/Nvidia%20logo%20and%20sign%20on%20headquarters%20by%20Michael%20Vi%20via%20Shutterstock.jpg)

Backed by the artificial intelligence (AI) boom, Nvidia (NVDA) became the first company to cross the $5 trillion market valuation threshold in October 2025. In the following months, NVDA stock has witnessed some correction and sideways movement. However, shares of the tech giant have still returned 53% in the last 52 weeks.

As positive new flows continue for Nvidia, the stock might be poised for another breakout after consolidation. Last week, Nvidia and Palantir (PLTR) announced a partnership on sovereign AI operating systems. This is an important collaboration, as the sovereign AI architecture will allow enterprises to completely control data, AI models, and applications.

The architecture is therefore important for customers with existing GPU infrastructure, latency-sensitive workflows, data sovereignty requirements, and geographical distribution. This can unlock significant revenue potential from governments and multiple industries. The partnership therefore adds to the positive catalysts for NVDA stock for the medium to long term.

About Nvidia Stock

Headquartered in Santa Clara, California, Nvidia identifies itself as a global leader in AI and accelerated computing. The company’s data center-scale infrastructure and computing platform is used by major cloud service providers, AI model makers, and enterprises for the acceleration of services and offerings.

Nvidia has two business segments: Compute & Networking and Graphics. For fiscal 2026, the company reported revenue of $215.9 billion, which was higher by 65% on a year-over-year (YOY) basis. This growth was backed by robust compute demand that’s likely to sustain with growth in agentic AI.

It’s worth noting that innovation is the core strength for Nvidia. Since inception, according to the company in a Form 10-K, Nvidia has invested $76.7 billion in research & development. This has given the firm an edge and is likely to ensure steady value creation.

Amid all the positives, NVDA stock has remained relatively sideways year-to-date (YTD), although shares are up 7% in the last six months. This seems like a good accumulation opportunity for investors, with data-center investment expected to touch $6.7 trillion by 2030.

Strong Moat Implies Robust Growth Potential

Starting from Nvidia’s CUDA development platform to its Blackwell architecture, the company has created a sustained industry advantage. This is reflected in Nvidia's growth momentum and gross margins. To put things into perspective, according to CFO Colette Kress, Nvidia’s data-center revenue has increased by 13 times since the emergence of ChatGPT.

It’s also worth noting that Nvidia is undertaking another product transition with Vera Rubin architecture. Last week, Microsoft (MSFT) announced that it is the first cloud service provider to start validating the Vera Rubin NVL72 system. Accelerated computing infrastructure may be the next growth driver.

For fiscal 2026, Nvidia reported revenue of $215.9 billion with a robust gross margin of 71.1%. For the same period, operating cash flow was $102.7 billion. Robust cash flows provide flexibility for investment in innovation. At the same time, there is ample headroom for value creation through dividends and aggressive share repurchases.

What Do Analysts Say About NVDA Stock?

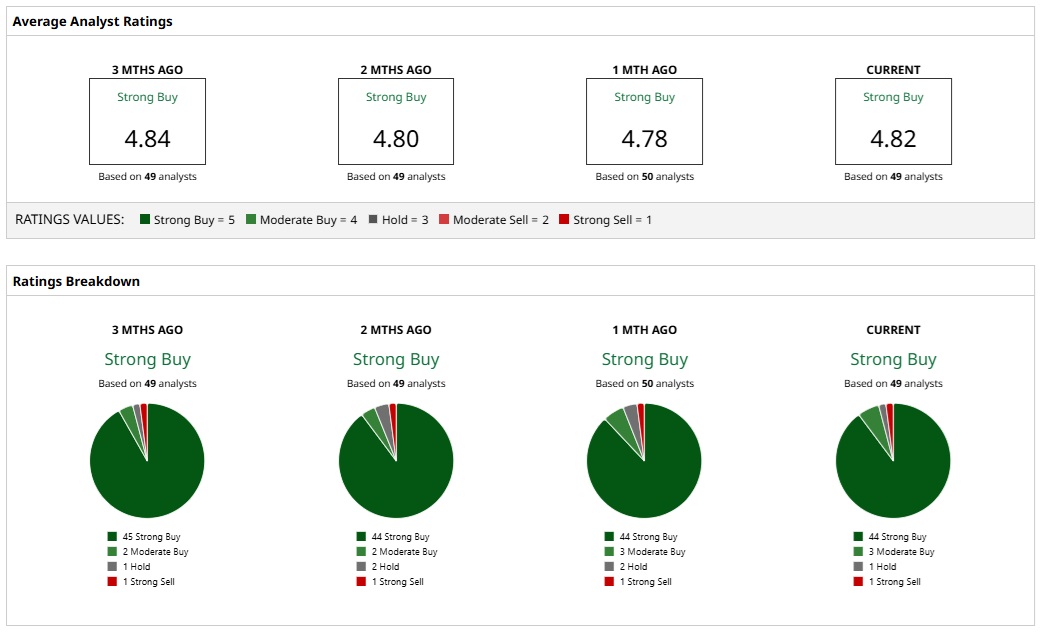

Based on 49 analysts with coverage, NVDA stock is a consensus “Strong Buy.” An overwhelming majority of 44 analysts have a “Strong Buy” rating for Nvidia, while three analysts have a “Moderate Buy” rating and one has a “Hold” rating. On the bearish side, one analyst believes that NVDA stock is a “Strong Sell.”

Analysts have a mean price target of $265.76, implying about 46% potential upside from here. Further, the most bullish price target of $360 suggests that NVDA could rise as much as 97% from current levels.

In the immediate term, Nvidia's GPU Technology Conference (GTC) this week could be a potential catalyst for stock upside. Details on the company’s agentic-optimized CPUs and co-packaged optic switch are likely to be key positives.

The bullish view on NVDA stock is also reaffirmed from a valuation perspective. The forward price-to-earnings (P/E) ratio of 23.9 times and P/E-to-growth (PEG) ratio of 0.61 point to an attractive valuation.

On the date of publication, Faisal Humayun Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/An%20aerial%20view%20of%20a%20data%20center%20cooling%20system%20by%20Sepia100%20via%20Adobe%20Stock.jpeg)