Duke Energy Corporation (DUK) is one of the largest electric power and energy holding companies in the United States, providing electricity and natural gas services to millions of residential, commercial, and industrial customers. Headquartered in Charlotte, North Carolina, the company operates regulated utilities primarily across the Southeast and Midwest regions of the U.S. Valued at $99.3 billion by market cap, the company also invests in pipeline transmission, renewable natural gas initiatives and storage infrastructure.

Shares of this leading energy company have underperformed the broader market over the past year. DUK has gained 2.1% over this time frame, while the broader S&P 500 Index ($SPX) has rallied nearly 31.4%. Moreover, in 2026, DUK stock is up 7.1%, slightly trailing SPX’s 7.6% YTD gain.

Narrowing the focus, DUK has also trailed the State Street Utilities Select Sector SPDR Fund’s (XLU) 13.5% surge over the past 52 weeks.

On May 5, DUK shares rose marginally after the company announced its first-quarter earnings. Adjusted EPS increased 9.7% year over year to $1.93, supported by higher electric rates, customer growth, and rising power demand from data centers and commercial customers. Meanwhile, total operating revenue climbed 11.3% annually to $9.18 billion, as strength in the electric utilities business more than offset the impact of milder weather conditions.

For the current fiscal year, ending in December 2026, analysts expect DUK’s EPS to grow 6.2% to $6.70 on a diluted basis. The company’s earnings surprise history is mixed. It beat the consensus estimate in three of the last four quarters, while missing on another occasion.

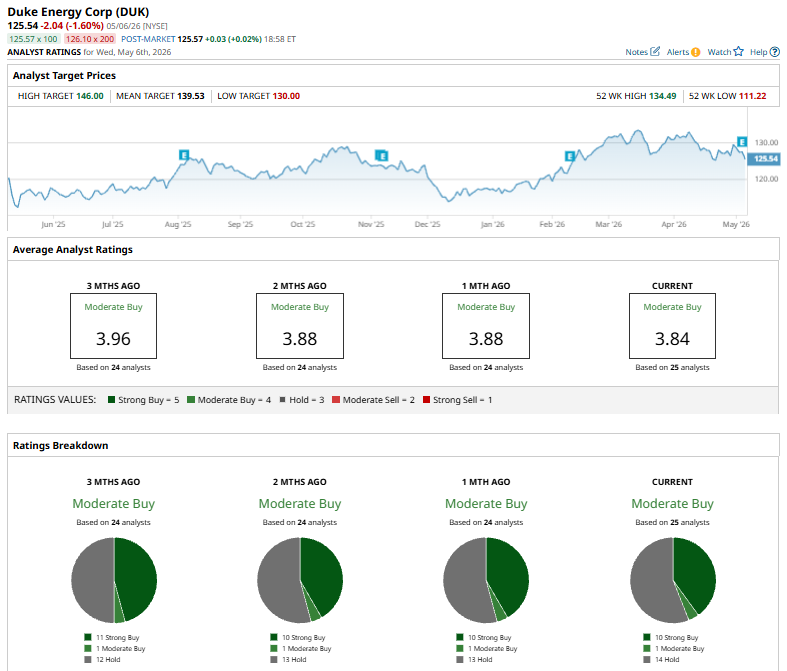

Among the 25 analysts covering DUK stock, the consensus is a “Moderate Buy.” That’s based on 10 “Strong Buy” ratings, one “Moderate Buy,” and 14 “Holds.”

This configuration is less bullish than three months ago, with 11 analysts suggesting a “Strong Buy.”

On Apr. 21, Morgan Stanley slightly lowered its price target on Duke Energy to $141 from $142 while maintaining an “Overweight” rating on the stock. The firm updated its outlook for North American regulated utilities and independent power producers, noting that utility stocks outperformed the broader market in March.

The mean price target of $139.53 represents an 11.1% premium to DUK’s current price levels. The Street-high price target of $146 suggests an upside potential of 16.3%.

On the date of publication, Kritika Sarmah did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Oracle%20Corp_%20office%20logo-by%20Mesut%20Dogan%20via%20iStock.jpg)

/Uber%20Technologies%20Inc%20logo%20outside%20offices-by%20Sundry%20Photography%20via%20iStock.jpg)

/NVIDIA%20Corp%20logo%20outside%20building-by%20BING-JHEN_HONG%20via%20iStock.jpg)

/Space%20Technology%20by%20Rini_%20com%20via%20Shutterstock.jpg)