/Advanced%20Micro%20Devices%20Inc_%20logo%20on%20phone%20and%20website-by%20T_Schneider%20via%20Shutterstock.jpg)

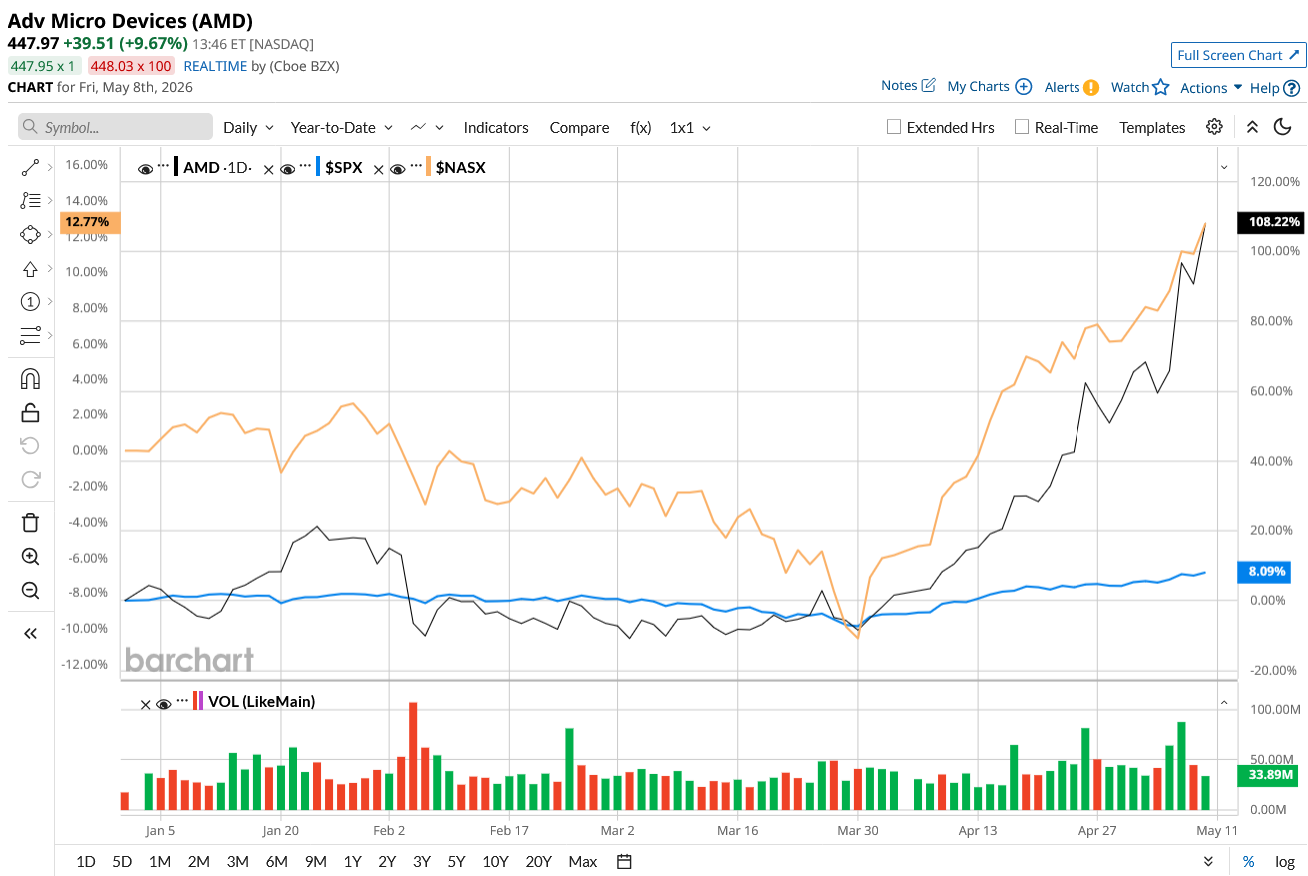

Advanced Micro Devices (AMD) shares have been on a stunning rally this year, up 108% year-to-date (YTD) as of this writing, as investors continue piling into artificial intelligence (AI) chipmakers. This rally has turned AMD into one of the market’s hottest semiconductor names again. While retail investors have been chasing the momentum higher, one of Wall Street’s most closely watched growth investors has done the opposite.

Cathie Wood has once again trimmed her position in AMD through ARK Invest (ARKK) (ARKW) funds, even as the stock trades near record highs. This move has investors wondering why Wood reduced exposure to one of the year's best-performing AI stocks.

Let’s find out why.

Cathie Wood Appears to Be Locking In Massive Gains

AMD’s rally this year has largely been driven by growing optimism around its AI accelerators, EPYC server processors, and expanding role in data centers. Furthermore, a blockbuster Q1 earnings boosted the stock higher. Yet, prior to the earnings release, Wood, through her ARK funds, sold more than 208,000 AMD shares in total across two trading sessions, totaling around $70.9 million.

One likely reason behind the selling is simple profit-taking. AMD has dramatically outperformed the broader market gain of 7% this year as enthusiasm around AI infrastructure spending has grown. Earlier this year, ARK Invest bought $1.10 million worth of AMD shares when the stock was trading around $194. It makes sense to cash in the profits when the stock rallied to around $360 on May 4.

ARK Invest is known for actively rebalancing positions after sharp rallies, especially when a stock grows too large within its portfolios. Despite the latest sales, AMD still remains one of ARK’s largest holdings across several ETFs, with a weightage of around 6%.

AMD’s AI Momentum Still Looks Strong

Wood’s decision to trim shares doesn’t necessarily mean the company is in trouble. Instead, the move could simply reflect portfolio discipline after one of the strongest semiconductor rallies in recent years.

In fact, its Q1 print revealed that its AI and data center businesses grew much faster than Wall Street anticipated. Revenue climbed 38% year-over-year (YoY) to $10.3 billion, beating the high end of management’s guidance. Meanwhile, earnings per share rose 43% to $1.37, and free cash flow more than tripled to $2.6 billion. Revenue and earnings both topped the consensus estimates. Data Center revenue, in particular, surged 57% YoY to $5.8 billion, fueled by explosive demand for EPYC server CPUs and Instinct AI GPUs. AMD’s EPYC server CPU business continues to take market share from rivals in both cloud and enterprise. Notably, revenue rose more than 50% YoY, with cloud and enterprise sales each growing over 50%.

Fueled by accelerating AI demand, AMD expects server CPU revenue to surge over 70% YoY in the second quarter, with strong growth trends likely to extend through late 2026 and into 2027. The company also significantly raised its long-term outlook, projecting the server CPU market to expand at a compound annual growth rate above 35% and surpass $120 billion by 2030.

Furthermore, AMD’s AI GPU business also appears to be strengthening. The company is expanding its partnership with Meta Platforms (META) and OpenAI and highlighted that demand for its upcoming MI450 GPUs and Helios AI platform is already exceeding internal forecasts. Management predicts that the Data Center AI business could generate “tens of billions of dollars” in annual revenue by 2027 while surpassing its long-term growth target of more than 80%.

Is AMD Stock a Buy Now?

AMD’s Q1 print shows enormous momentum across nearly every major AI infrastructure category. The only concern is valuation. After the stock’s massive rally, expectations are extremely high, which is evident in its forward price-to-earnings ratio of 55x. Analysts predict the company’s earnings to increase by 76% in 2026, followed by 75% in 2027. AI-related semiconductor stocks can become volatile when growth slows even slightly. However, for long-term investors willing to tolerate volatility, AMD looks like one of the strongest large-cap AI infrastructure plays today.

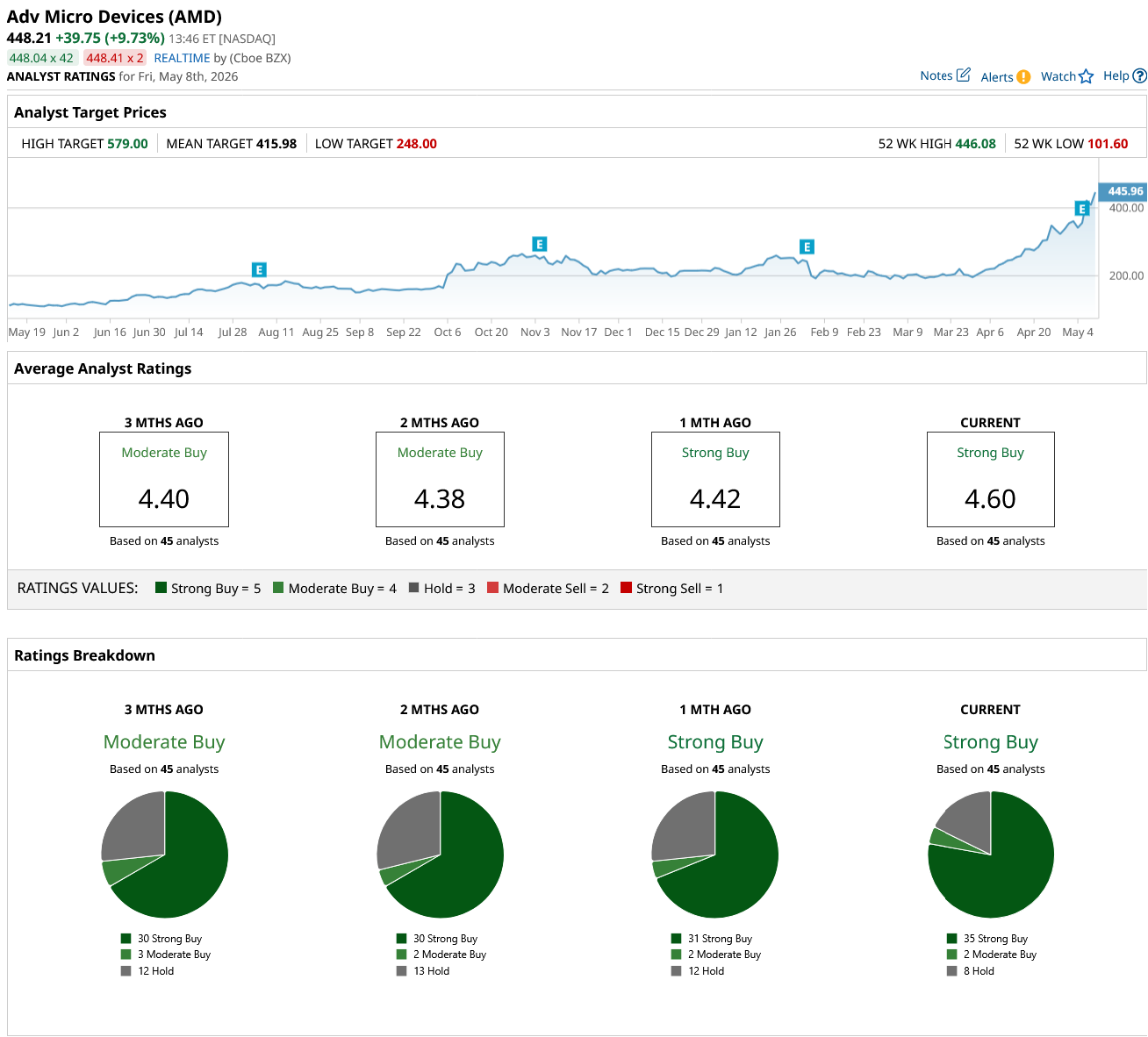

On Wall Street, AMD stock is an overall consensus “Strong Buy.” Of the 45 analysts covering the stock, 35 rate it a “Strong Buy,” two rate it as a “Moderate Buy,” and eight rate it a “Hold.” AMD stock rallied after the Q1 earnings release and is hitting fresh all-time highs today. The high price estimate of $579 suggests the stock has an upside potential of 29% over the next 12 months.

On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20corporate%20sign%20for%20SK%20Hynix%20by%20Tada%20Images%20via%20Adobe%20Stock.jpeg)

/Server%20racks%20by%20dotshock%20via%20Shutterstock.jpg)

/2d%20illustration%20of%20Cloud%20computing%20by%20Blackboard%20via%20Shutterstock.jpg)

/Alibaba%20by%20Photo%20Agency%20via%20Shutterstock.jpg)