Dismissing all the talk of a bubble and fears around huge capex, shares of one of the most popular and widely owned semiconductor indices recently crossed all-time highs. The PHLX Semiconductor Index ($SOX) closed above 10,500 on Friday—a level never seen before. Continued high and sustainable demand, along with tight supply, is contributing to this searing rally. This has been validated in a study by consulting major McKinsey, which has estimated that the value of the global semiconductor industry is set to exceed $1.5 trillion by 2030.

Now, there are numerous ways to benefit from this trend. While the usual suspects, such as Nvidia (NVDA) and AMD (AMD), are well-known, the world of semiconductor stocks goes much beyond these limited names. Thus, here are a couple of names from the sector that are quickly becoming the Street's favorites. What works for them and what doesn't? Let's find out.

Atomera (ATOM)

Founded in 2001, Atomera (ATOM) is a semiconductor materials and IP licensing company. It operates as a fabless technology provider, meaning it does not manufacture chips itself but develops materials/process technologies that semiconductor foundries can integrate.

Valued at a market cap of $333 million, the ATOM stock has been on a tear this year, zooming by 256% on a YTD basis. Although it is down almost 9% in early trading Monday.

With no large-scale commercial adoption, however, the company's most recent results were a miss all around. Encouragingly, revenues increased to $50,000 from $23,000 in the year-ago period, and losses narrowed to $0.14 per share from $0.16 per share in the prior year.

In terms of liquidity, Atomera ended 2025 with a cash balance of $19.2 million, well ahead of its short-term debt of just $567,000.

Yet, beyond the muted results, two key developments have made stakeholders excited about the stock, leading to its subsequent rally. First, the company demonstrated the manufacturability of its proprietary MST technology on Gate-All-Around transistor structures, and second, a top-20 semiconductor company began running production wafers using Mears Silicon Technology (MST) on gallium nitride. Moreover, the company announced a deeper collaboration with engineering solutions provider Synopsys (SNPS), providing further impetus to the rally.

On a broader basis, what separates Atomera from others is its MST, mentioned above. MST is a thin film of reengineered silicon, typically only 100 to 300 angstroms thick, applied as a channel enhancement to CMOS-type transistors, designed to boost performance and power efficiency. What separates it from the crowd is that MST can be implemented using equipment already deployed in semiconductor manufacturing facilities, making it complementary to other nano-scaling technologies in the semiconductor industry roadmap rather than requiring fabs to overhaul their lines, which is a critical commercial advantage.

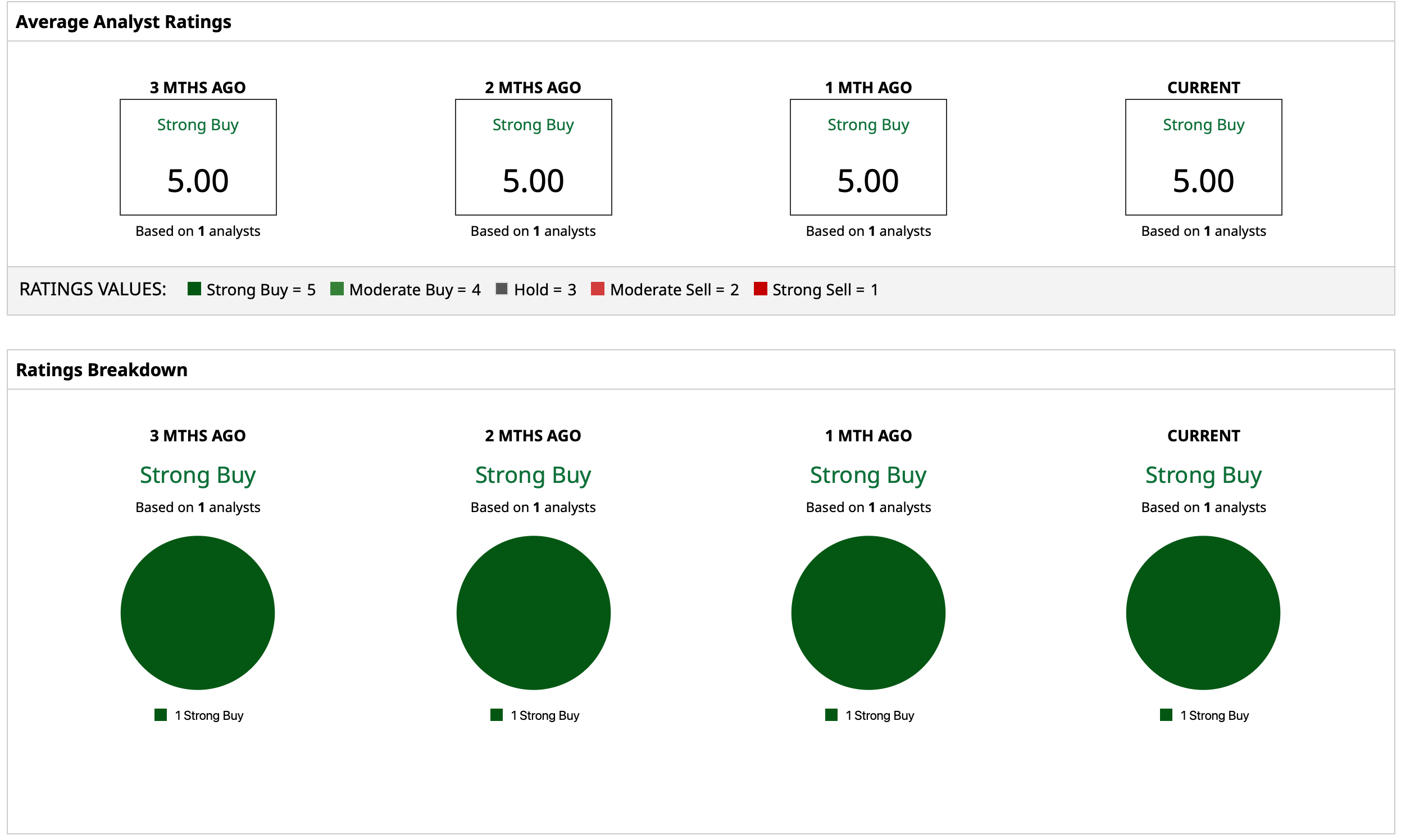

Overall, coverage remains limited, however, on the stock. With a single “Strong Buy” rating, both the mean and high target prices have been surpassed.

GCT Semiconductor (GCTS)

The second top-rated chip stock investors should buy is GCT Semiconductor (GCTS). Founded in 1998, GCT Semiconductor is also a fabless semiconductor company focused on wireless communication chipsets, particularly 4G LTE and 5G solutions. It designs and sells wireless connectivity chips used in smartphones, routers, and IoT devices, among others.

Valued at a market cap of about $98 million, the GCTS stock is up 9% on a YTD basis.

However, GCT reported a decline in revenues along with a widening of losses in 2025, which is a matter of concern. The company reported net revenues of $2.9 million in 2025, much lower than 2024's $9.1 million. Further, losses widened substantially to $0.82 per share from $0.30 per share in the prior year.

The liquidity position is also shaky, with the company exiting 2025 with a cash balance of just $590,000, comparable to its short-term debt levels of $686,000.

Yet, all is not lost, and the company's operations are slowly but surely gaining traction. It is one of the very few small-cap chipmakers that has actually crossed the threshold from 5G development into real commercial shipments. In Q4 2025, the company shipped over 1,900 5G chipsets for commercial use, with Gogo (GOGO) publicly confirming the activation of its air-to-ground 5G network using GCT's technology, which is meaningful proof that the chips work in some of the most demanding wireless environments imaginable.

Overall, what gives GCT a genuine competitive edge is the combination of product breadth and market positioning. The company licensed its 5G and 4G chipsets to one of the world's largest satellite communications providers and partnered with Skylo Technologies, a non-terrestrial network provider covering 36 countries across 70 million square kilometers, targeting the fast-growing segment where devices seamlessly switch between satellite and ground networks. Notably, management has cited a million-plus annual unit potential from the satellite program alone.

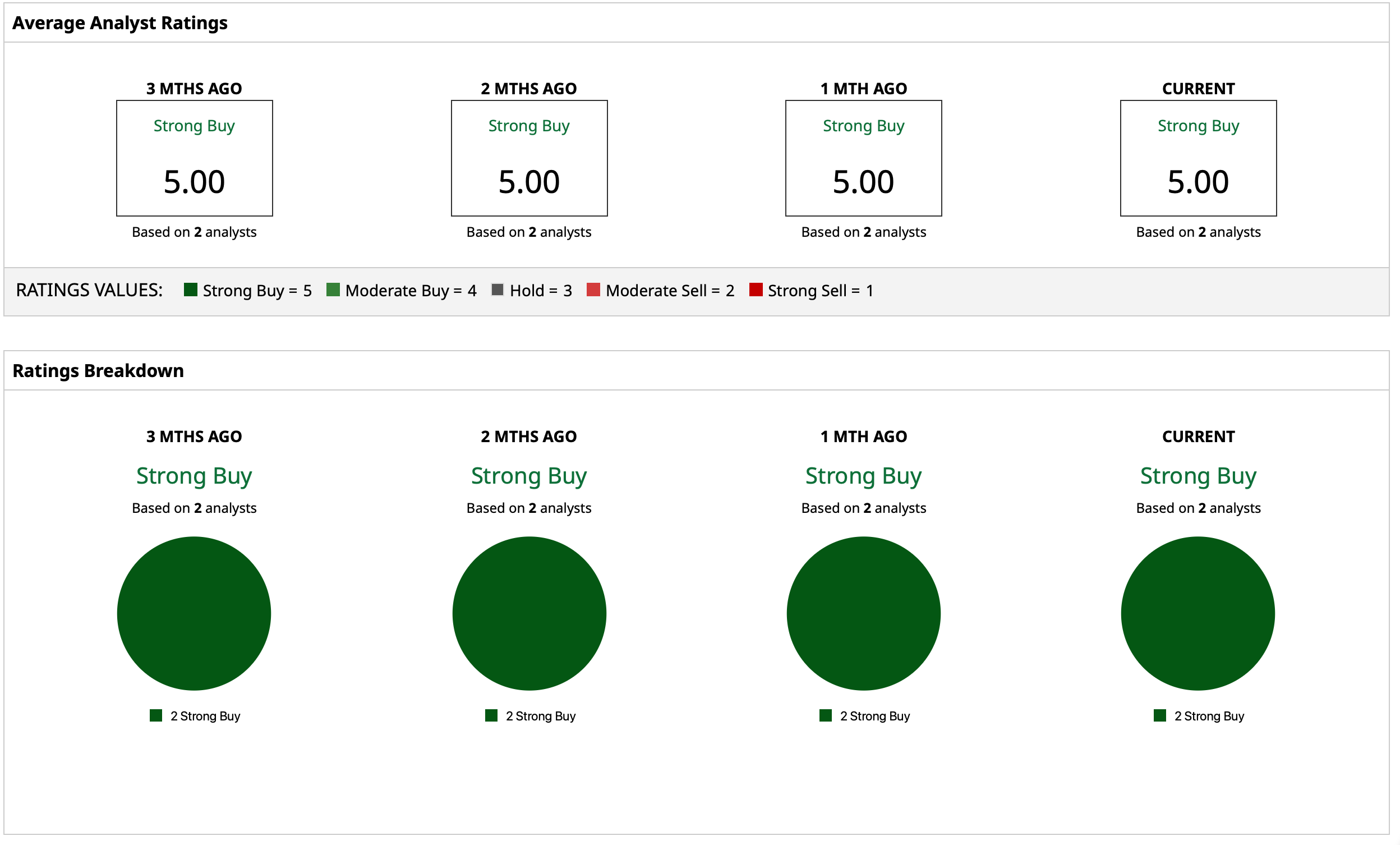

Thus, analysts have deemed GCTS stock a “Strong Buy,” although the coverage is limited, just like ATOM above. The mean target price of $3.47 indicates an upside potential of about 169% from current levels, with two analysts unanimously giving the stock a rating of “Strong Buy.”

On the date of publication, Pathikrit Bose did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Dell%20Technologies%20by%20Poetra_RH%20via%20Shutterstock.jpg)

/The%20sign%20for%20Marvell%20Technology%20out%20front%20of%20a%20corporate%20office%20by%20Valeriya%20Zankovych%20via%20Shutterstock.jpg)

/Intel%20Corp_%20badge%20holder-by%20hasrul_rais%20via%20Shutterstock.jpg)