Palantir Technologies (PLTR) has been on a wild ride in 2026. Rising defense demand amid the Iran war made the stock soar barely a month ago. However, valuation concerns quickly weighed on the stock. Recently, Cathie Wood, the founder of ARK Invest, made a bold bet that put the spotlight back on Palantir. Wood, known for her high-conviction bets on disruptive innovation, has added roughly $11.15 million worth of Palantir shares to her ETFs, showing renewed confidence in one of the most debated names in the artificial intelligence (AI) space.

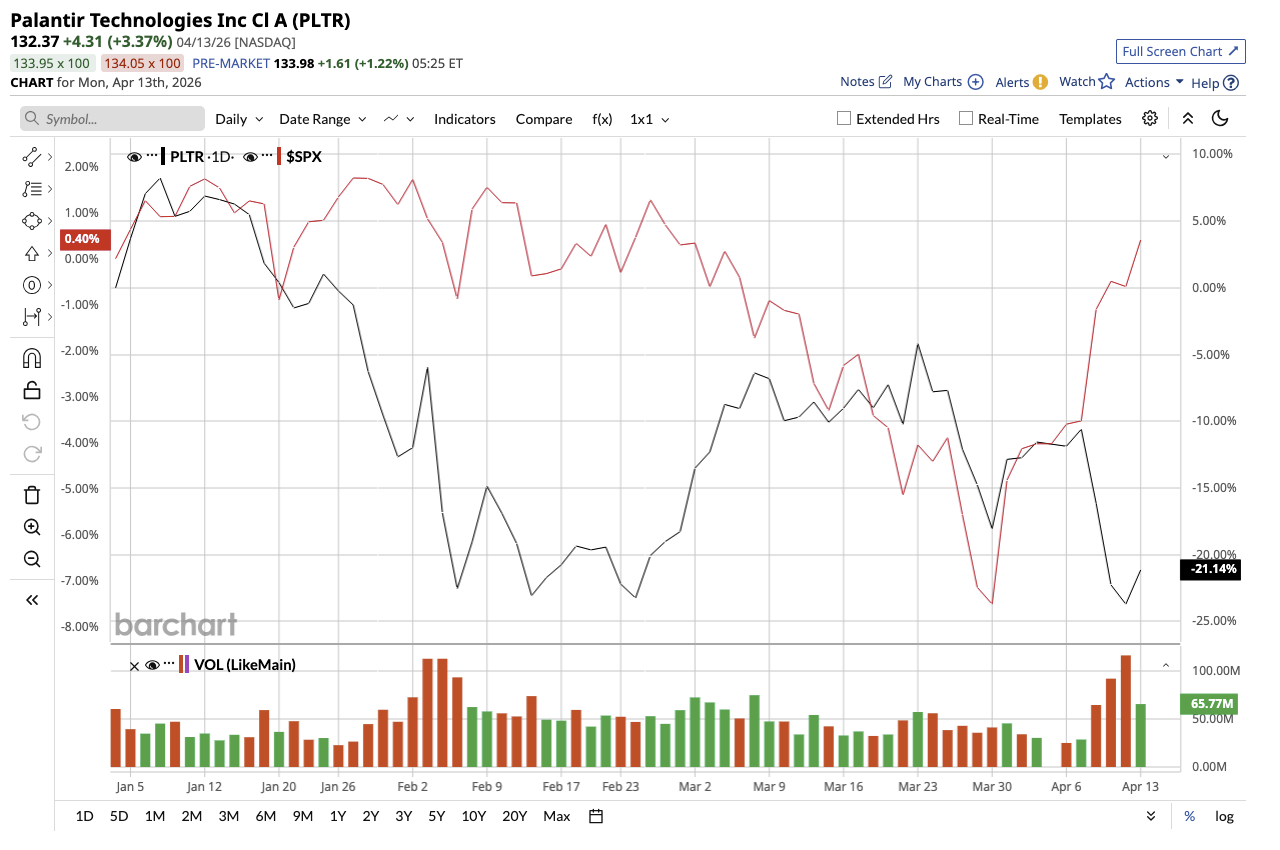

Palantir's stock is down about 23% year-to-date (YTD), yet it has still delivered a strong 47% gain over the past 52 weeks. Should investors follow Wood’s lead or stay cautious?

A Fresh $11 Million Bet Signals High Conviction

On April 11, ARK Invest’s daily trade disclosures revealed the firm purchased 85,485 shares worth $11.15 million, spread across multiple flagship ETFs, including the ARK Innovation ETF (ARKK), ARK Autonomous Technology & Robotics ETF (ARKQ), ARK Next Generation Internet ETF (ARKW), ARK Blockchain & Fintech Innovation ETF (ARKF), and ARK Space & Defense Innovation ETF (ARKX). Palantir now holds a total of 17% weightage, reflecting its position as a core holding in Wood’s disruptive-focused portfolio.

This addition aligns with her investment strategy of identifying companies that can dominate emerging technologies, particularly AI, and then increasing exposure in these stocks during periods of volatility. This move comes at a time when Palantir continues to be a controversial topic in the tech sector.

The Controversy Surrounding Palantir

Palantir has often swung between the bulls and the bears. The bull side recognizes its deep ties with government and defense agencies, as well as its successful expansion into the commercial sector, which has positioned it as a key player in enterprise AI. The bear side has often raised ethical questions about surveillance and the use of data in warfare and security and the stock’s overvaluation. Adding to this, CEO Alex Karp’s unconventional leadership style has received some criticism.

More recently, the debate intensified when President Donald Trump publicly praised Palantir’s “warfighting capabilities” in a Truth Social post, boosting sentiment around its defense role. At the same time, prominent investor Michael Burry continues to bet against the company, claiming that the stock is considerably overvalued relative to its fundamentals.

Palantir’s Performance: From Government Contractor to AI Powerhouse

Currently, PLTR stock trades at a premium of 100x forward 2026 earnings, which is expected to increase by 76.1%. Analysts expect a further increase of 40.8% in EPS in 2027. While the concerns revolve around valuation, the company’s progress over the past few years has been nothing but remarkable. Palantir ended 2025 with $4.47 billion in revenue, a 56% year-over-year (YoY) growth. Management expects a 61% increase in revenue in 2026, in line with the consensus targets.

What was more striking was the performance of its U.S. commercial segment, which expanded 137% YoY, reflecting accelerating enterprise adoption of its AI-driven platforms. Palantir's overdependence on government contracts has often been questioned. But the company has clearly solved that problem.

The Government business still remains a powerful and stable revenue driver. The segment grew 66% YoY in the U.S., supported by strong demand from defense and civil agencies. In 2025, the company secured major contracts, including a deal worth up to $448 million with the U.S. Navy to modernize supply chains and improve operational efficiency.

Palantir’s dual-engine model of high-growth commercial business alongside resilient government revenue is a balance that few software companies have. Furthermore, its hypergrowth, strong profit margins, and cash generation capabilities reduce some of the risks typically associated with high-growth tech stocks. This explains its premium valuation.

The Bottom Line: A High-Stakes Bet on the Future of AI

Cathie Wood’s $11 million bet reflects deeper confidence in Palantir’s accelerating growth trajectory and its expanding role in the AI ecosystem. As organizations across both the public and private sectors deepen their reliance on data-driven decisions, platforms like Palantir’s could become indispensable.

However, the stock remains a battleground for bulls and bears. PLTR stock is down 34% from its 52-week high of $207.52. Investors who share Wood's trust in Palantir and are ready to deal with volatility may find the current sell-off in this controversial stock appealing.

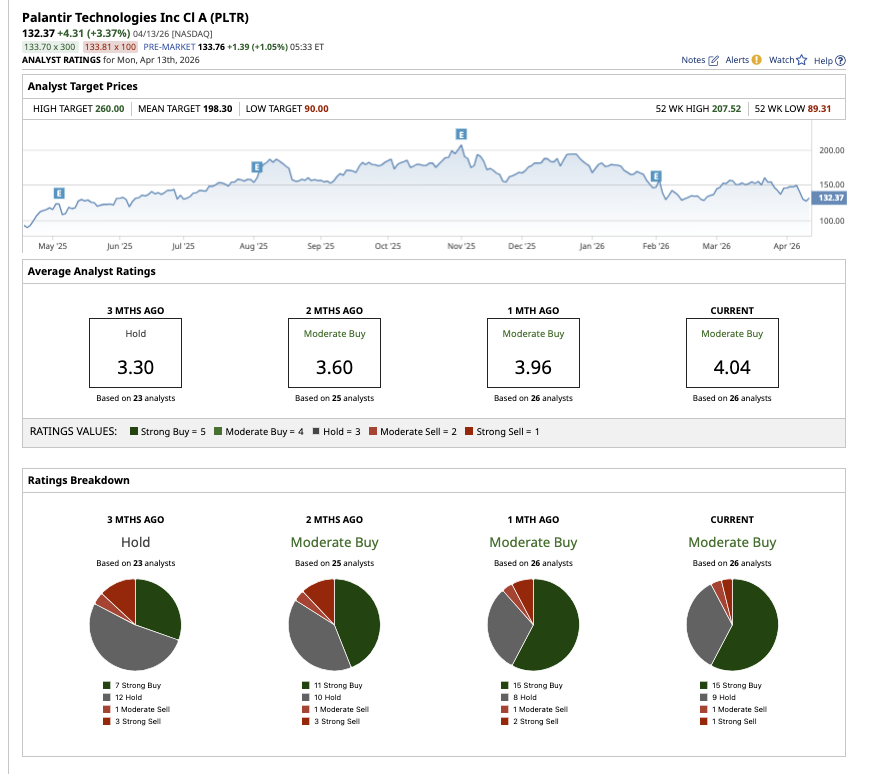

Overall, PLTR stock is a “Moderate Buy” on Wall Street. Of the 26 analysts covering PLTR stock, 15 rate it as a “Strong Buy,” nine have a “Hold” rating, one analyst has a “Moderate Sell” rating, and one analyst has a “Strong Sell” rating. Based on the average price target of $198.30, analysts see the stock climbing 50% from current levels. The high price estimate of $260 suggests potential upside of 96% from here.

On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/Data%20Center%20by%20Caureem%20via%20Shutterstock%20(2).jpg)

/A%20corporate%20sign%20for%20SK%20Hynix%20by%20Tada%20Images%20via%20Adobe%20Stock.jpeg)