/Visa%20Inc%20HQ%20photo-by%20Michael%20Vi%20via%20Shutterstock.jpg)

San Francisco, California-based Visa Inc. (V) is a payment technology company that operates one of the world's most extensive processing networks that facilitates commerce across more than 200 countries and territories. Valued at a market cap of $578.7 billion, the company provides a comprehensive suite of payment solutions, including credit, debit, and prepaid products, alongside commercial payment solutions and global ATM access.

This payment technology company has considerably underperformed the broader market over the past 52 weeks. Shares of V have declined 8.2% over this time frame, while the broader S&P 500 Index ($SPX) has gained 28.5%. Moreover, on a YTD basis, the stock is down 8.4%, compared to SPX’s 7.6% rise.

However, looking closer, V has outpaced the Amplify Digital Payments ETF’s (IPAY) 12.3% drop over the past 52 weeks and 9.7% loss on a YTD basis.

Visa delivered stronger-than-expected Q2 earnings results on Apr. 28, and its shares surged 8.3% in the subsequent trading session. Robust momentum across consumer and commercial payments, as well as money movement solutions, led to a 17.1% year-over-year increase in its revenue to $11.2 billion, topping analyst expectations by 5.1%. Moreover, its adjusted EPS of $3.31 exceeded consensus estimates of $3.09.

For the current fiscal year, ending in September, analysts expect V’s EPS to grow 13.9% year over year to $13.06. The company’s earnings surprise history is promising. It topped the consensus estimates in each of the last four quarters.

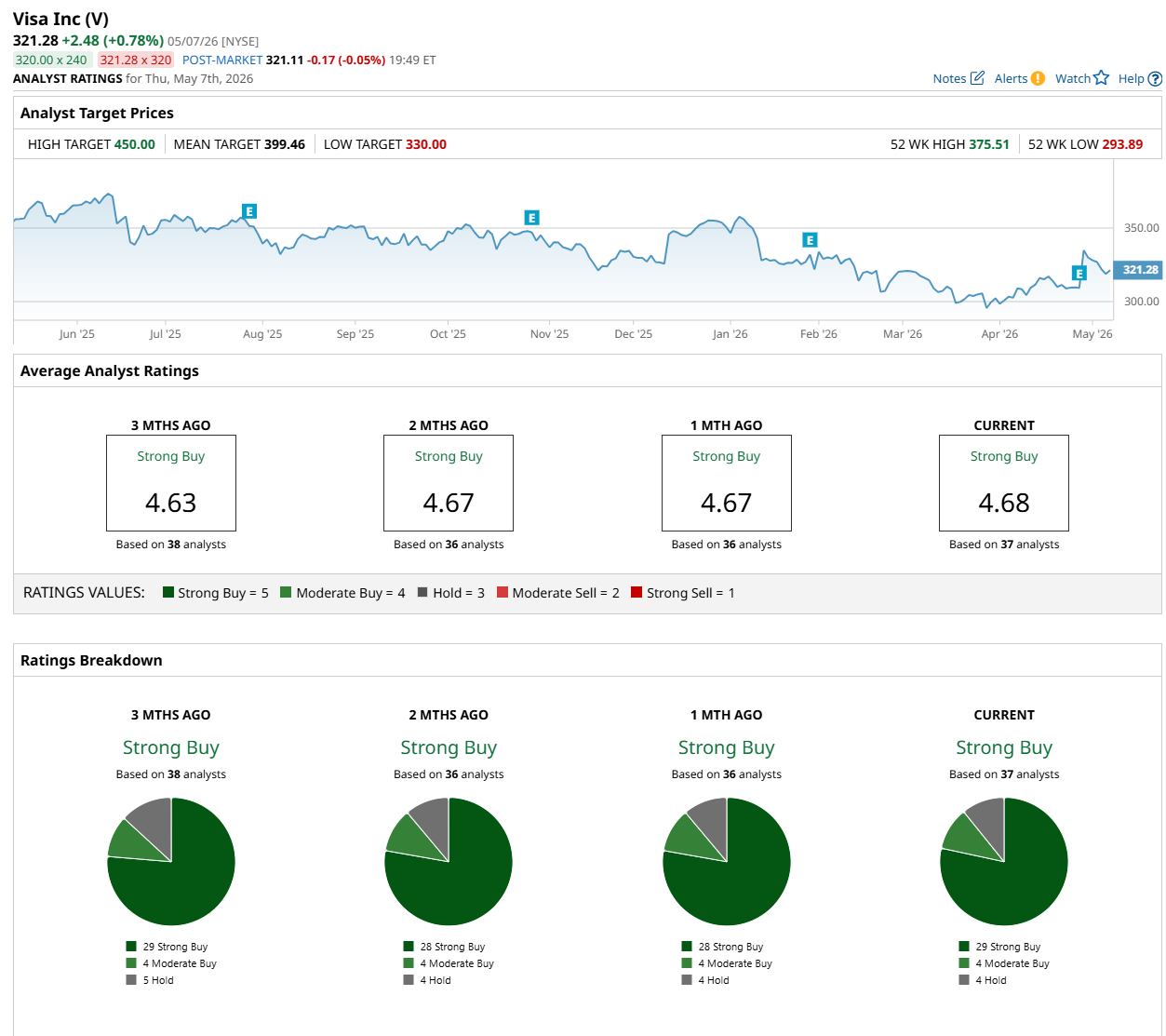

Among the 37 analysts covering the stock, the consensus rating is a "Strong Buy,” which is based on 29 “Strong Buy,” four “Moderate Buy,” and four "Hold” ratings.

The configuration is slightly more bullish than a month ago, with 28 analysts suggesting a "Strong Buy” rating.

On Apr. 30, Argus Research analyst maintained a “Buy” rating on Visa and set a price target of $396, indicating a 23.3% potential upside from the current levels.

The mean price target of $399.46 suggests a 24.3% premium to its current levels, while its Street-high price target of $450 implies a 40.1% potential upside from the current price levels.

On the date of publication, Neharika Jain did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Oracle%20Corp_%20office%20logo-by%20Mesut%20Dogan%20via%20iStock.jpg)

/Uber%20Technologies%20Inc%20logo%20outside%20offices-by%20Sundry%20Photography%20via%20iStock.jpg)

/NVIDIA%20Corp%20logo%20outside%20building-by%20BING-JHEN_HONG%20via%20iStock.jpg)

/Space%20Technology%20by%20Rini_%20com%20via%20Shutterstock.jpg)