/Eli%20Lilly%20and%20Co_%20by%20Sergio%20Photone%20via%20Shutterstock.jpg)

Eli Lilly (LLY) stock closed notably down on April 24 following reports that its newly launched oral obesity pill, Foundayo, is trailing Novo Nordisk’s (NVO) oral Wegovy in initial uptake.

Moreover, the IQVIA prescription data for the week ending April 17 showed a modest 0.3% week-over-week decline in total prescriptions across Lilly's broader GLP-1 lineup.

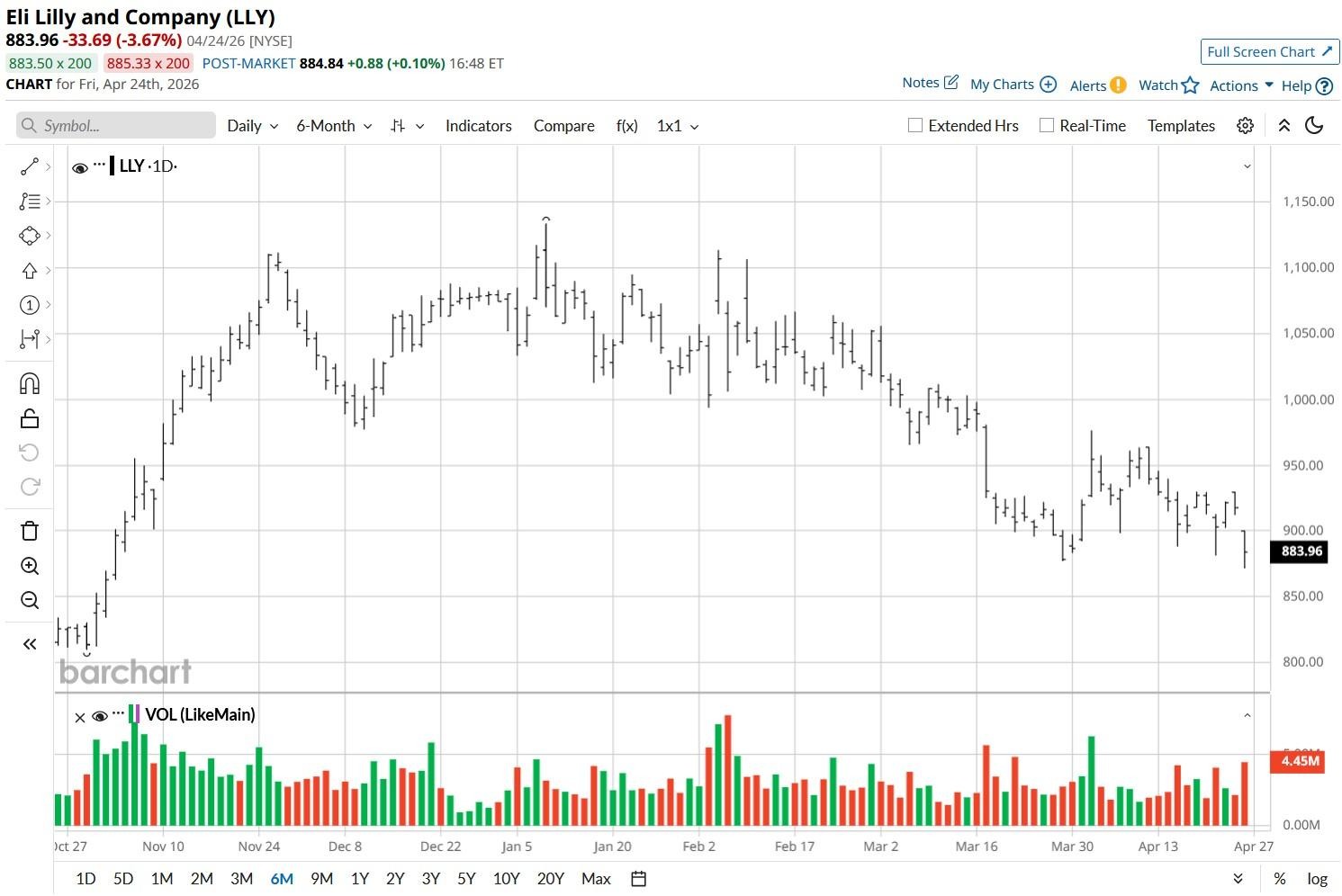

Eli Lilly stock has been a major disappointment for investors in 2026, currently down more than 20% versus its year-to-date high.

Should You Load Up on Eli Lilly Stock Today

Foundayo, which launched on April 9, recorded only about 3,700 prescriptions in its second week on the market, according to IQVIA data released on Friday.

LLY shares slipped primarily because this compares to roughly 18,400 for NVO’s oral Wegovy during a comparable launch period.

However, context matters enormously here. Lilly still commands an estimated 59% share of new GLP-1 prescriptions — and the overall GLP-1 market continues to expand at around 32% year-over-year.

Morgan Stanley analysts project nearly 6% upside to 2026 estimates for Mounjaro and Zepbound combined, suggesting the Street may still be underappreciating volume growth trajectories.

A 0.78% dividend yield makes LLY even more attractive to buy on the current dip.

LLY Shares Are Now Attractively Priced

Long-term investors should consider loading up on Eli Lilly shares also because they’re now going for about 27x forward earnings, a significant discount to the euphoric peaks of the initial GLP-1 hype cycle.

The company’s multiple has compressed even as its portfolio has diversified and its risk profile has arguably improved. Plus, Lilly’s debt-to-EBITDA ratio is expected to fall below 1x this year, which indicates ample balance sheet flexibility for tuck-in acquisitions and pipeline investment.

Meanwhile, LLY’s partnership expansion with Hims & Hers (HIMS), enabling prescriptions of Zepbound and Foundayo through the LillyDirect pharmacy service, demonstrates it is proactively broadening distribution rather than ceding ground.

Note that Eli Lilly has a history of closing both May and June in the green — a historical pattern that makes it even more attractive to own in the near term.

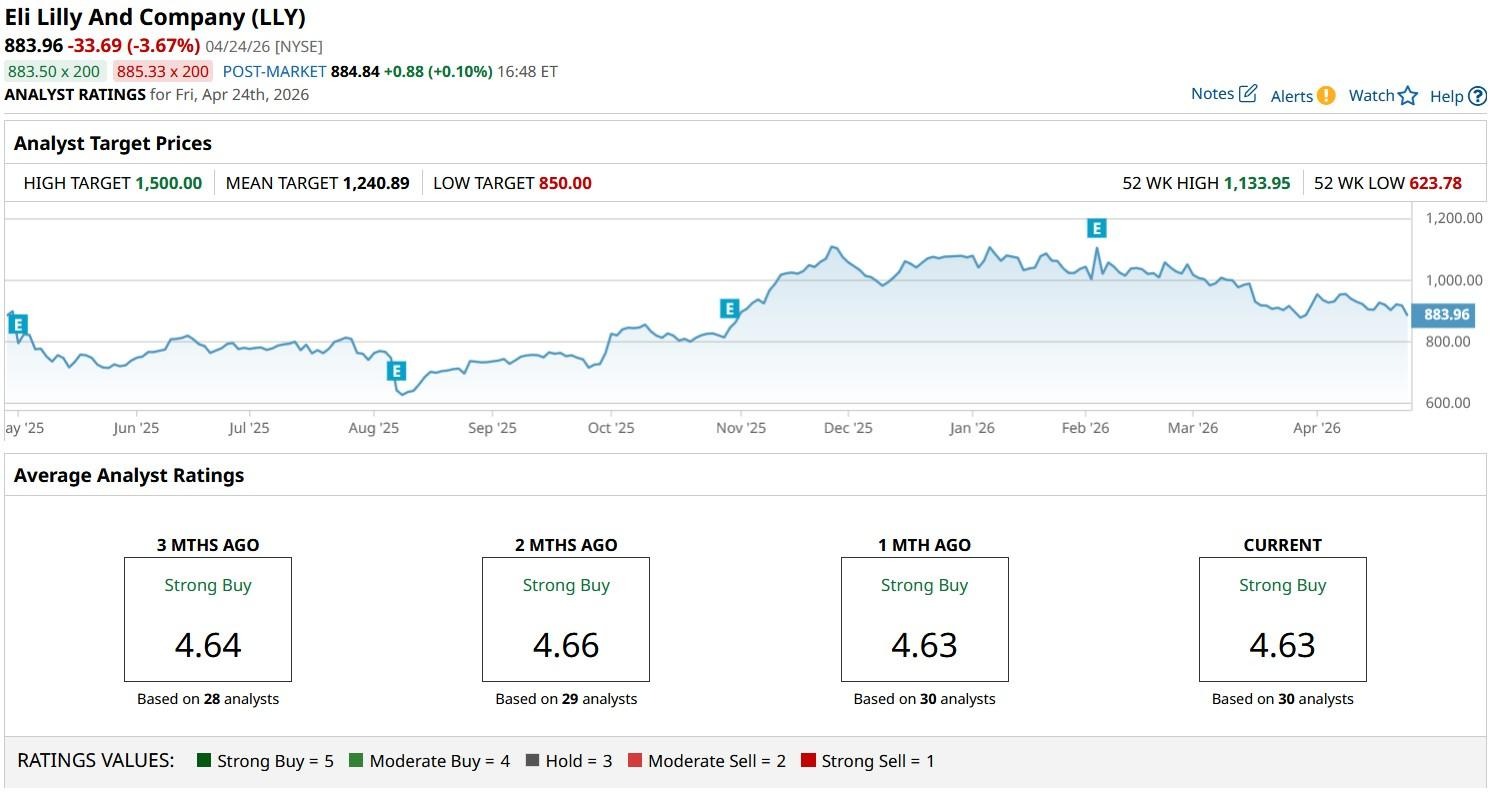

What’s the Consensus Rating on Eli Lilly?

Wall Street also remains bullish on LLY stock, especially after management’s guidance for robust 25% revenue growth in 2026.

The consensus rating on Eli Lilly sits at a “Strong Buy” currently, with the mean price target of about $1,241 indicating potential upside of more than 25% from here.

This article was created with the support of automated content tools from our partners at Sigma.AI. Together, our financial data and AI solutions help us to deliver more informed market headline analysis to readers faster than ever.

On the date of publication, Wajeeh Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Microsoft%20headquarters%20By%20Peter.jpeg)

/Apple%20products%20on%20desk%20by%20Ake%20Ngiamsanguan%20via%20iStock.jpg)

/Nvidia%20logo%20by%20Konstantin%20Savusia%20via%20Shutterstock.jpg)