Valued at $71.5 billion by market cap, Apollo Global Management, Inc. (APO) is a leading alternative investment manager that operates at the intersection of private markets and institutional capital. The New York-based company specializes in deploying capital across private equity, credit, and real assets, with a strong emphasis on generating long-term, risk-adjusted returns.

Apollo Asset Management has struggled to keep pace with the broader market. APO stock has plunged 11.1% over the past 52 weeks and dipped 15.5% in 2026, compared to the S&P 500 Index’s ($SPX) 28.3% surge and 4.2% rally, respectively.

The underperformance extends to its sector peers as well, with Apollo trailing the iShares U.S. Financials ETF (IYF), which has gained 11.4% over the past year and is down 4.5% in this year.

Apollo Global Management has lagged the broader market over the past year primarily due to pressure on alternative asset managers from macro and cycle dynamics. Elevated interest rates and tighter financial conditions have slowed deal activity and exit volumes, limiting performance fee (carry) realization, an important driver of upside earnings. At the same time, mark-to-market volatility in credit and private assets has weighed on investor sentiment toward the sector. Additionally, Apollo’s credit-heavy, insurance-linked model, while structurally resilient, has faced scrutiny over spread sustainability and the pace of capital deployment in a shifting rate environment.

For FY2026, which ends in December, analysts expect Apollo Global Management to deliver adjusted EPS of $8.44, representing a 14.5% year-over-year increase. However, the firm's track record of meeting expectations has been inconsistent. It has missed the Street's earnings estimates twice over the past four quarters and exceeded them twice.

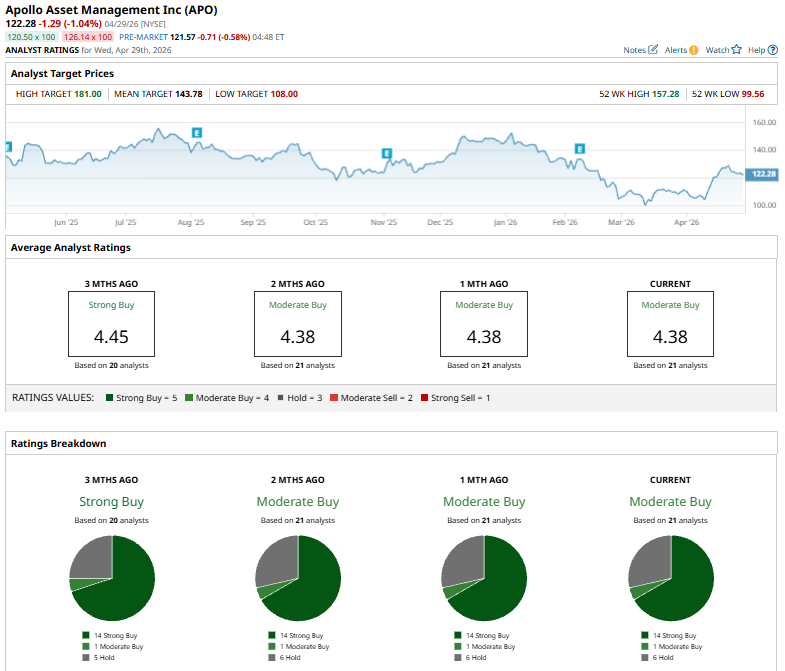

Analysts remain very optimistic about the stock’s long-term prospects. APO holds a consensus “Moderate Buy” rating overall. Of the 21 analysts covering the stock, opinions include 14 “Strong Buys,” one “Moderate Buy,” and six “Holds.”

The overall rating is bearish than three months ago, when the stock had three “Strong Buy” suggestions.

Apr. 21, Michael Cyprys of Morgan Stanley lowered his price target on Apollo Global Management to $165 from $181 while maintaining an “Overweight” rating. Ahead of Q1 results, he cut EPS estimates by about 9% but still expects the firm to come in slightly above consensus across its alternative asset manager coverage.

APO’s mean price target of $143.78 indicates a 17.6% premium to current price levels.

On the date of publication, Kritika Sarmah did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Microsoft%20headquarters%20By%20Peter.jpeg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/NVIDIA%20Corp%20logo%20outside%20building-by%20BING-JHEN_HONG%20via%20iStock.jpg)

/Amazon%20-%20Image%20by%20bluestork%20via%20Shutterstock.jpg)