/Tesla%20Inc%20logo%20by-%20baileystock%20via%20iStock.jpg)

Tesla (TSLA) reported Q1 2026 earnings on April 22, and the numbers looked strong at first glance. Revenue grew 16% year-over-year (YOY) and came in above Wall Street estimates. Even so, the stock fell about 3.6% in the next session.

The main issue was one comment from CFO Vaibhav Taneja on the earnings call. Tesla said its 2026 capital spending would rise to more than $25 billion, up sharply from the $8.6 billion it spent in 2025 and above the $20 billion investors were already expecting. Management also said that free cash flow would stay negative for the rest of the year at that spending level. That helped drive the selloff and pushed TSLA’s year-to-date (YTD) loss past 16%, making it the worst performer in the "Magnificent Seven" this year after gaining 32.64% in 2025.

But that may not be the whole story. While investors are focused on Tesla’s spending, Roth Capital analyst Craig Irwin said this week that what matters most for TSLA right now isn’t Tesla at all, it’s SpaceX. SpaceX is aiming for an IPO roadshow in the week of June 8 and is looking to raise $75 billion at a valuation of as much as $1.75 trillion. If that happens, it would be the biggest IPO ever, far ahead of Saudi Aramco’s $29 billion raise in 2019.

So if the market gets swept up in SpaceX, will Tesla’s $25 billion spending plan still matter as much as it does now? Let’s find out.

The Numbers Behind the CapEx Backlash

Tesla makes electric vehicles, sells energy storage products, and is spending more heavily on AI and robotics. Currently, its market capitalization is $1.4 trillion.

Tesla trades at 274.26 times forward earnings, far above the sector average of 15.83 times, which means investors are still pricing in a lot of future growth with little room for mistakes.

Its first-quarter 2026 results were actually strong. Revenue came in at $22.39 billion, ahead of the $22.06 billion Wall Street expected, while non-GAAP earnings per share of $0.41 also beat the $0.36 estimate. Gross margin improved to 21.1% from 16.3% a year earlier, operating margin rose to 4.2% from 2.1%, and free cash flow margin increased to 6.5% from 3.4%. But even with those better numbers, the stock still fell nearly 7% for the week because investors were more focused on what the higher capex could do to cash flow going forward.

The Growth Engines Behind Tesla’s Next Chapter

Tesla is working on a smaller and cheaper electric SUV as it tries to fix slowing sales. This will be a completely new model, not a smaller Model 3 or Model Y. It is expected to be about 14 feet long, which is shorter than the Model Y. Production will start in China and later expand to the U.S. and Europe. That matters because Tesla had dropped its low-cost vehicle plans in 2024 when Musk turned more of the company's focus toward robotaxis and humanoid robots.

At the same time, Tesla is building out the supply side. Its lithium refinery near Corpus Christi, Texas is now up and running, and the company says it is the biggest and most advanced one in the U.S. The plant turns spodumene ore into battery-grade lithium hydroxide using a new process for North America. Tesla says the method is cleaner, simpler, and cheaper, which could help lower battery costs while also reducing U.S. dependence on China for refined lithium.

Tesla is also planning a $4.3 billion battery cell plant in Lansing, Michigan, with LG Energy Solution. Production is set to begin in 2027, and the batteries will be used in Megapack 3 systems for the energy storage business. Those cells will then be shipped to Houston, giving Tesla a more local battery supply chain for one of its fastest-growing businesses.

Wall Street’s Split View

Wall Street sees June quarter earnings at $0.30 per share, up from $0.27 a year ago. The September quarter estimate is $0.38, just slightly above last year's $0.37. For full-year 2026, the average estimate is $1.35 per share versus $1.09 in 2025, and that rises to $1.86 in 2027.

Wedbush's Dan Ives is still one of the biggest bulls on the stock. He says the heavy spending is needed if Tesla wants to become a major player in physical AI, and he kept his “Outperform” rating with a Street-high $600 price target.

RBC Capital is positive too, but a bit more careful. It lowered its target to $475 from $480 while keeping an “Outperform” rating, pointing to the bigger capex bill and some caution around humanoid robots. Needham is more skeptical. It kept a “Hold” rating and no price target, saying Tesla's first-quarter margin beat may not last because some of the gains were one-off.

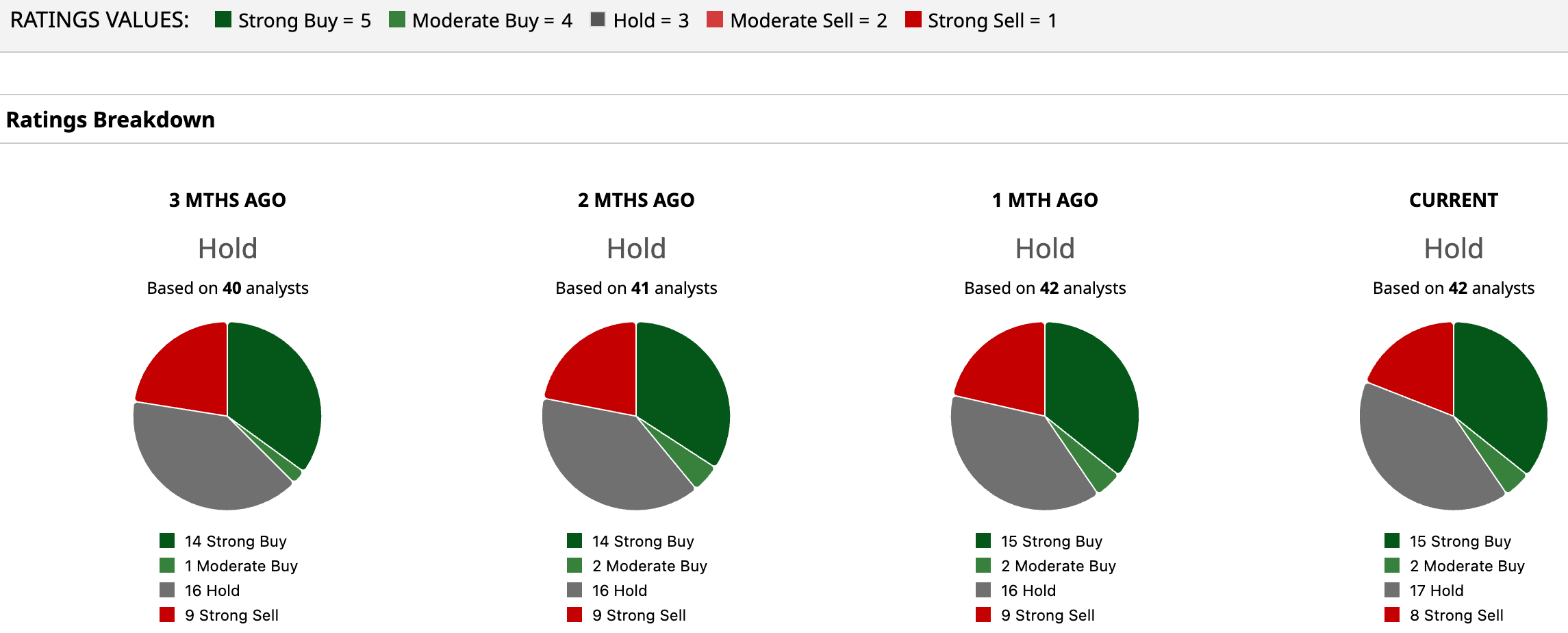

For Tesla, 42 analysts who were surveyed give a consensus rating of “Hold," with the mean price target is $405.08. That suggests just 6.77% upside from the current price.

Conclusion

The market’s first reaction says the $25 billion spending plan matters, but probably not for as long as the recent selloff suggests. Tesla is still asking investors to fund a very expensive transition into AI, robotics, energy, and lower-cost vehicles all at once, so near-term volatility looks more likely than a clean rebound. Even so, the bigger force over the next few months may be sentiment around Elon Musk’s broader ecosystem, because a successful SpaceX IPO could quickly pull attention away from Tesla’s cash burn and back toward the growth optionality investors usually pay up for in Musk-linked assets.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Renewable%20Energy%20by%20Yuri%20Hoya%20via%20Shutterstock.jpg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)