/PayPal%20Holdings%20Inc%20logo%20and%20money-by%20Sergio%20Photone%20via%20Shutterstock.jpg)

PayPal (PYPL) spent 2025 trying to convince investors that its turnaround strategy was finally gaining traction under the leadership of CEO Alex Chriss. However, the board became frustrated with the company’s slow turnaround progress, weak execution, and continued competitive struggles, ultimately removing Chriss in early 2026.

PayPal reported its first-quarter earnings on May 5. The report revealed that, while PayPal is trying to reposition itself for long-term growth under a new CEO, three major problems continue to weigh heavily on investor confidence. PYPL stock is down 22% year-to-date (YTD), trailing the overall market's gain of 8%.

Let’s take a look at these three major issues hurting the stock — and what PayPal is doing about it.

PayPal's Core Checkout Business Is Still Struggling

PayPal’s branded checkout business has always been the company’s most valuable and profitable segment. In the first quarter, online branded checkout total payment volume grew just 2% on a currency-neutral basis, owing to slow growth in Europe and challenges in the travel sector. Management also admitted that current trends indicate overall payment volume may be at the low end of its full-year projection.

PayPal appointed Enrique Lores as its new CEO in March 2026. Since taking over, Lores has pushed an aggressive turnaround strategy. The company is now investing heavily in rewards, loyalty programs, buy-now pay-later (BNPL) offerings, and improved checkout experiences in order to drive consumer engagement and defend market share. Pay with Venmo grew 34% year-over-year (YOY), while BNPL volume increased 23%.

It is fantastic news that newer payment products are outperforming the core business. However, this is concerning investors that PayPal's traditional checkout dominance will weaken as competition from digital wallets, alternative methods of payment, and emerging fintech platforms grows. Although total company payment volume grew 11% to $464 billion during the quarter, the sluggish growth in its core business may be one of the main reasons PYPL stock continues to suffer.

Profitability Is Under Pressure as Spending Rises

The second major issue is that PayPal is spending heavily just to stabilize growth. The company is increasing investments across technology, marketing, AI infrastructure, product development, loyalty programs, and organizational restructuring. These investments are putting pressure on profitability in the near term. Consequently, operating income fell 5% YOY to $1.5 billion, while adjusted EPS increased only 1% to $1.34.

Management also guided that Q2 would face even more pressure, with adjusted EPS likely to be down around 9% YOY, driven by higher investment expenses and ongoing restructuring efforts. Management believes these investments will boost long-term growth. Basically, the company is asking investors to accept weaker profit margins and slower earnings now based on future promises.

PayPal Admitted It Fell Behind Technologically

During the earnings call, Lores admitted that that PayPal suffered from “years of underinvestment” in its technology platform. The CEO now intends to speed modernization initiatives, become more cloud-native, and aggressively integrate AI into development and operations. Lores confirmed what many investors feared that PayPal lost momentum while competitors like Apple (AAPL), Visa (V) and Mastercard (MA) innovated faster. The company is now undergoing a huge transformation, which includes reorganizing the business into three divisions, streamlining decision-making, removing management layers, and implementing AI across operations. Management anticipates these efforts to result in gross savings of at least $1.5 billion over the next two to three years.

The challenge is that PayPal is attempting to modernize its infrastructure while also protecting market share, increasing user interaction, scaling Venmo, extending stablecoin projects, and restructuring internal operations. Investors fear that such large-scale transformations usually take years, which is why PYPL stock is struggling now.

What Is the Verdict on PYPL Stock?

PayPal still has enormous scale, a globally recognized brand, strong free cash flow generation, and valuable assets like Venmo and Braintree. The company generated $1.7 billion in adjusted free cash flow in Q1 and continues to return capital through buybacks, including $1.5 billion in share repurchases during the first quarter alone. Nonetheless, I believe the stock remains a “wait-and-see” story, until there is clearer evidence of sustainable growth.

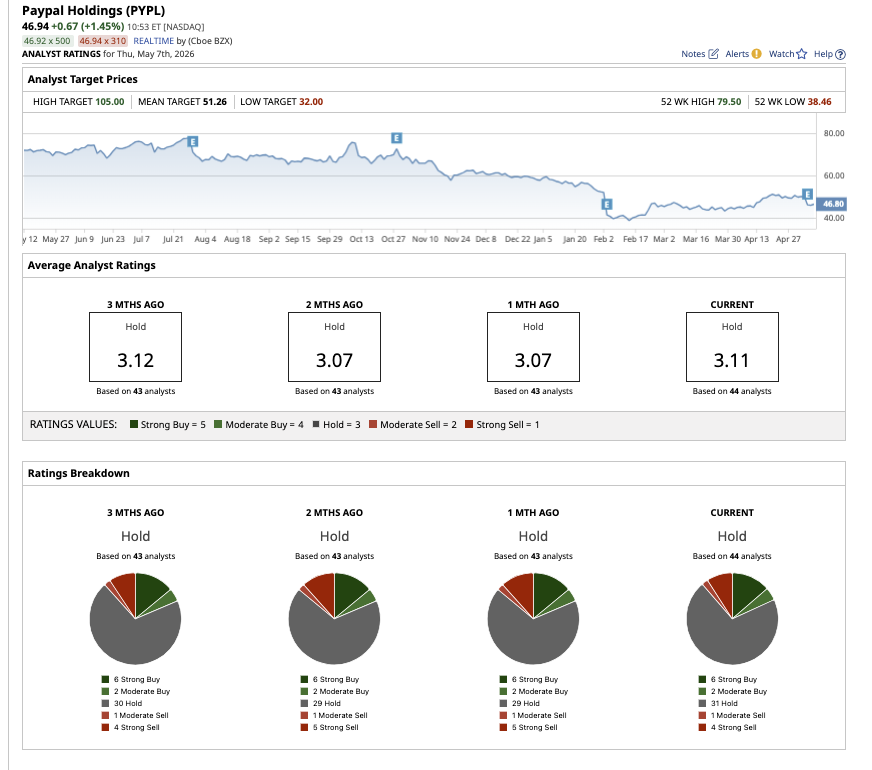

Analysts agree that it might be wise to watch PayPal from the sidelines now to see whether management’s turnaround strategy ultimately works. On the Street, PYPL stock has a consensus “Hold” rating. Of the 44 analysts covering the stock, five rate it a “Strong Buy,” two rate it a “Moderate Buy,” 32 have a "Hold" rating, one says it is a “Moderate Sell,” and four analysts have a "Strong Sell" rating. The mean target price for PYPL stock is $51.33, which implies 12% potential upside from current levels. The high target price of $105 suggests as much as 129% potential upside over the next 12 months.

On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/A%20close-up%20of%20a%20General%20Motors%20corporate%20sign%20by%20lindaparton%20via%20Adobe%20Stock.jpeg)

/Zoetis%20sign%20at%20their%20Canadian%20By%20JHVEPhoto.jpeg)