/Insurance%20salesman%20and%20customer%20signing%20agreement%20by%20kamiphotos%20via%20Adobe%20Stock.jpeg)

Valued at a market cap of $25.8 billion, W. R. Berkley Corporation (WRB) is a leading commercial property and casualty insurance holding company that provides insurance and reinsurance products to businesses and individuals worldwide. The Greenwich, Connecticut-based company’s offerings include commercial auto, workers' compensation, professional liability, excess and surplus lines, healthcare, environmental, and specialty insurance, serving a broad range of industries.

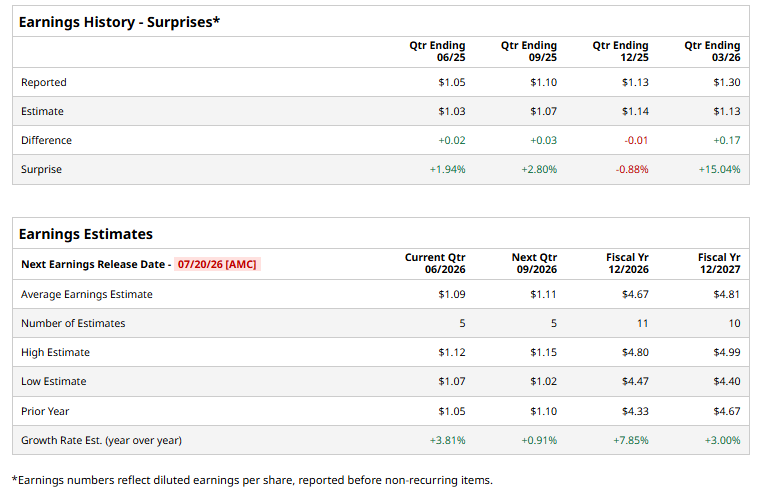

The insurance company is expected to announce its fiscal Q1 earnings for 2026 after the market closes on Monday, July 20. As we approach the event, analysts expect this insurance company to report a profit of $1.09 per share, up 3.8% from $1.05 per share in the year-ago quarter. The company has topped Wall Street’s bottom-line estimates in three of the last four quarters, while missing on another occasion.

For the current fiscal year, ending in December, analysts expect WRB to report a profit of $4.67 per share, up 7.9% from $4.33 per share in fiscal 2025. Furthermore, its EPS is expected to grow 3% year over year to $4.81 in fiscal 2027.

Shares of WRB have declined 3.5% over the past 52 weeks, underperforming the S&P 500 Index's ($SPX) 20.8% return and the State Street Financial Select Sector SPDR ETF’s (XLF) 4% rise over the same time period.

On June 3, W. R. Berkley announced a $0.50-per-share special cash dividend, raised its regular quarterly dividend by 11.1% to $0.10 per share, and restored its share repurchase authorization to 25 million shares, underscoring its commitment to returning capital to shareholders. The announcement was well received, with WRB shares rising 1.6% in the following trading session.

Wall Street analysts are cautious about WRB’s stock, with an overall "Hold" rating. Among 20 analysts covering the stock, two recommend "Strong Buy," 13 indicate “Hold," and five advise “Strong Sell.” While the stock currently trades above the mean price target of $67.53, the Street-high price target of $78 indicates a 12.6% potential upside from the current levels.

On the date of publication, Kritika Sarmah did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Arista%20sing%20at%20headquarters%20of%20an%20American%20multinational%20technology%20company%20Arista%20Networks%20-%20Santa%20Clara%2C%20California%2C%20USA%20-%202020%20By%20MichaelVi.jpeg)

/AI%20(artificial%20intelligence)/AI%20Data%20Center%20by%20Gorodenkoff%20via%20Shutterstock.jpg)