News Corporation (NWS) is a diversified media and information services company based in New York. Valued at $16.9 billion by market cap, its global footprint spans news publishing, digital real estate services, book publishing, and subscription-based content platforms.

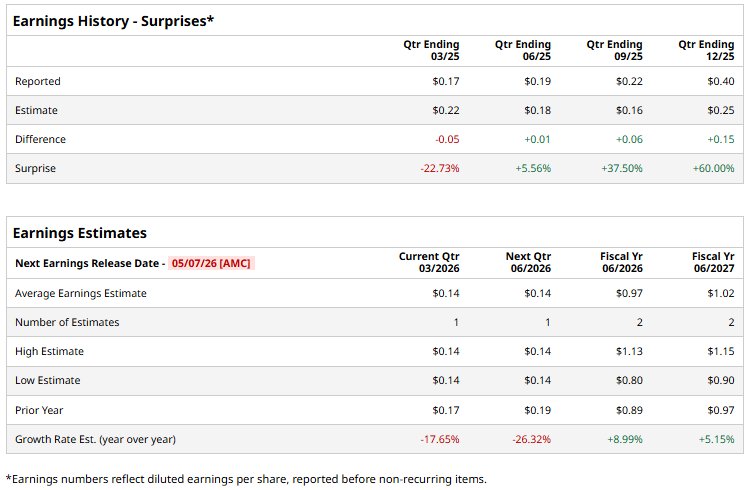

The global media and information powerhouse is gearing up to report its fiscal 2026 third-quarter earnings after the market closes on Thursday, May 7. Ahead of the event, Wall Street currently forecasts a profit of $0.14 per share on a diluted basis, down 17.7% from $0.17 per share in the year-ago quarter. The company beat the consensus estimates in three of the last four quarters while missing the forecast on another occasion.

Looking beyond the immediate quarter, the broader trajectory appears more constructive. In the current year, analysts expect NWS’ EPS to climb 9% to $0.97 from $0.89 in fiscal 2025. Additionally, its EPS is expected to rise 5.2% annually to $1.02 in fiscal 2027.

NWS stock has dropped 2.5% over the past year, underperforming the S&P 500 Index’s ($SPX) 30.6% gains and the State Street Communication Services Select Sector SPDR ETF’s (XLC) 23.2% uptick over the same time frame.

News Corporation has lagged the broader market over the past year largely due to a mix of cyclical pressures and structural headwinds across its portfolio. A key drag has been its digital real estate segment, where platforms like REA Group and Realtor.com are sensitive to housing market activity.

At the same time, its News Media division continues to face structural decline in print advertising, and while digital subscriptions are growing, they haven’t fully offset the erosion in legacy revenues. Investor sentiment has also been tempered by uneven earnings momentum, including occasional misses and expectations of short-term profit declines,

Analysts’ consensus opinion on NWS stock is reasonably bullish, with a “Moderate Buy” rating overall. Out of the three analysts covering the stock, two advise a “Strong Buy” and one suggests a “Hold” rating. NWS’ average analyst price target is $37, indicating a potential upside of 22.4% from the current levels.

On the date of publication, Kritika Sarmah did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/An%20Intel%20sign%20out%20front%20of%20a%20corporate%20office%20by%20wolterke%20via%20Adobe%20Stock.jpeg)

/Alibaba%20by%20testing%20via%20Shutterstock.jpg)

/Alphabet%20(Google)%20Image%20by%20Markus%20Mainka%20via%20Shutterstock.jpg)