/A%20Palantir%20sign%20displayed%20on%20an%20office%20building%20by%20Poetra_RH%20via%20Shutterstock.jpg)

Palantir is the only company that has no "AI slop.” This sounded like a bold claim from management on the earnings call, but the numbers backing it are strong. Palantir now points to a Rule of 40 score of 145% after revenue jumped 85% year-over-year (YOY), thanks in large part to the firm more than doubling its U.S. business. Now, CEO Alex Karp is guiding for 71% full‑year revenue growth, up 10 points from just a quarter ago.

That confidence is showing up outside the conference line, too. President Donald Trump recently praised Palantir while highlighting a $1.3 billion Pentagon contract tied to operations in the Middle East, putting its software closer to the center of how U.S. power is projected.

On Wall Street, Wedbush analyst Dan Ives has tagged Palantir as his favorite name outside of the “Magnificent Seven,” arguing this is where the next round of AI spending could turn into real revenue instead of slides and slogans. All of that leaves a simple question hanging in the air: Is this truly the defining “no slop” name of this cycle, or just the best-told story right now? Let's take a closer look.

Palantir's Deepening Profits and Contracts

Palantir Technologies (PLTR) is headquartered in Aventura, Florida, where it builds data and software platforms that help governments and companies make important day‑to‑day decisions. At roughly $137 per share today, PLTR stock is down 23% this year but still up 24% over the past 52 weeks.

The market is clearly paying up for the story. Palantir is worth about $319.9 billion by market capitalization and trading at a forward price-to-earnings (P/E) ratio of 128.3 times and a price‑to‑cash flow ratio of 196.8 times, far above the respective sector medians.

Palantir’s most recent earnings report, released on May 4 for the quarter ending March 2026, gives a sense of why the valuation is so rich. EPS came in at $0.25, beating the $0.22 consensus by almost 14%.

The quarter saw revenue climb 85% YOY and 16% from the prior quarter to $1.633 billion, showing that demand is not fading. Palantir showed U.S. revenue at $1.28 billion, up 104% YOY and 19% quarter-over-quarter, with U.S. commercial revenue up 133% YOY to $595 million and U.S. government revenue up 84% YOY to $687 million.

The sales engine is busy as well. The results included 206 deals worth at least $1 million, with 72 at $5 million or more and 47 at $10 million or more. This translated into a total contract value of $2.41 billion, up 61% YOY, and U.S. commercial TCV of $1.17 billion, up 45%.

That strength pushed U.S. commercial remaining deal value to $4.92 billion, more than double a year earlier and up 12% sequentially, giving some support to the idea that the growth has legs. Palantir finished the quarter with GAAP net income of $871 million at a 53% margin, operating cash flow of $899 million at a 55% margin, adjusted free cash flow of $925 million at a 57% margin, and $8 billion in cash and short‑term Treasuries on the balance sheet.

Palantir Is Expanding Mission‑Critical Partnerships

Palantir is trying to back up its “no slop” claim with deals that actually touch the real world, not just pitch decks. The partnership with GE Aerospace (GE) on U.S. military aircraft puts its software right inside critical operations. Palantir will help predict parts needed on J85 engines, cut maintenance delays, and keep training jets ready to fly under a multi‑year agreement tied directly to U.S. Air Force readiness.

That same hands‑on approach shows up in energy, where Centrus Energy (LEU) is using Palantir’s Foundry platform across a large uranium enrichment buildout, with the project already pointing to nearly $300 million in potential cost savings and helping manage risk on a $3.8 billion backlog that matters for U.S. nuclear security.

There is also the sovereign angle, which lines up with management’s push toward real production use. Palantir’s work with Nvidia (NVDA) goes beyond branding, as the two are rolling out a sovereign operating system reference design.

Outside of chips and core defense, the footprint keeps widening. A major U.S. Department of Defense contract has expanded Palantir’s role across sensitive U.S. military programs with its Maven Smart System and pushed its AI software deeper into day‑to‑day decision‑making.

A renewed five‑year agreement with Stellantis (STLA) is keeping Palantir's software inside auto plants, too. Stellantis plans to use Palantir’s Foundry platform more widely and will also start rolling out Palantir's Artificial Intelligence Platform (AIP) in select parts of its business and regions.

Taken together, these deals show a company trying to live up to the “no slop” message by plugging its platforms into mission‑critical workflows.

Palantir Stock Reads as a Street Favorite

For a stock that management keeps calling “no slop,” expectations are high. Wall Street is looking for EPS of $0.24 for the current quarter, up from $0.13 a year ago, which translates to an estimated growth rate of about 85% YOY. That is not a bar cleared by talk alone.

Michael Burry has been skeptical about Palantir for a while, yet Wedbush now argues he will be “emphatically wrong,” pointing to faster revenue growth and improving margins as the base of a longer‑term rerating case. Cathie Wood appears to share that conviction, adding roughly $11 million worth of more shares across her Ark funds and treating the name as a core holding rather than just a short‑term trade.

Morgan Stanley has also taken a constructive stance on the fundamentals, saying Palantir can keep pushing revenue higher.

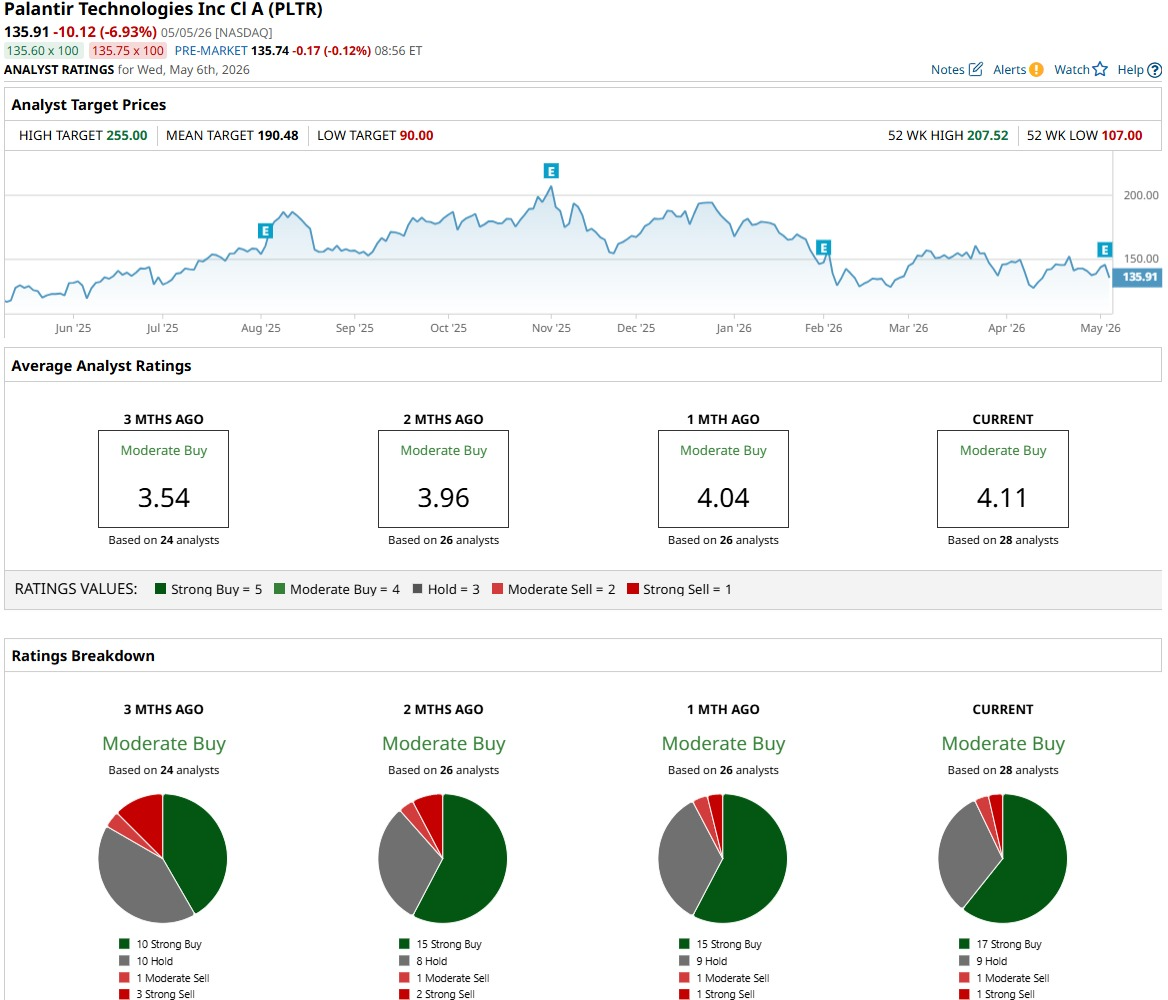

All of these views roll up into a fairly clear stance on the Street. Across 28 covering analysts, the consensus sits at a “Moderate Buy” rating. The average price target is $190.88, implying roughly 39% potential upside from current levels.

Conclusion

Palantir is starting to look less like hype and more like a company turning its “no slop” message into real contracts, steady earnings beats, and meaningful cash flow. With this kind of growth, a solid backlog, and a growing list of serious partnerships, the share price seems more likely to work higher over time than suddenly reset much lower. The move toward that $190 average price target for PLTR stock probably happens in steps rather than in one big jump, with day‑to‑day execution and the rich valuation deciding how smooth or choppy the climb turns out to be.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.