Houston, Texas-based Sysco Corporation (SYY) sells, markets, and distributes food products to restaurants, healthcare facilities, lodging establishments, and other customers who prepare meals away from home. Valued at a market cap of $34.7 billion, the company also offers non-food essentials like paper products, tableware, cookware, and restaurant equipment.

This food distributor has considerably lagged the broader market over the past 52 weeks. Shares of SYY have gained 2.6% over this time frame, while the broader S&P 500 Index ($SPX) has soared 31%. Moreover, on a YTD basis, the stock is down 1.5%, compared to SPX’s 8.3% rise.

Zooming in further, SYY has aligned with the Invesco Food & Beverage ETF’s (PBJ) 2.6% return over the past 52 weeks. However, it has underperformed PBJ’s 8.2% YTD uptick.

On Apr. 28, shares of SYY declined 2.6% as the company delivered weaker-than-expected Q3 results. The company’s revenue grew 4.7% year-over-year to $20.5 billion but missed analyst estimates by a slight margin. Moreover, its adjusted EPS of $0.94 fell short of the consensus estimate by a penny. The underwhelming performance triggered a negative market reaction, as investors remained concerned about ongoing margin pressures and uncertainties surrounding the company’s pending acquisition of Restaurant Depot.

For the current fiscal year, ending in June, analysts expect SYY’s EPS to grow 2.9% year over year to $4.59. The company’s earnings surprise history is mixed. It topped the consensus estimates in three of the last four quarters, while missing on another occasion.

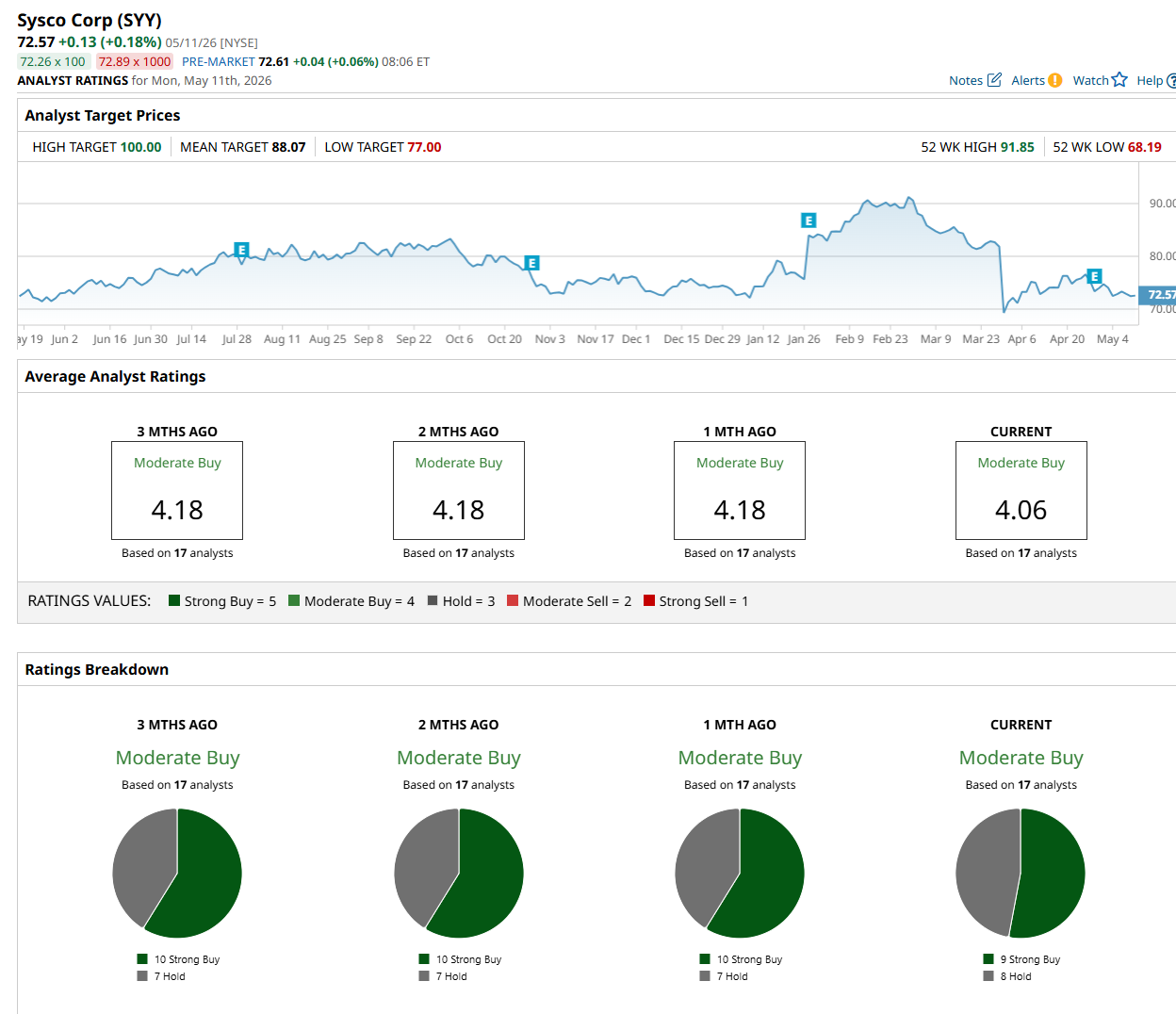

Among the 17 analysts covering the stock, the consensus rating is a "Moderate Buy,” which is based on nine “Strong Buy” and eight "Hold” ratings.

The configuration is slightly less bullish than a month ago, with 10 analysts suggesting a “Strong Buy” rating.

On May 7, Guggenheim analyst John Heinbockel reiterated a “Buy” rating on SYY and set a price target of $90, indicating a 24% potential upside from the current levels.

The mean price target of $88.07 suggests a 21.4% premium to its current price levels, while its Street-high price target of $100 implies a 37.8% potential upside.

On the date of publication, Neharika Jain did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/Ai%20chip%20by%20Quality%20Stock%20Arts%20via%20Shutterstock.jpg)

/A%20hand%20holding%20a%20phone%20with%20the%20Reddit%20logo_%20Mamun_Sheikh%20via%20Shutterstock_.jpg)

/Seagate%20sign%20on%20the%20building%20atits%20operational%20headquarters%20By%20JHVEPhoto.jpeg)

/Apple%20logo%20on%20store%20front%20by%20frantic00%20via%20iStock.jpg)