/Intel%20Corp_%20logo%20on%20mobile%20phone-by%20Piotr%20Swat%20via%20Shutterstock.jpg)

Shares of Intel Corporation (INTC) have witnessed an extraordinary rally in 2026, advancing about 130% year-to-date (YTD) following a sharp post-earnings surge of 23.6% on Friday. The latest surge in INTC stock was driven by stronger-than-expected first-quarter performance, strengthening the view that Intel is regaining operational momentum after several years of strategic and execution challenges.

The company’s Q1 results point to improving demand dynamics, particularly in segments related to artificial intelligence (AI) infrastructure. Moreover, management’s forward guidance suggests that this momentum will likely be sustained, driven by AI-related workloads. Notably, Intel’s solid operating performance also shows that the company is beginning to participate more meaningfully in the secular growth themes that have benefited its peers in the semiconductor space.

While Intel’s fundamentals are improving, its valuation has also expanded rapidly, pricing in the positives.

Into Intel’s Q1 Performance

Intel reported a strong first-quarter performance, supported by robust demand and a better-than-expected supply environment. It also benefited from a more favorable product mix and better pricing, which helped offset rising costs.

Revenue for the quarter reached $13.6 billion, marking a 7% increase year-over-year (YoY). Notably, Intel’s AI-related businesses are driving its growth, accounting for 60% of total revenue in Q1 and expanding by 40% YoY.

The Data Center and AI (DCAI) segment is witnessing solid growth, generating $5.1 billion in revenue. This represented a 7% sequential increase and a 22% rise YoY. The segment’s growth was broad-based across customers and segments, driven by increasing investments in CPUs as AI workloads evolve from training to inference and, increasingly, to more advanced agentic applications.

Notably, demand for custom silicon also surged, with Application-Specific Integrated Circuits (ASICs) revenue climbing more than 30% sequentially and nearly doubling YoY.

The segment is likely to sustain strong growth led by AI-driven demand. Moreover, Intel secured several long-term agreements during the quarter, including one with Alphabet’s (GOOG) (GOOGL) Google, which strengthens the segment’s growth trajectory.

In the Client Computing Group (CCG), revenue totaled $7.7 billion. Although this was a 6% decline from the previous quarter, it still exceeded management’s expectations. Demand remained strong despite ongoing industry challenges such as component shortages and inflation and continued to outpace available supply. Notably, Intel’s AI-powered PCs are seeing strong growth, with revenue in this category rising 8% sequentially and now accounting for more than 60% of the client CPU mix.

Intel’s profitability also improved during Q1, with adjusted gross margin reaching 41%, up 1.8% from a year earlier. This improvement was driven by higher volumes, a favorable product mix, and pricing actions. Overall, Intel delivered adjusted earnings of $0.29 per share for the quarter, significantly outperforming its earlier guidance of break-even. The better-than-expected bottom-line performance reflects stronger revenue, improved margins, and a focus on cost reduction.

Intel to Sustain Momentum in Q2

Intel is expected to maintain its momentum into the second quarter, even as macroeconomic and geopolitical pressures persist. During its Q1 conference call, management highlighted that customer orders remain robust in the near term, which will support its top line in Q2.

Notably, the ongoing expansion of AI infrastructure is driving demand for CPUs, which will support Intel’s growth. Management anticipates strong growth ahead, led by higher CPU demand, which is expected to carry forward through 2027.

Thanks to a favorable demand environment, Intel has projected Q2 revenue of $13.8 billion to $14.8 billion, reflecting a sequential increase of 2% to 9%. The company expects both its CCG and DCAI segments to mark growth, driven by improved supply conditions and the full-quarter impact of pricing adjustments. Notably, the DCAI segment is expected to deliver double-digit growth.

Despite this positive revenue outlook, rising input costs could pressure margins and potentially affect demand. Even so, profitability is expected to improve, with management forecasting Q2 EPS of $0.20, a significant improvement from an adjusted loss of $0.10 in the same quarter last year.

Can INTC Stock Sustain This Rally?

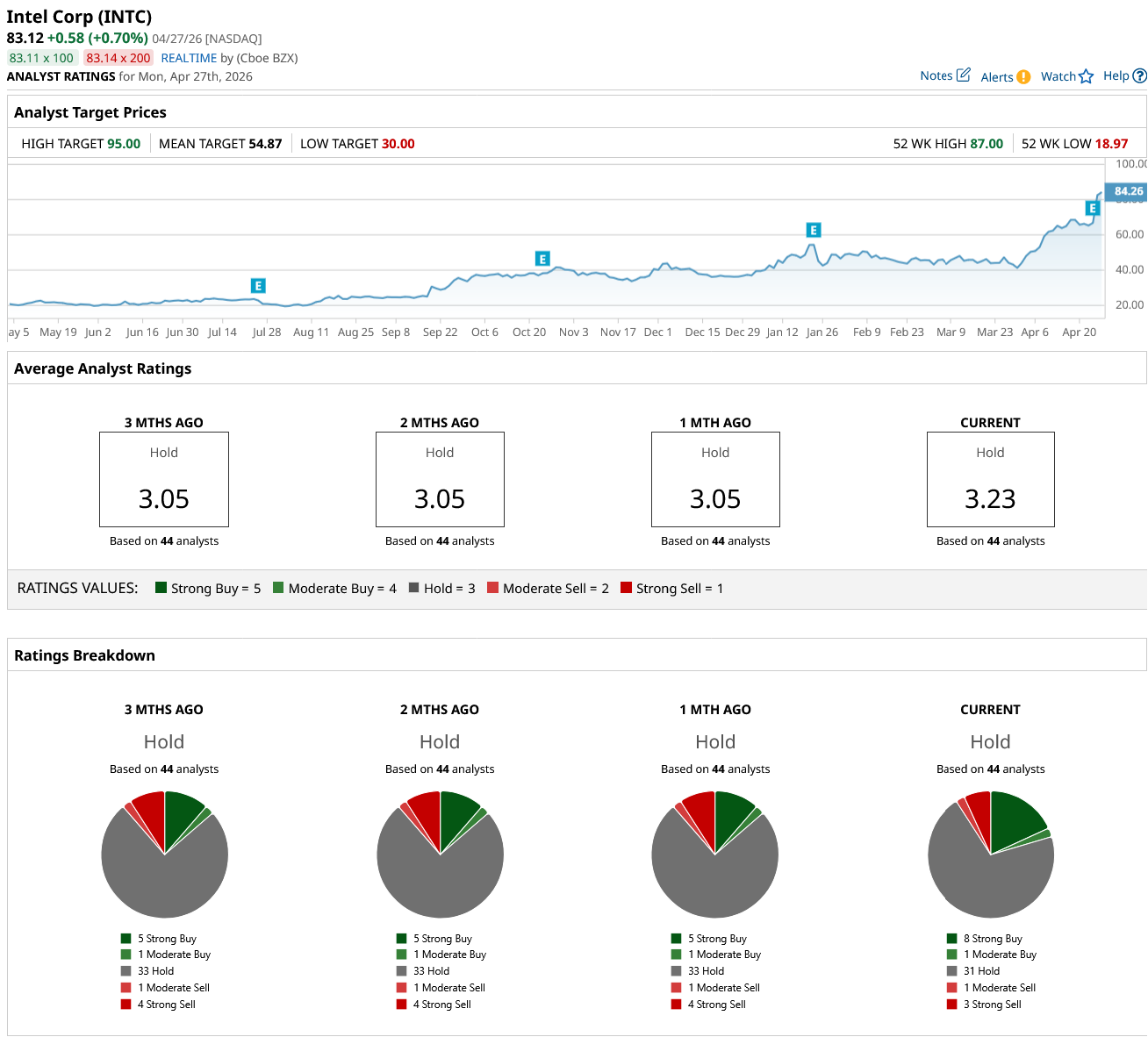

Intel’s solid operating performance and the positive investor sentiment could support Intel stock in the short term. The company’s outlook remains encouraging, driven by rising demand for AI-related computing and continued strength in the CPU market. Improved pricing is also expected to help support margins. This suggests INTC stock could reach its highest price target of $95.

That said, the sharp run-up in INTC stock suggests that much of this optimism is already priced in. Wall Street analysts currently rate Intel shares as a consensus “Hold.” While the company’s long-term prospects remain positive, investors should wait for a pullback before considering new positions.

On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/An%20aerial%20view%20of%20a%20data%20center%20cooling%20system%20by%20Sepia100%20via%20Adobe%20Stock.jpeg)