With a market cap of $12.1 billion, UDR, Inc. (UDR) is a leading multifamily real estate investment trust with more than 53 years of experience delivering long-term value through the management, acquisition, development, and redevelopment of apartment communities across targeted U.S. markets. As of March 31, 2026, the company owned or held ownership positions in 59,782 apartment homes, including 300 homes under development, while maintaining a strong commitment to shareholders, residents, and associates.

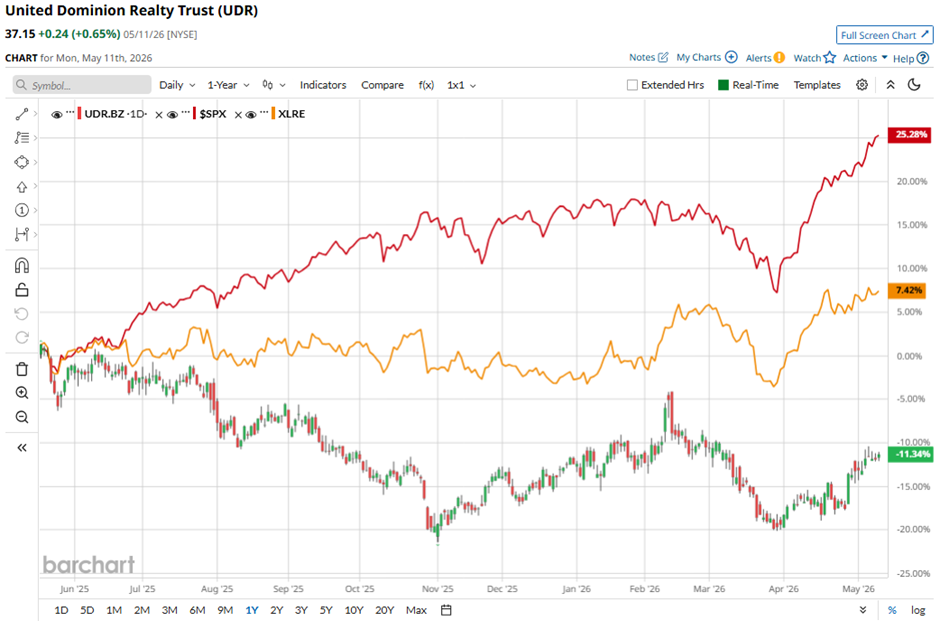

Shares of the Maryland, USA-based company have underperformed the broader market over the past 52 weeks. UDR stock has declined 12.2% over this time frame, while the broader S&P 500 Index ($SPX) has rallied nearly 31%. Moreover, shares of the company are up 1.3% on a YTD basis, compared to SPX’s 8.3% gain.

Zooming in further, shares of UDR have lagged behind the State Street Real Estate Select Sector SPDR ETF’s (XLRE) 7.2% return over the past 52 weeks.

Shares of UDR recovered marginally following its Q1 2026 results on Apr. 29 as the company reported FFO as adjusted of $0.62 per share, in line with guidance. Investor sentiment was further supported by solid operating metrics, including blended lease rate growth of 1.6%, occupancy in the mid-96% range, renewal rent growth of 5.2%, and a 300-basis-point improvement in resident retention year over year.

Sentiment also improved after UDR announced a monthly dividend, sold four apartment communities for $362 million, repurchased $150 million of shares, and guided Q2 FFOA to $0.62 per share - $0.64 per share.

For the fiscal year ending in December 2026, analysts expect UDR’s FFOA to decline marginally year-over-year to $2.53 per share. However, the company’s earnings surprise history is promising. It beat or met the consensus estimates in the last four quarters.

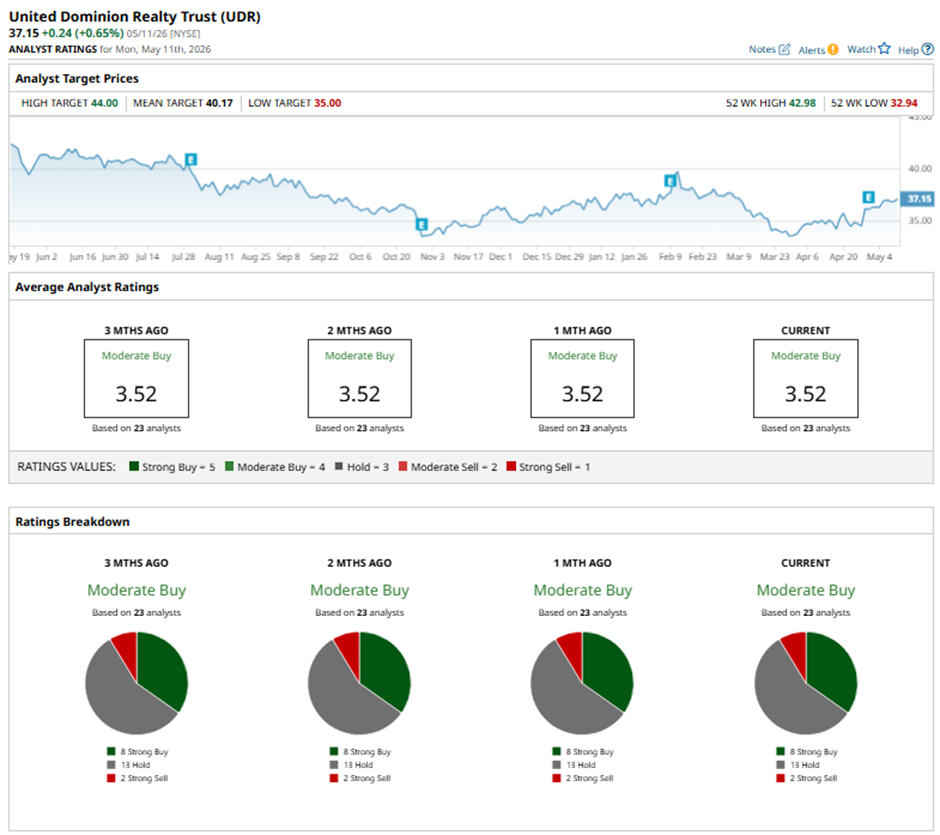

Among the 23 analysts covering the stock, the consensus rating is a “Moderate Buy.” That’s based on eight “Strong Buy” ratings, 13 “Holds,” and two “Strong Sells.”

On May 11, Barclays cut its price target on UDR to $41 while maintaining an “Overweight” rating.

The mean price target of $40.17 represents a 8.1% premium to UDR’s current price levels. The Street-high price target of $44 suggests a 18.4% potential upside.

On the date of publication, Sohini Mondal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/Ai%20chip%20by%20Quality%20Stock%20Arts%20via%20Shutterstock.jpg)

/A%20hand%20holding%20a%20phone%20with%20the%20Reddit%20logo_%20Mamun_Sheikh%20via%20Shutterstock_.jpg)

/Seagate%20sign%20on%20the%20building%20atits%20operational%20headquarters%20By%20JHVEPhoto.jpeg)

/Apple%20logo%20on%20store%20front%20by%20frantic00%20via%20iStock.jpg)