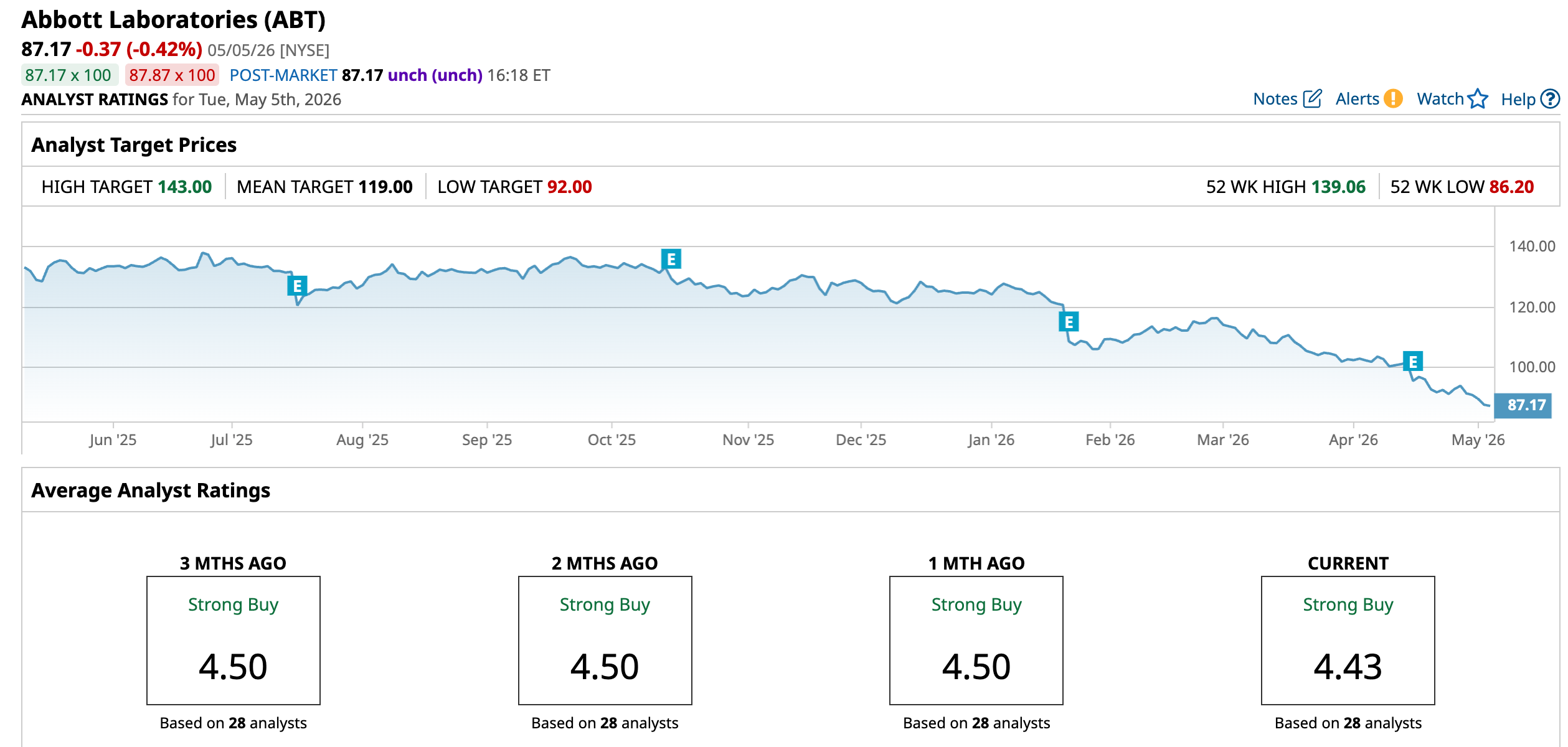

The S&P 500 Health Care sector ($SRHC) has been one of the weakest spots in the market in 2026, and Abbott Laboratories (ABT) has taken an even harder hit. As of May 4, 2026, Abbott shares closed at a new 52-week low of $87.54, down roughly 37.1% from the 52-week high of $139.06 set in June 2025. In just the last three months, ABT has dropped 19.85%.

That slide looks especially striking for a company generating $44.3 billion in annual revenue and reporting Q1 2026 sales of $11.16 billion, up 7.8% from a year earlier. Abbott also holds the rare status of being both a Dividend Aristocrat and a Dividend King, meaning it has raised its dividend for at least 50 straight years. Abbott’s most recent quarterly payout was $0.63 per share, which works out to a 2.73% yield, more than double the S&P 500’s ($SPX) 1.1% average.

So when a stock with that kind of record is trading near multi-year lows, sharp investors tend to take notice. Last week, several Abbott insiders did just that, buying shares in the open market while many others were still selling. Do these insiders see something the market is missing?

Breaking Down the Financial Picture

Abbott runs a broad healthcare business, selling medical devices, diagnostics, nutrition products, and branded generic drugs, so it touches both steady, everyday demand and faster-growing niches.

Even with that setup, the stock has been hit hard, falling 33.95% over the past year and 30.10% year-to-date (YTD).

Right now, Abbott trades at a forward P/E of 16.33 times, a bit below the sector average of 17.37 times, so the market is not giving it a big premium.

On the income side, the stock yields 2.74%, above the healthcare sector’s 1.58% average. The latest quarterly dividend was $0.63 per share, paid on April 15, 2026, and the forward payout ratio sits at 45.67%. Abbott pays dividends quarterly and has raised its payout for 55 straight years, which is exactly what income-focused investors like to see from a blue-chip name.

The business itself is still growing. In Q1 2026, Abbott reported revenue of $11.16 billion, beating the $11.03 billion analysts were looking for and rising 7.8% from a year earlier. Adjusted EPS came in at $1.15, matching expectations. The weak spot was profitability: operating margin fell to 12% from 16.3% a year ago, so more of that growth is getting eaten up by costs.

Management also nudged full-year adjusted EPS guidance down to $5.48 at the midpoint, but still expects 2026 comparable sales to grow 6.5% to 7.5%, with adjusted EPS between $5.38 and $5.58, including about $0.20 of dilution from the Exact Sciences deal.

The Growth Engines Still Powering the Story

Abbott just received FDA clearance and a CE Mark for its new Ultreon 3.0 coronary imaging platform, software that uses AI and optical coherence tomography to guide heart procedures in real time. It reads the type of plaque causing a blockage, helps doctors pick the right stent size and spot, and ties everything into one workflow so procedures can be faster and more accurate.

At the same time, Abbott is pushing deeper into precision oncology. Through its integration with Flatiron Health’s OncoEMR system, community oncologists can order Abbott tests like Oncotype DX Breast Recurrence Score, OncoExTra, Oncodetect, and Riskguard directly inside their existing records, track orders, and see results in one place. That setup taps into more than 1,600 community cancer centers and 4,700 providers, putting Abbott’s diagnostics right where most cancer care actually happens.

The Exact Sciences acquisition takes this even further. With Exact now a wholly owned subsidiary as of March 20, 2026, Abbott has stepped straight into the fast-growing cancer screening and diagnostics market, boosting its scale and giving it a larger set of tools to reach millions more patients.

Analysts See Room for Recovery

For the current quarter ending June 2026, the average earnings estimate is $1.28, slightly above $1.26 a year ago, which works out to about 1.59% growth. For the September 2026 quarter, the consensus moves up to $1.43 from $1.30 last year, a stronger 10.00% year-over-year (YOY) increase. For the full year, analysts expect EPS of $5.48 for 2026 versus $5.15 in 2025, a gain of 6.41%.

Wells Fargo’s Larry Biegelsen has kept his “Overweight” rating on Abbott, even after cutting his price target to $122, which is still well above where the stock trades now. BTIG’s Marie Thibault is even more bullish, reaffirming a “Strong Buy” and a $131 target as of April 27, treating the recent drop as a better entry point, not a sign that the business is falling apart.

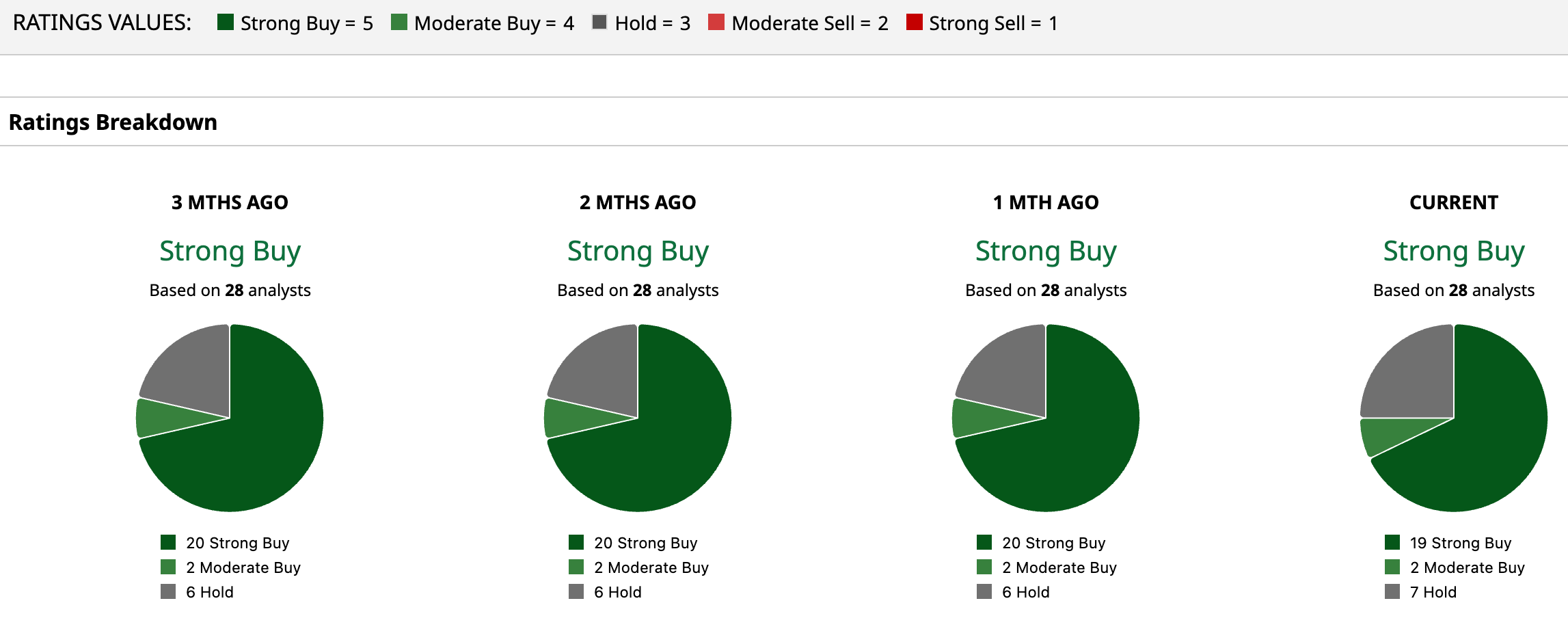

Looking at the group as a whole, 28 analysts surveyed currently rate Abbott a consensus “Strong Buy”, with an average target price of $119. Based on recent trading levels, that points to roughly 36.5% upside from here.

Conclusion

Overall, Abbott’s selloff seems more tied to sentiment than to a collapse in the underlying business. The stock is down hard, but the combination of insider buying, still-positive earnings growth estimates, a 55-year dividend growth streak, and Wall Street targets that still point materially higher suggests the shares are more likely to stabilize and recover than keep spiraling lower, especially if management delivers steady execution over the next couple of quarters. That does not mean the rebound will be immediate, but from these levels, the path of least resistance looks more up than down.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/AI%20technology%20concept%20by%20NMStudio789%20via%20Shutterstock.jpg)