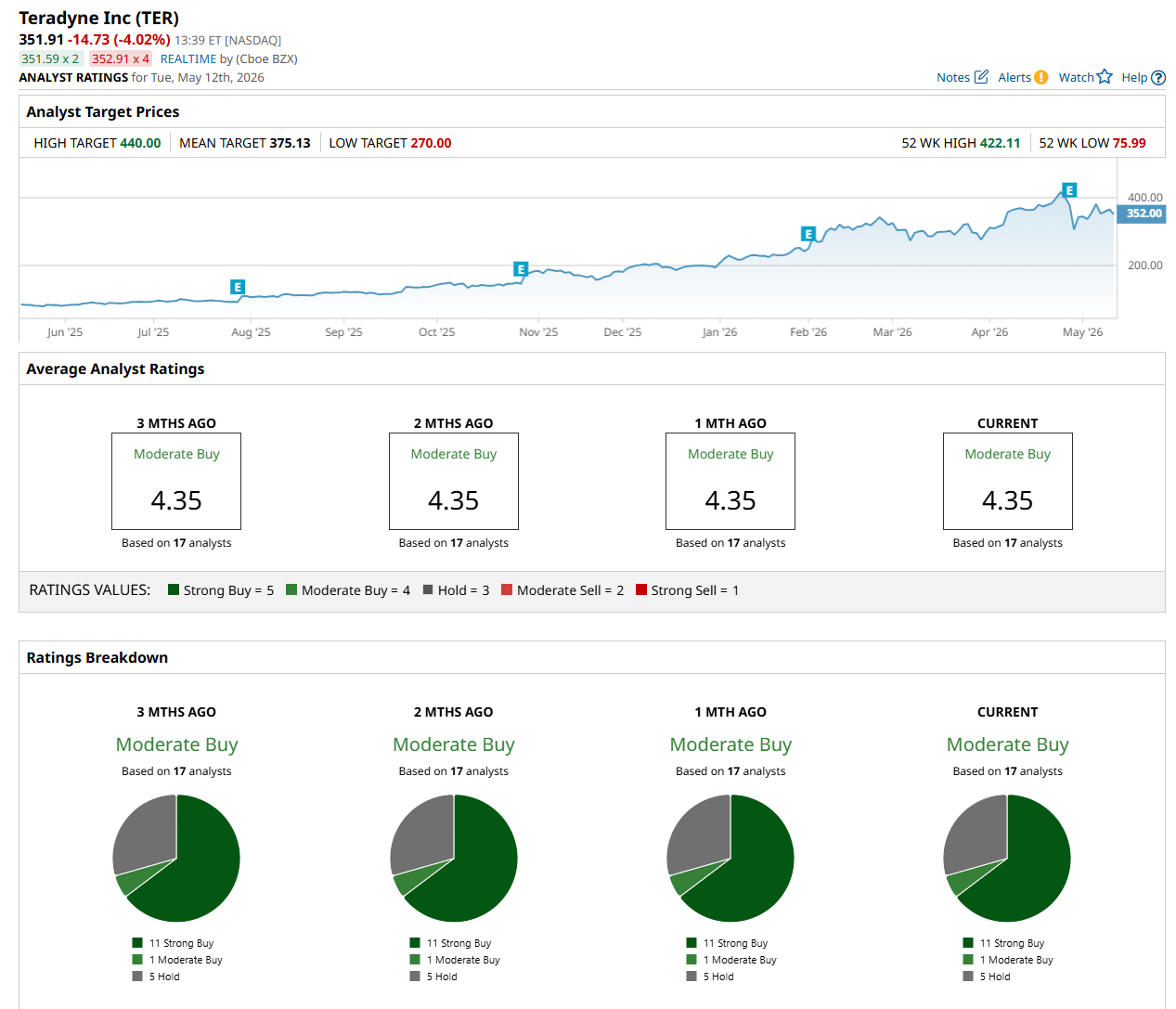

Among the 17 analysts covering the stock, the consensus rating is a "Moderate Buy,” which is based on 11 “Strong Buy,” one "Moderate Buy,” and five “Hold” ratings.

The configuration has remained consistent over the past three months.

On Apr. 30, Morgan Stanley analyst Shane Brett maintained an “Equal Weight” rating on TER and raised its price target to $387, indicating a 10% potential upside from the current levels.

The mean price target of $375.13 suggests a 6.6% premium to its current price levels, while its Street-high price target of $440 implies a 25% potential upside.

On the date of publication, Neharika Jain did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Semiconductor%20chip%20by%20Mykola%20Pokhodzhay%20via%20iStock.jpg)

/Lululemon%20Athletica%20inc_%20storefront%20by-%20Robert%20Way%20via%20iStock.jpg)