/Micron%20Technology%20Inc_billboard-by%20Poetra_RH%20via%20Shutterstock.jpg)

Leading memory chipmaker Micron Technology (MU) has had a stellar run on Wall Street over the past year, as the company faces a strong demand for the memory chips it makes. These chips are the backbone component of consumer electronics devices such as smartphones and laptops. Moreover, memory chips have become important for artificial intelligence (AI) data centers and the servers installed in these facilities, which has skyrocketed demand for them.

The “big three” of memory chips, Micron, Samsung, and SK Hynix, faced this growing demand (culminating in a shortage) and rising memory prices. In particular, there is a huge demand for high-bandwidth memory (HBM).

This memory crunch is proving to be long-lasting, as technology companies are set to spend roughly $650 billion on computing infrastructure in 2026. Synopsys (SNPS) CEO Sassine Ghazi expects the chip crunch to last through this year and the next because products that need memory chips are being “starved” as they are directed toward AI infrastructure.

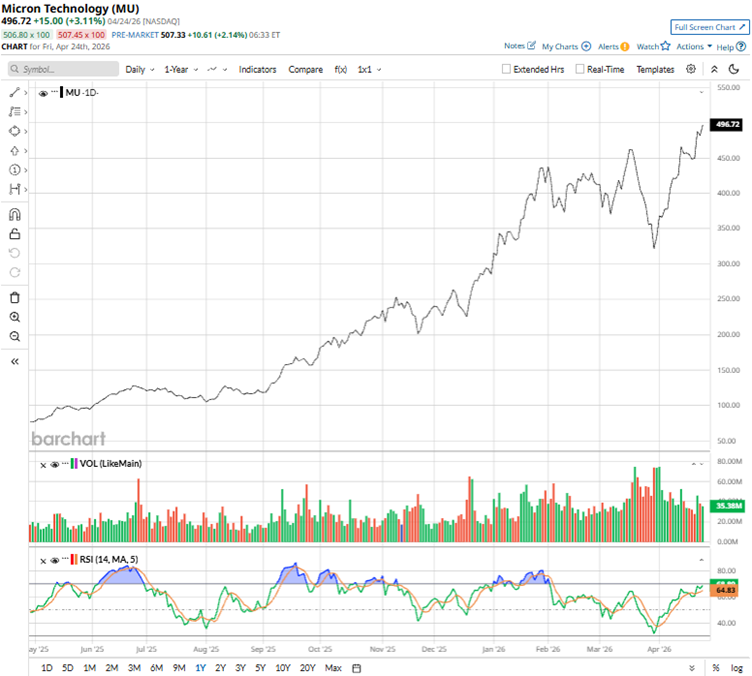

Against this backdrop, Micron’s stock has gained a whopping 557.1% over the past 52 weeks. Just to give some context, the broader S&P 500 Index ($SPX) has increased by 29.84% over the past 52 weeks, and the S&P Semiconductor SPDR ETF (XSD) gained 138.64% over the same period. However, Micron still carries a cheap valuation. Its forward-adjusted price-to-earnings (non-GAAP) ratio is just 8.35 times, well below the industry average of 24.06 times.

As the demand for memory chips remains robust, Micron might be a buy at cheap levels.

About Micron Stock

Headquartered in Boise, Idaho, Micron Technology is a leading producer of memory and storage semiconductors. Its core operations span designing, manufacturing, and selling DRAM, NAND, and NOR products through four key segments: Cloud Memory Business Unit; Core Data Center Business Unit; Mobile and Client Business Unit; and Automotive and Embedded Business Unit.

With a vertically integrated model, Micron controls wafer fabrication at advanced facilities worldwide, as well as assembly, testing, and global distribution. The company emphasizes innovation in HBM for AI applications, serving cloud, PC, mobile, and enterprise markets. It has a market capitalization of $560.17 billion.

The sustained explosive demand for its memory chips in AI applications has continued to drive Micron’s stock higher. This year, the stock is up 83.79%, while the S&P 500 index is up 4.8% year-to-date (YTD). In addition, the stock has outperformed the XSD ETF, which is up 44.46% YTD. Micron’s shares reached a 52-week high of $531.36 on April 27.

Micron’s 14-day relative strength index (RSI) of 73.20 is closer to the overbought territory than the oversold territory.

Micron Powers AI Surge with Stellar Q2 Results

For the second quarter of fiscal 2026 (quarter ended Feb. 26), Micron reported growth across all segments, with new records set across multiple financial metrics. The company’s revenue climbed by 196.3% year-over-year (YOY) to $23.86 billion. Wall Street analysts had expected Q2 revenue to be $19.61 billion.

This triple-digit growth also translated into skyrocketing profitability. The company’s non-GAAP gross margin as a percentage of revenue increased from 37.9% in the prior-year period to 74.9%. Its non-GAAP EPS grew by a striking 682.1% YOY to $12.20, surpassing the $8.80 that Street analysts had expected.

Street analysts are robustly optimistic about Micron’s bottom line trajectory. For the current fiscal year, EPS is projected to surge 651.4% annually to $57.71, followed by a 69.4% increase to $97.77 in the next fiscal year.

What Do Analysts Think About Micron’s Stock?

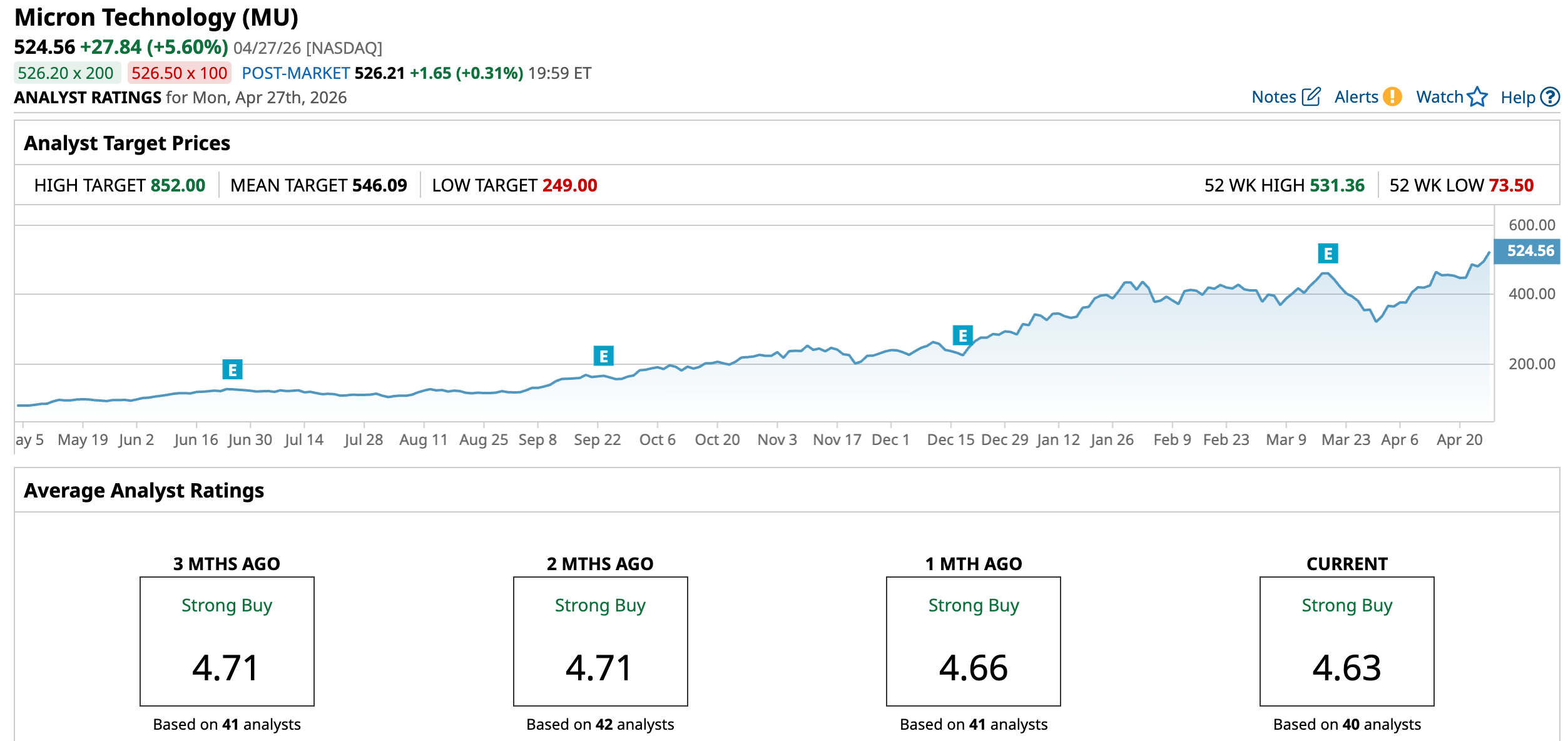

This month, analysts at UBS maintained a “Buy” rating on Micron’s stock, while raising the price target from $510 to $535. The company continues to face a favorable pricing backdrop for DRAM and NAND memory chips, especially for HBM, while UBS analysts heard about hyperscalers and OEMs actively negotiating with a strong intent to secure long-term supply agreements with Micron.

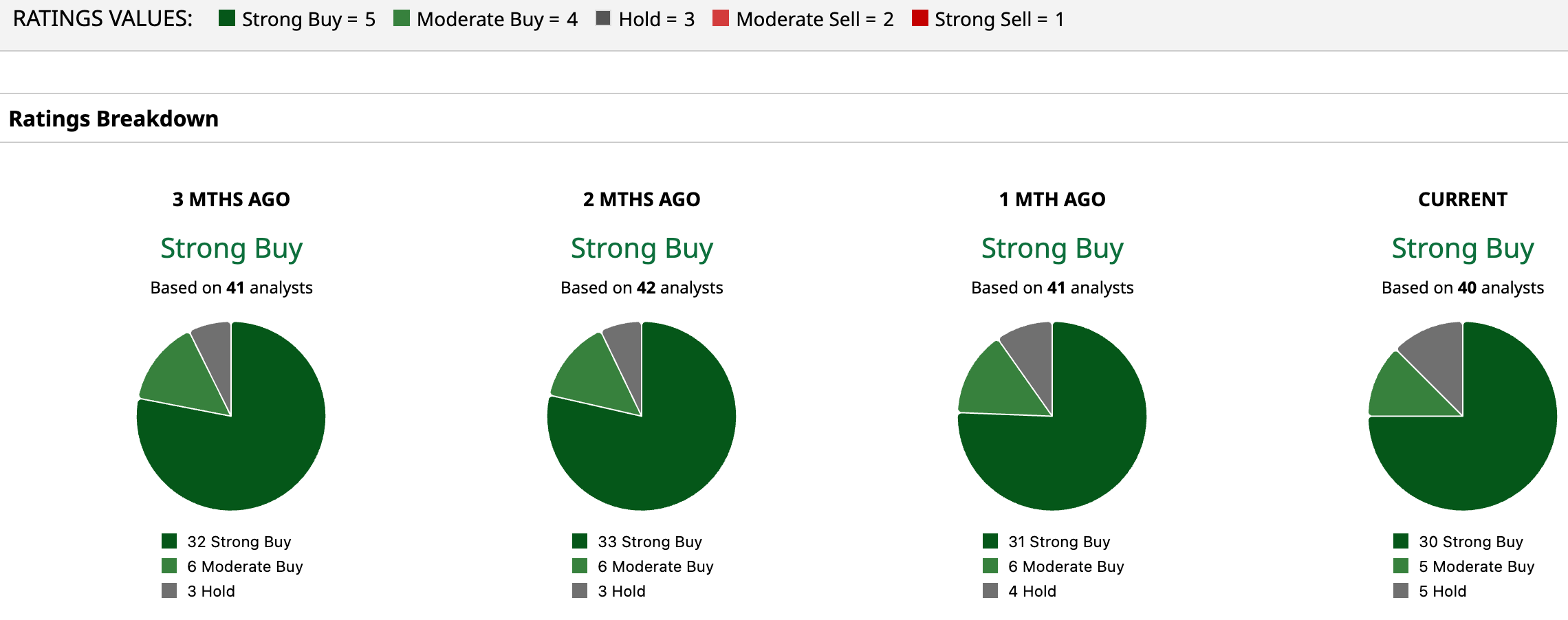

Micron is gaining praise on Wall Street, with analysts awarding it a consensus “Strong Buy” rating overall. Of the 40 analysts rating the stock, a majority of 30 have given it a “Strong Buy” rating, five a “Moderate Buy,” and five a “Hold.” The consensus price target of $546.09 represents a 4.1% upside from current levels. Moreover, the Street-high price target of $852 implies a 62.4% upside.

On the date of publication, Anushka Dutta did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Microsoft%20headquarters%20By%20Peter.jpeg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/NVIDIA%20Corp%20logo%20outside%20building-by%20BING-JHEN_HONG%20via%20iStock.jpg)

/Amazon%20-%20Image%20by%20bluestork%20via%20Shutterstock.jpg)