/Code%20on%20computer%20screen%20java%20html%20by%20Pexels%20via%20Pixabay.jpg)

In macro market analysis, there are milestones that act as flashing yellow lights. We just hit one.

New data shows that U.S. business investment in computers and related equipment officially surged past the peak of the 1990s dot-com boom. As a percentage of GDP, we are now entering a zone that many veteran investors thought we would never see again. This surge isn’t just a trend. It is a capital migration for the ages.

And while there are no certainties about these types of trends, I’m willing to say that it ends very badly. I just don’t know when. Many investors thought the stock market was “toast” by late 1996, when then-Federal Reserve Chair Alan Greenspan characterized the economy as “irrational exuberance.” The stock market didn’t peak until early 2000.

Back in 1999, the spending was about the “pipes.” Those fiber optic cables and the basic servers required to stand up the early internet. Today, the capital is flowing into the “brains.” Those are the high-end GPUs, specialized AI chips, and massive liquid-cooled data centers required to run large language models (LLMs).

We have lapped the dot-com peak because the ante, so to speak (or front end load if you remember those days in the mutual fund business) for this new era is exponentially higher than it was for the world wide web. When a tech giant commits to a multibillion-dollar build-out, they aren’t just buying hardware. They are building a full-fledged digital system.

Something About This Massive Spend on Compute Does Not Compute

This level of investment creates a massive risk. In the late 1990s, the mantra was build it and they will come. As I like to say about a lot of things in investing, it worked… until it didn’t. Eventually, the lack of immediate return on investment (ROI) led to a violent hardware hangover. And that is the same type of risk we face today.

We also have a market where a tiny handful of stocks account for nearly half of the S&P 500 Index’s ($SPAA) total weight. And they are nearly all directly tied to historic, AI-motivated computer spending. Will profits follow on a broad basis? Hopefully, if you are a permabull.

So, how do we handle a market that just broke a 25-year investment record? I think we start by looking at the less-heralded utility sector’s presence in the AI story. You can’t run a record amount of computer equipment without a record amount of electricity.

If the specialized chips become overvalued, the smart money often rotates to the center of the trade. Namely, the power grid, cooling systems, and electrical infrastructure. Not the Anthropic IPO.

In any long-term cycle, the players that spend the most money the fastest are the ones most vulnerable to hitting the proverbial wall. It concerns me deeply that mega-cap companies that have had gobs of cash flow are now seeing it dwindle in order to ante up more and more for the AI mission. I readily admit, I’m a technician, not a fundamental investor. But even for me, something’s just not right here.

And even if it turns out to be successful, that doesn’t mean it doesn’t carry massive risk of underperforming expectations. When the stuff hit the fan in 2000, it opened the floodgates for three straight down years in the global stock market.

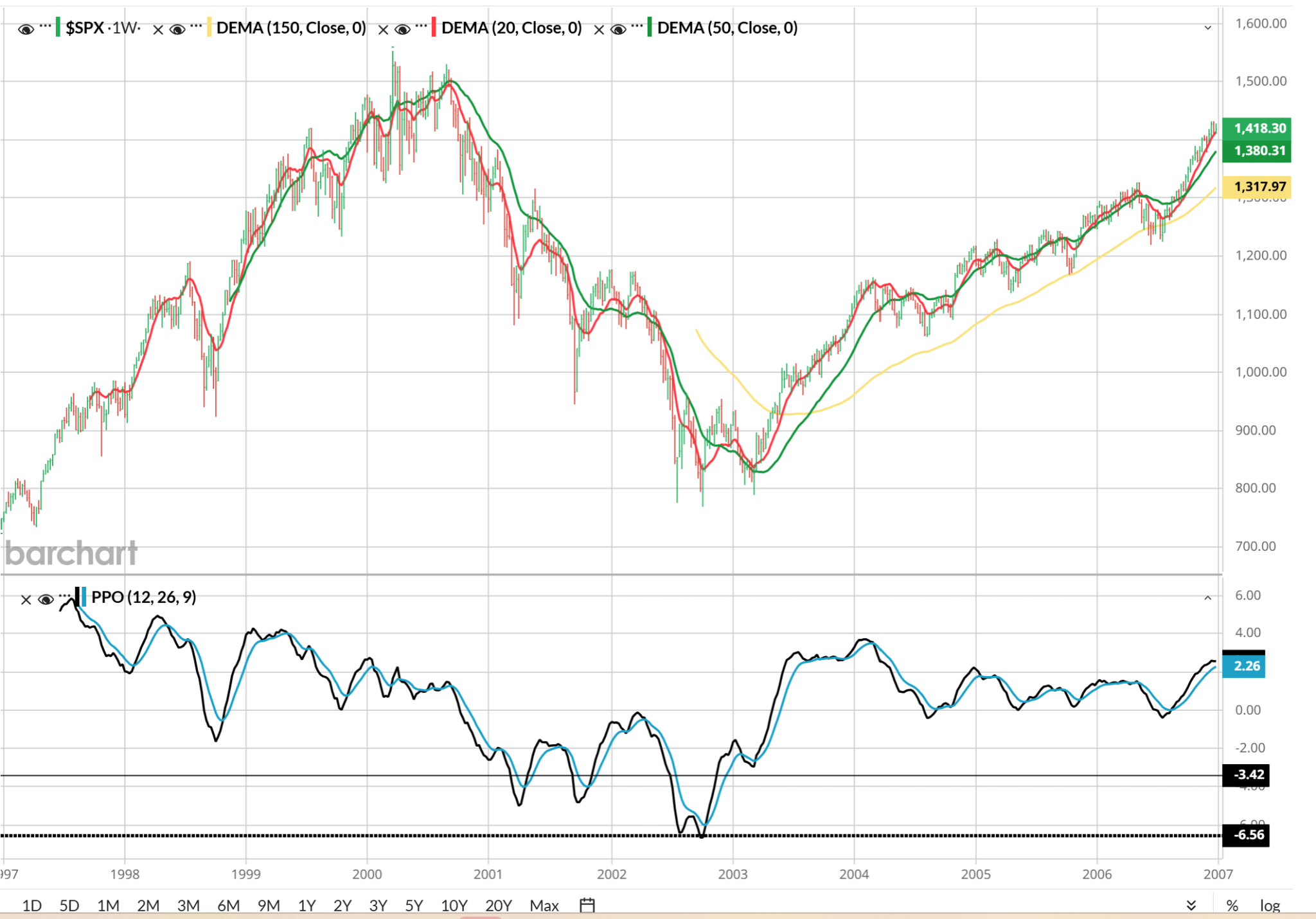

This was the S&P 500 Index from the end of 1996 through the end of 2006. 10 years that worked out OK, as long as you didn’t buy too close to the ultimate top. And even if you started when this graph does, in early 1997, as of six years later, you were just breaking even.

That was back when the world was bracing for something called Y2K.

Today, I think we should be bracing for anything less than meeting lofty expectations in terms of return on this historically high investment. Because there’s nothing Wall Street panics about more than not matching expectations. Look no further than some recent corporate earnings reports to see what happens to a single stock when it “misses.” What happens if the whole AI trade “misses?”

Rob Isbitts created the ROAR Score, based on his 40+ years of technical analysis experience. ROAR helps DIY investors manage risk and create their own portfolios. For Rob’s written research, check out ETFYourself.com.

On the date of publication, Rob Isbitts did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/An%20aerial%20view%20of%20a%20data%20center%20cooling%20system%20by%20Sepia100%20via%20Adobe%20Stock.jpeg)